Boots on the Ground. Is Your Playbook Ready?

War, the Fed, and the Biggest Wealth Transfer Since 1945

Easter weekend (April 5-6) is the most likely window for full US escalation against Iran. The calendar, the politics, and the military positioning all converge on that date. If not then, the military posture suggests it’s a matter of time. If you’re reading this before April 5, the question isn’t whether escalation is possible. It’s whether the machinery is already in motion.

If this prediction plays out, here’s what the Easter looks like:

US and Israeli forces launch a coordinated ground-and-air campaign against Iran. Congress is in recess. European markets are closed. By the time London opens on Tuesday, the world will have changed.

This article isn’t about whether war is possible — the machinery is already in motion. It’s about the chain of monetary and financial consequences that most investors haven’t even begun to price. And at the center of that chain sits one institution: the Federal Reserve.

What Happens When the Shooting Starts

Once full escalation begins, the dominoes fall fast:

The Strait of Hormuz functionally closes as marine war-risk insurance collapses. No insurer, no shipping.

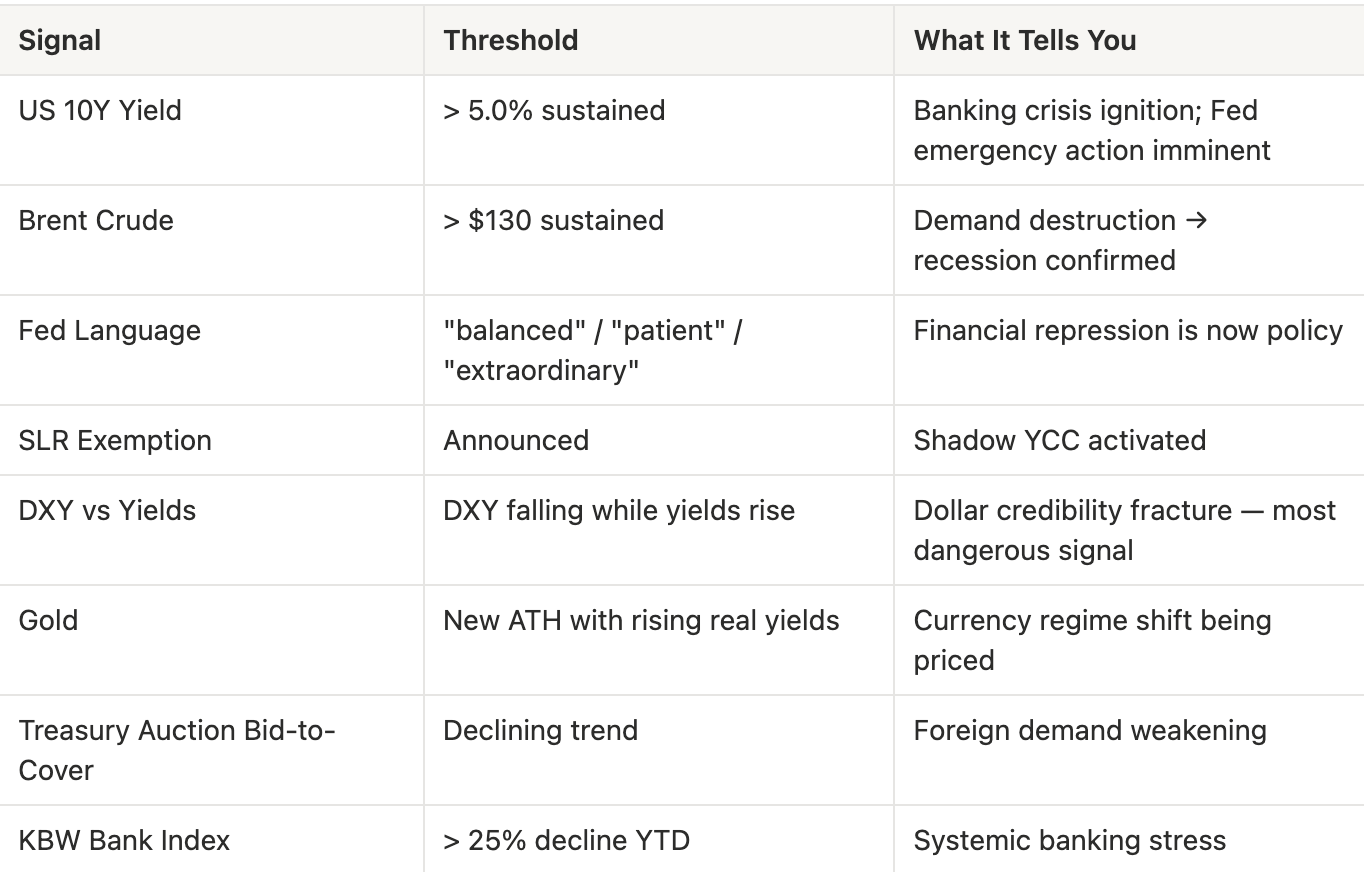

Brent crude breaches $120 and holds. Asian spot LNG prices double.

The US 10-year yield spikes past 4.6%, with intraday prints above 4.8%.

$2.5 trillion gets wiped from global bond markets within weeks (a 100bp move across $25T+ in outstanding Treasuries).

KBW Bank Index drops 18%+. Unrealized losses across the US banking system approach the $690 billion peak seen in late 2022, just before the SVB crisis.

Iran rejects every ceasefire proposal. The US commits ground troops. There is no off-ramp.

This won’t be a temporary disruption. This will be a structural regime shift.

The Oil Shock Is Structural

Forget 2022 comparisons. In 2022, Russia chose to weaponize gas, and Europe rerouted within months. This time, geography is the weapon. The Strait of Hormuz carries ~20% of global oil and ~25% of global LNG.

Here’s where this lands:

Brent $120-150 is the new floor, not the ceiling. Demand destruction will eventually cap prices — but that destruction IS the recession.

Asia enters energy triage. Japan, South Korea, India begin rationing. KOSPI drops 22%+. This becomes a manufacturing depression for import-dependent economies.

Food prices follow energy — always. Fertilizer, transport, cold-chain logistics. The most politically explosive inflation is grocery inflation, and it’s coming.

The 1973 embargo lasted 5 months. This one could exceed it — because reopening would require a political settlement neither side can accept.

The Fed’s Only Move: Financial Repression

The Fed will face three mandates that directly contradict each other:

Control inflation → raise rates

Prevent a banking crisis → cut rates or inject liquidity

Fund the war → keep yields low so Treasury can borrow $1.5T+

You cannot do all three. In wartime, historically, #1 always loses. 1942-1951, Korea, Vietnam — central banks do not tighten into a war their government is fighting.

My base case — not a possibility, a prediction:

The Fed holds at 3.50-3.75% while inflation runs 5-7%. They won’t cut (optics). They won’t hike (that triggers a banking crisis). They will hold and deploy stealth liquidity. Here’s the playbook:

“Patient” language replaces “committed to 2%.” When you hear “patient,” financial repression is policy.

SLR exemption — Treasuries exempt from leverage ratios, turning every bank balance sheet into a captive buyer of government debt. Shadow yield curve control.

Regulatory capital rewrite — risk weights on corporate loans rise, sovereign debt stays at zero. Hundreds of billions quietly redirect from the private economy into Treasuries. No headline. No announcement.

Emergency lending facilities — not called QE. Called “market functioning operations.” The effect is identical.

Regulatory forbearance — bank examiners go easy on unrealized losses. Mark-to-market de-emphasized.

The result: real interest rates turn deeply negative. Government borrows at ~3.75%, inflation runs at 6-7%, and the real value of $39 trillion in debt erodes at 3%+ per year.

This is not a bug. This is the plan. A silent wealth transfer — from savers to the government — just like 1942-1951, except this time the exits aren’t sealed.

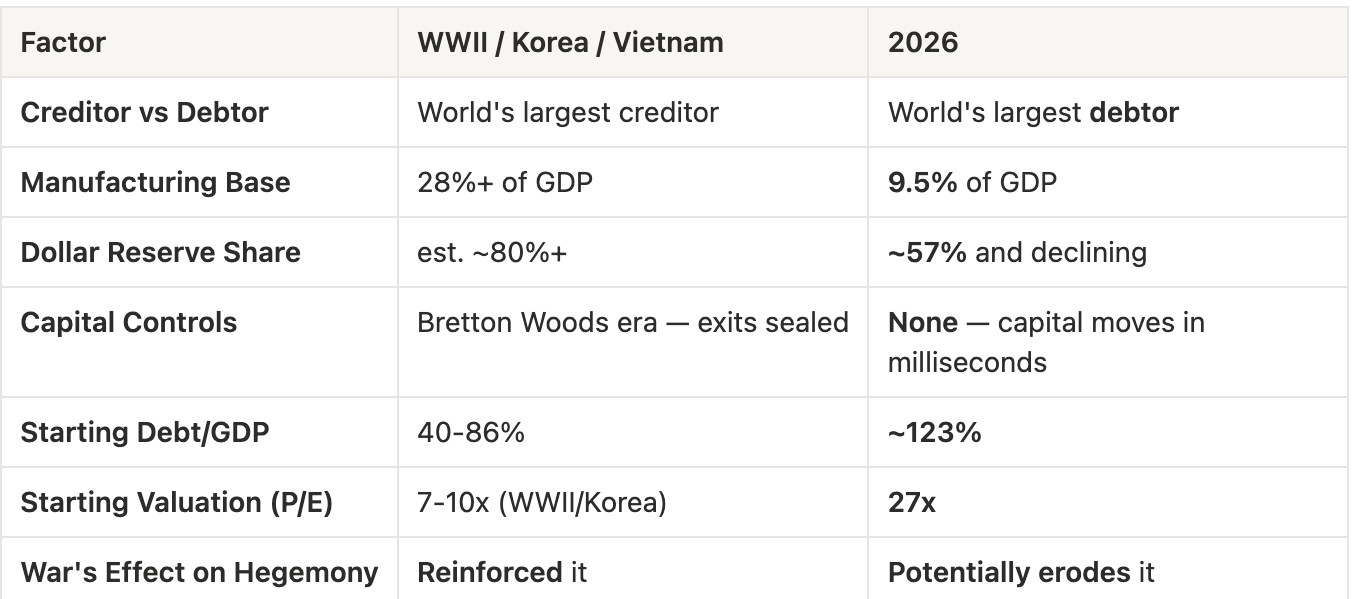

The Dollar Problem

The WWII financial repression playbook worked because creditors had no alternatives. Bretton Woods. Capital controls. No Bitcoin. No Singapore ETFs.

In 2026, every one of those conditions is reversed:

Gulf sovereign wealth funds ($3T+) are actively diversifying away from Treasuries. Any escalation would be in their backyard.

China accelerating Treasury reduction.

Iran accepting yuan for Hormuz transit fees — small in scale, enormous in signal.

Central banks globally accumulating gold at record pace.

The critical signal: watch the DXY against yields. Rising yields should strengthen the dollar. If yields rise and the dollar falls — that’s the market pricing a credibility fracture. That’s when the 1940s playbook breaks.

We’re not there yet. But every week a conflict drags on, the probability rises.

Don’t Buy the “War Economy” Narrative

The White House will sell this as economic stimulus. Manufacturing renaissance. Blue-collar jobs.

The reality:

Manufacturing is 9.5% of GDP today vs 28% in 1953. The transmission channel from military spending to broad stimulus has shrunk by two-thirds.

The $600B in additional spending flows to a narrow set of contractors — Lockheed, Raytheon, Northrop — not the broad economy.

Critical supply chains run through adversary territory — rare earths through China, advanced chips through Taiwan.

The $600B has to come from somewhere: higher taxes (contractionary), more borrowing (yields rise), or money printing (inflation accelerates).

This is not the Arsenal of Democracy. This is a fiscal accelerant on an already-burning fire.

Why Historical War Rallies Don’t Apply

Yes, US markets rose during nearly every major war — WWII, Korea, Vietnam, Gulf War. But every rally rested on conditions that no longer exist:

In 1945, America fought its way into hegemony. In 2026, the question is whether it would be fighting its way out.

And here’s the subtlety most will miss: equities may still rise nominally — and that’s still bearish in real terms. If inflation runs 6-7% and the S&P gains 3-5%, you feel like you’re not losing. But your purchasing power erodes at 2-4% per year. That’s financial repression working exactly as designed.

The exception: energy, defense, commodities, and infrastructure will outperform in real terms. Everything else — tech at 30x, consumer discretionary, financials — reprices for a world of structurally higher costs.

The Escalation Dashboard

Two Paths

Path A: Negotiated Exit Within 3 Months (Secondary case)

Hormuz partially reopens. Oil falls to $90-100. Fed holds, inflation peaks at 5-6% and fades. Banks survive but weakened. Gold holds gains. Equities recover 10-15% from lows, led by energy and defense. Dollar stabilizes.

Painful but contained.

Path B: Prolonged War, 6+ Months (Base case — 65%)

No ceasefire. Hormuz stays closed. Oil grinds above $120. Inflation embeds. Full financial repression playbook activated.

When markets reopen:

Crude surges. Brent $120-150 floor.

Japan and South Korea gap down hard.

US equities sell off unevenly — energy/defense rally, tech/consumer/financials reprice lower.

US regional banks under severe stress — another SVB-scale event likely.

Dollar weakens on trade-weighted basis — even as yields rise.

Treasuries destroy purchasing power under negative real yields.

Gold long-term bullish — but margin calls may push it down first.

The Bottom Line

War doesn’t solve America’s debt problem. War IS America’s debt problem.

And the most dangerous part? In the short run, it may not look like it. Nominal rallies in defense and energy will make headlines. The S&P may even hold. That’s not strength — that’s the anesthesia before the surgery.

Debt/GDP at ~123% — already exceeding the WWII peak. No Marshall Plan on the other side. No Bretton Woods II. Unlike 1945, the US won’t emerge as the sole industrial power — China’s manufacturing base is intact, and the war’s destruction is in a region that won’t need American-led reconstruction.

There is only the Fed, a printing press, and the hope that the world keeps accepting the paper.

The moment to watch is not the next bomb. It’s the next Treasury auction. When the bid-to-cover ratio breaks, the game changes. Because that’s when the market realizes the war isn’t just in the Middle East.

It’s in the bond market. And in the bond market, America is fighting itself.

This article was written and published on March 29, 2026 — one week before Easter weekend. The escalation framework, the Fed prediction, and the positioning are all locked before the first shot is fired. Consider this a sealed envelope: if you’re reading it after April 5, you already know whether we were right.

Garrett’s Signal delivers original macro research at the intersection of geopolitics, energy, and rates. Subscribe for the Weekly Signal Playbook — where the triggers, sizing, and invalidation levels live.

Thanks! Great financial breakdown of what I argue on a much more aggregate level. A question: you see a wealth transfer from citizens to government - I agree but see that as a ‘station’ on the way to private/industrial pockets. Basically, the state being the one organising the transit of funds from the regular man-in-the-street’s savings to industrial (oligarch) accounts. No?

Great article. I think Path A remains the most credible path (No Ground Invasion) and should be the base case instead of your current base case (Path B). I’ve laid out the reasons why a ground invasion, although possible is still not the base case: https://asymmetryfinder.substack.com/p/a-ground-invasion-of-iran-would-be?utm_campaign=post-expanded-share&utm_medium=web