Hormuz Is the Battlefield

The Strait is shut. Duration is mispriced. Risk assets stay under pressure.

Core Thesis: We have argued since Day 1 that the market was not pricing the duration of the Hormuz disruption. Brent's surge from $85 to $119.50 suggests that repricing has now begun, but the situation is far more complex than a simple oil trade. The Strait of Hormuz has been functionally shut down by the combination of Iran's cheap asymmetric arsenal and the collapse of the global marine insurance system. Air strikes cannot reopen it. The US is trapped in a war it is winning tactically and losing strategically: unable to exit without surrendering its entire Middle East alliance system, yet unable to end the crisis from the air. The only remaining decent exit is the Xi-Trump summit, but Beijing has no overwhelming incentive to help unless the price is enormous. If diplomacy fails, the logic of the situation points toward ground troops, and an empire's graveyard that dwarfs Afghanistan.

I. TEN Days In: The War Nobody Planned For

On February 28, 2026, the United States and Israel launched Operation Epic Fury / Roaring Lion, the most intense aerial campaign against a sovereign nation since the 2003 invasion of Iraq. In eleven days, the coalition has:

Struck over 3,000 targets across Iran

Sunk 43 Iranian naval vessels, effectively eliminating Iran’s conventional navy

Killed Supreme Leader Ali Khamenei and 48+ senior officials

Destroyed the Natanz nuclear facility, IRGC headquarters, and key missile production sites

Deployed 50,000+ personnel, 200+ aircraft, and 2 carrier strike groups

By any conventional military metric, this is overwhelming dominance. And yet:

Iran has not surrendered. Khamenei’s son Mojtaba has been appointed the new Supreme Leader. The IRGC has sworn allegiance.

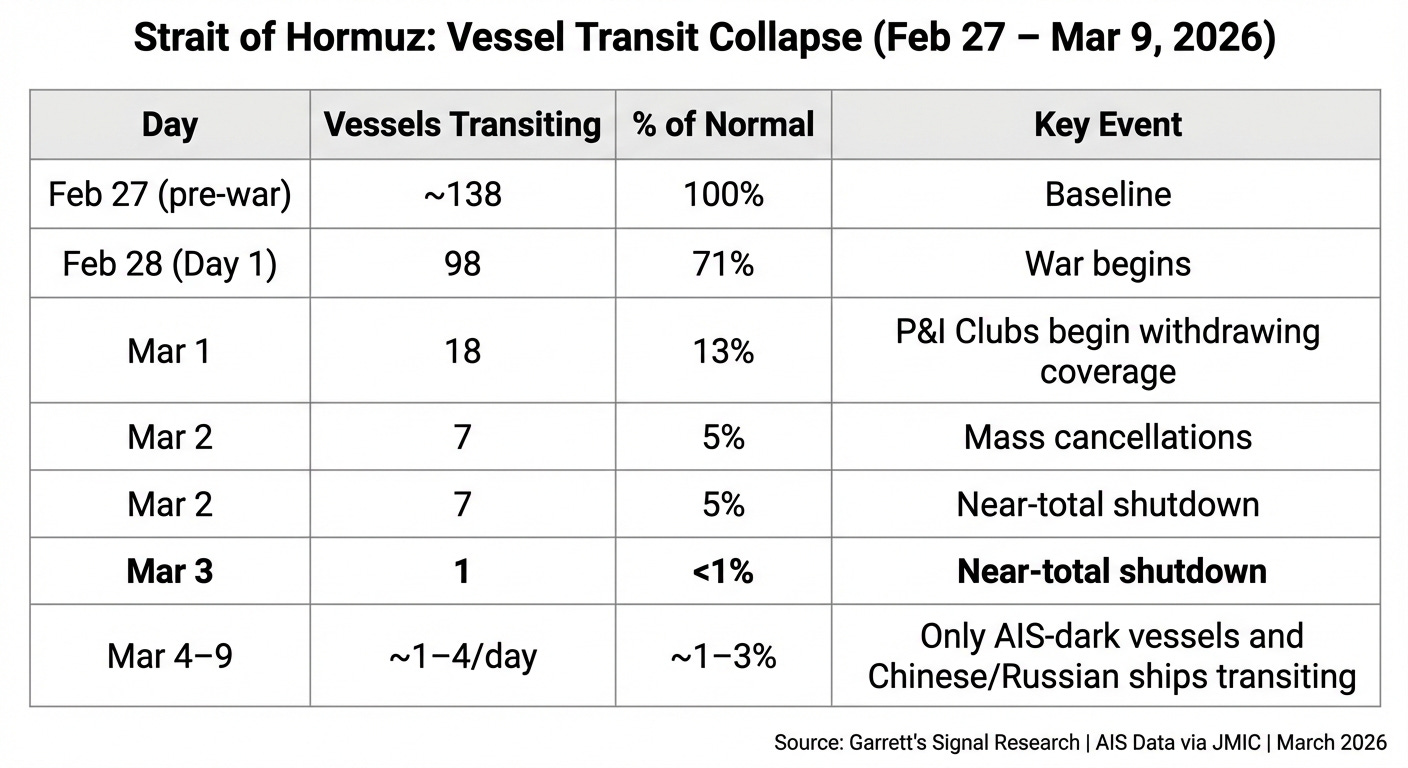

The Strait of Hormuz remains functionally closed: only 9 commercial vessels have transited since March 3.

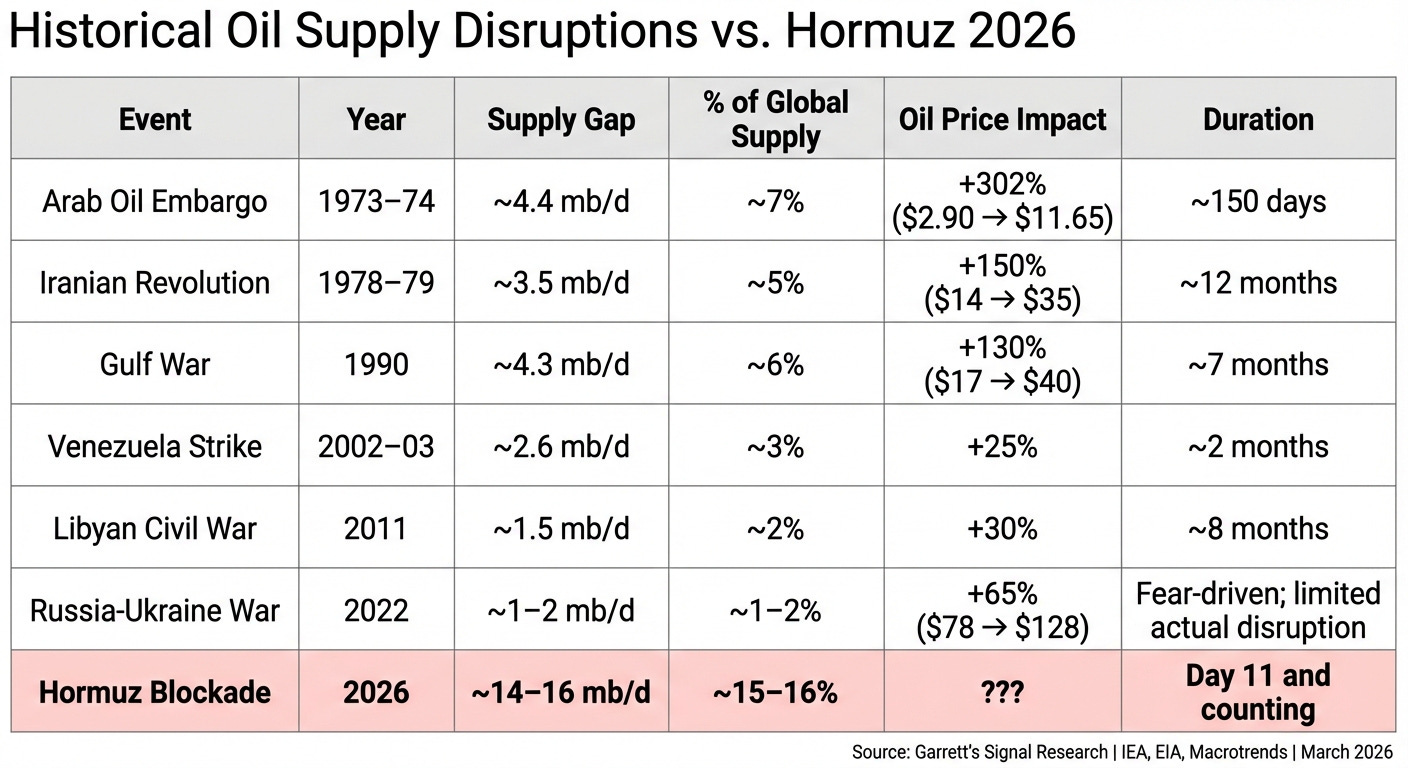

Brent crude has surged 64% to $119.50, with JPMorgan projecting Middle East production cuts exceeding 4 mb/d by next weekend.

7 American service members are dead.

Iran claims it can sustain six months of high-intensity operations and will deploy more advanced long-range missiles.

The paradox is stark: America is winning every battle and losing the war. The coalition has destroyed Iran's conventional military, but the real battlefield was never in Iranian airspace. It is the 33 km-wide Strait of Hormuz, and it remains firmly in Iranian hands.

II. The Hormuz Crisis: Why the Strait Cannot Be Reopened

The Strait of Hormuz is functionally closed. Not because Iran has laid a wall of mines across the channel, but because no rational shipowner will send a vessel through it, and no insurer will cover one that tries.

This is the product of two reinforcing forces: physical threat and insurance collapse. Both must be understood together.

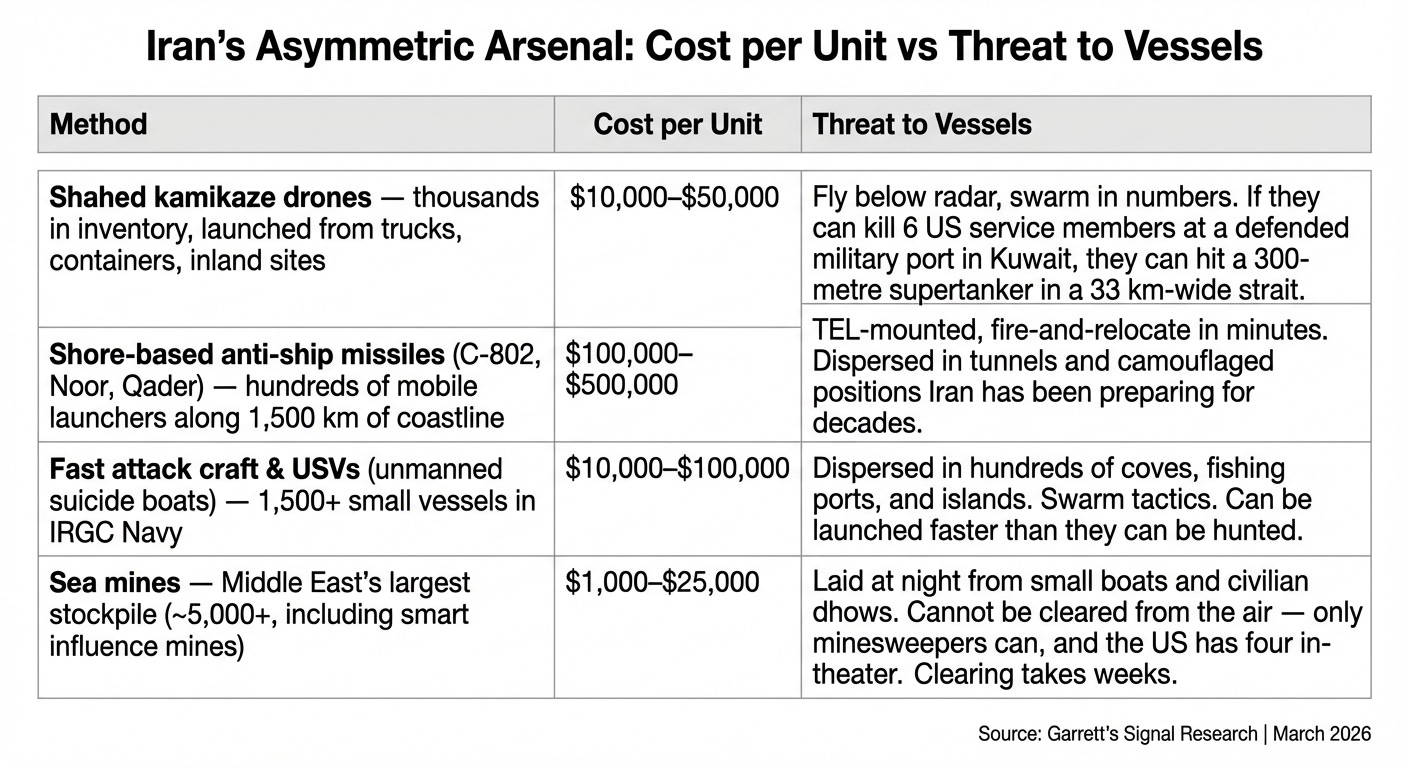

2.1 The Physical Threat: Iran’s Asymmetric Arsenal

2.1.1 Electronic Warfare: The “Soft Blockade”

The Strait is also being closed by invisible means: GPS jamming and spoofing. Recent shipping-track data shows vessel “clusters” and impossible reported speeds (tankers at >100 knots) — classic signatures of GNSS interference. The effects cascade: degraded navigation in a narrow, crowded waterway; unreliable collision-avoidance systems; corrupted AIS position broadcasts (AIS embeds GPS-derived coordinates, so spoofed GPS = spoofed AIS); and, critically, shattered insurer confidence in safe-transit models.

Attribution is ambiguous — both state militaries and Iran-aligned forces have capability and incentive — but attribution is also irrelevant to the market impact. What matters is the duration implication: even a credible ceasefire headline does not instantly reopen Hormuz if the electronic environment remains degraded. Jamming is a force multiplier that hardens the insurance/crew-refusal feedback loop without firing a shot.

The coalition has sunk 43 Iranian warships. But the IRGC does not need a functioning navy to make Hormuz impassable. It has an arsenal of cheap, dispersed, and practically inexhaustible methods to threaten any vessel transiting the strait:

9+ commercial vessels have already been attacked across the Persian Gulf since the war began — from Kuwait to Oman. The IRGC has demonstrated it can strike ships at will across the entire waterway, not just the narrow strait itself.

The cost asymmetry is devastating. A Shahed drone costs $10,000–$50,000. A Patriot interceptor costs $2–4M. A supertanker carries $150–200M of crude. Iran can launch dozens of threats against a single transit for less than the cost of one interception. Even if 90% are stopped, the 10% that get through make the entire route uninsurable. This is the arithmetic that has shut Hormuz, not a physical blockade.

2.2 The Insurance Collapse

The physical threat alone didn’t close Hormuz. What closed it was the global marine insurance system’s response to that threat.

The mechanism:

EU Solvency II regulations require insurers to hold capital against “1-in-200-year” loss events. War outbreak triggered immediate model recalculation.

The 12 P&I Clubs covering ~90% of global ocean-going vessels faced instant capital shortfalls. Reinsurance contracts allow 7-day cancellation.

Without P&I certificates, ports worldwide refuse to berth ships. Without war risk coverage, letters of credit cannot be issued. The entire trade chain breaks.

The Joint War Committee (JWC) designated the entire Persian Gulf as an expanded high-risk area. War risk premiums surged from 0.15% to 1-3% of hull value.

The International Transport Workers’ Federation (ITF) declared that crew members have the right to refuse entry into the war zone.

“Insurance withdrawal is doing the work that physical blockade has not.” — Kpler

Even if a ceasefire were announced tomorrow, rebuilding the insurance architecture would take weeks. JWC must reassess risk zones → P&I Clubs must re-underwrite → ship owners must sign new contracts → crew must agree to sail → ports must accept the new coverage. The minimum recovery timeline from a credible ceasefire signal to 50%+ transit recovery is 3-4 weeks. The base case is 6-10 weeks.

Historical analogs support this estimate. After the September 2019 Abqaiq-Khurais drone attack (a single-day event with no sustained threat), war risk premiums in the Persian Gulf took 2-3 weeks to normalize, and that was from a much lower baseline. In the Red Sea crisis (2023-24), the JWC expanded the high-risk zone in December 2023; six months later, with Houthi attacks continuing, major container lines still had not resumed Red Sea transit. Insurance markets have long memories and short risk appetites.

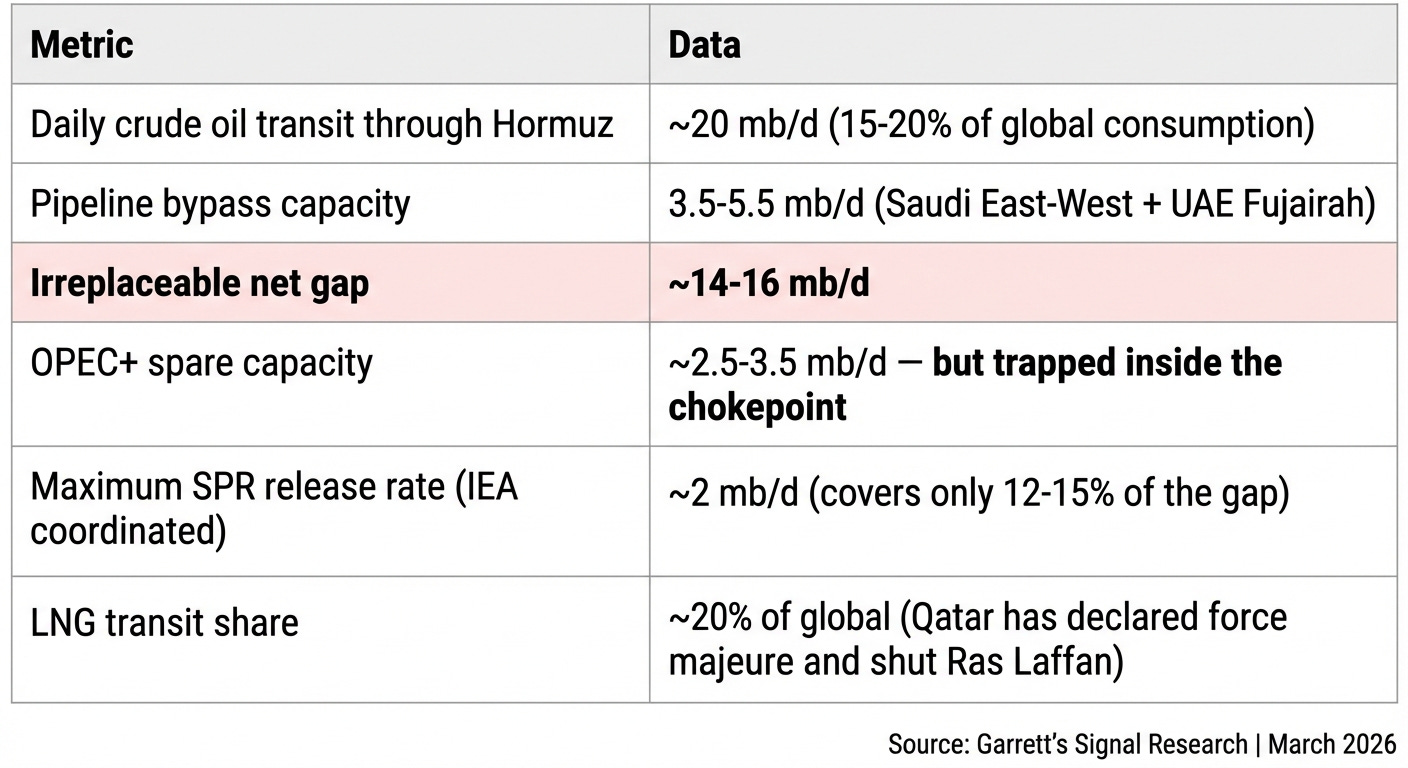

2.3 The Supply Gap Is Unprecedented

Gross gap vs. net effective shortage. The 14–16 mb/d figure is the gross disruption — total Hormuz flow minus pipeline bypass capacity. The net effective shortage will be smaller, because high prices trigger demand destruction (estimated short-run elasticity: ~0.03–0.05), fuel switching, rationing, and drawdowns from non-Hormuz sources. At $120+ Brent, demand destruction of 1–2 mb/d is plausible within 30 days; at $150+, 3–5 mb/d. Combined with SPR releases (~2 mb/d) and limited non-OPEC supply response, the net effective gap at Phase 3 pricing is more likely 6–10 mb/d, still historically unprecedented, but meaningfully smaller than the gross headline figure. We use the gross number to frame the scale of the disruption; the phased pricing model in Section VI incorporates demand-side offsets.

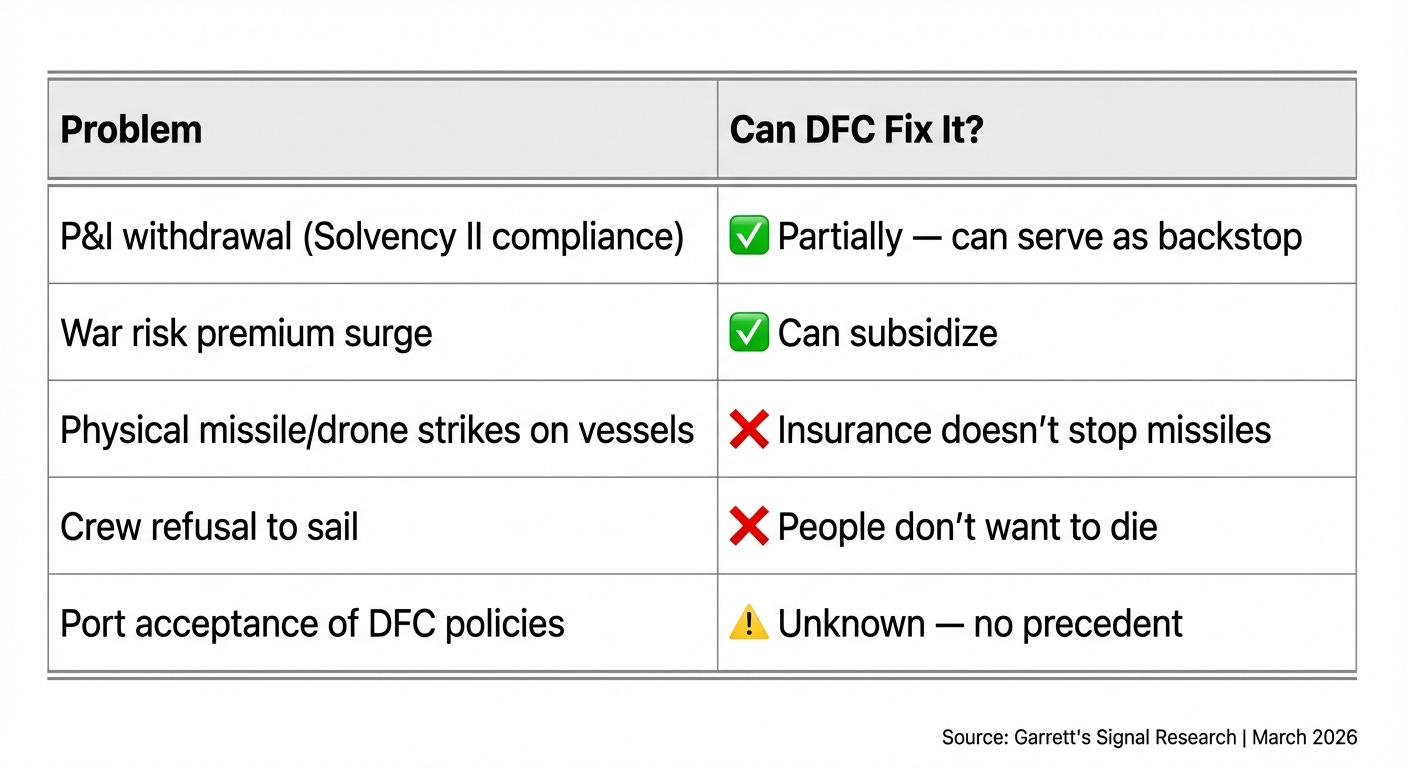

2.4 The DFC Insurance Fix: Necessary but Insufficient

Trump ordered the US Development Finance Corporation (DFC) to provide political risk insurance for Gulf shipping. The assessment:

Specific terms still have not been published. Even under the most optimistic assumptions, DFC implementation to first vessel departure requires 1-2 weeks. And one successful Iranian attack on a transiting commercial vessel would instantly destroy all confidence in the "insurance recovery → normalization" thesis.

III. Iran’s “Selective Blockade”

3.1 What Iran Is Actually Doing

Iran declared Hormuz “closed” but issued no formal navigation closure notice. IRGC broadcasts warnings via VHF, but this is rhetorical, not legal. Meanwhile:

Chinese and Russian vessels are explicitly permitted to transit, framed as “strategic gratitude” for their diplomatic positions.

IRGC authorized “direct strikes and destruction” of unauthorized vessels.

But in practice, Greek shipowner Dynacom has sent 5 tankers through with AIS transponders turned off — all transited without being attacked.

Iran knows these ships are passing. Its coastal radars, patrol boats, and electro-optical systems cover the entire 33 km strait. The decision not to attack is deliberate.

The inherent logic of Iran's selective blockade is to sustain (not shorten) duration. The longer it lasts, the more leverage Iran accumulates, and the more unbearable the political and economic costs become for Washington. This is the exact opposite of what markets initially priced.

IV. The Strategic Deadlock: Washington’s Impossible Position

The Hormuz crisis described above creates a problem that has no military solution. The strait is not held by a navy that can be sunk. It is held by dispersed asymmetric threats costing a fraction of what it takes to counter them, and by the global insurance system’s rational response to risk. Every escalation (new strike categories, expanded target lists) feeds directly into the actuarial models that keep Hormuz shut. More bombing = longer closure.

The obvious middle option, naval escort of commercial convoys, sounds intuitive but faces severe practical constraints. Even with a carrier strike group providing air defense, Iran’s threat portfolio includes sea mines (which require slow minesweeper clearance, not air cover), swarming fast boats and USVs launched from hundreds of coastal coves, and Shahed kamikaze drones costing $10,000–$50,000 apiece that can be launched in dozens against a single convoy. A single successful strike on an escorted commercial vessel — even a non-fatal one — would instantly confirm the risk that P&I Clubs are pricing in, and destroy whatever confidence the escort program was meant to create. Escort may reduce the probability of a successful hit, but it cannot eliminate it, and in the insurance world, cannot eliminate is functionally the same as uninsurable. The crew refusal problem is also untouched: sailors are not obligated to enter a war zone regardless of how many warships accompany them.

Meanwhile, the Politico exposé of March 5 revealed the internal truth: CENTCOM has requested intelligence personnel to support operations for at least 100 days, potentially through September, while Trump publicly claims the war will last “4-5 weeks.” A former senior diplomat described the operation as “completely improvised, as if nobody believed military action was imminent.”

4.1 The “Can’t Stay, Can’t Leave” Trap

Why Trump Can’t Exit:

The core cost of withdrawal is not political embarrassment — it is strategic surrender of the entire American position in the Middle East. An exit without a decisive outcome means:

Handing over Gulf allies (Saudi Arabia, UAE, Bahrain, Kuwait) to an emboldened Iran that just survived America’s best shot. These allies would be forced to accommodate Tehran, rebalancing the region’s power structure permanently.

Ceding the oil architecture: pricing power, petrodollar recycling, Aramco/ADNOC investment flows, and the security umbrella that underpins them. Decades of US energy diplomacy, unravelled.

Capital flight from US orbit: Gulf sovereign wealth funds ($3T+) would diversify away from US Treasuries and defense contracts toward Beijing and other partners who didn’t abandon them.

Israel exposed: Netanyahu’s October election hinges on continued US support; withdrawal forces an Israeli ceasefire and potentially ends his political survival.

Nuclear reconstitution: Iran’s 441 kg of HEU (enough for ~11 weapons) means the nuclear program reconstitutes within 6-12 months if facilities aren’t physically secured.

In short: exiting means surrendering the entire Middle East alliance system and the oil, capital, and security architecture behind it. No American president — especially not one who brands himself as a dealmaker — can accept that.

This is the trap. Trump cannot exit without a “victory” big enough to justify the cost. He cannot sustain an indefinite air campaign as oil climbs, inflation accelerates, and his own base fractures. And the core problem — Hormuz — has no air-based solution.

There is, however, a quiet irony buried in this deadlock. While Trump faces acute political pressure to resolve the crisis — rising gas prices, a fracturing base, midterm elections in November, the structural fiscal dynamics of a prolonged conflict are not entirely unfavorable to the United States as a sovereign borrower. Wartime inflation erodes the real value of $36 trillion in predominantly fixed-rate federal debt; defense spending inflates nominal GDP; and the dollar's reserve status allows Washington to finance operations at rates no other belligerent could sustain. This is the same mechanism that shrank US debt-to-GDP from ~120% after WWII to ~30% by the 1970s. The urgency, in other words, is Trump's, not necessarily America's. This distinction matters: it suggests that the institutional machinery of the US government may not be as desperate for a rapid exit as the President's political calendar implies. But the mechanism has limits. If oil sustains above $150 for multiple months and inflation expectations become unanchored (as measured by breakevens, consumer surveys, and wage negotiations), the benign "inflate away the debt" story flips into a credibility crisis for the dollar and the Fed. The line between helpful inflation and destructive inflation is not visible until it has been crossed.

4.2 The Likely Option — and Its Price

If Trump cannot exit, and air strikes alone cannot force Iran to surrender — which eleven days of the most intense bombing since 2003 have already demonstrated is extremely unlikely, then there is only one option left: ground troops.

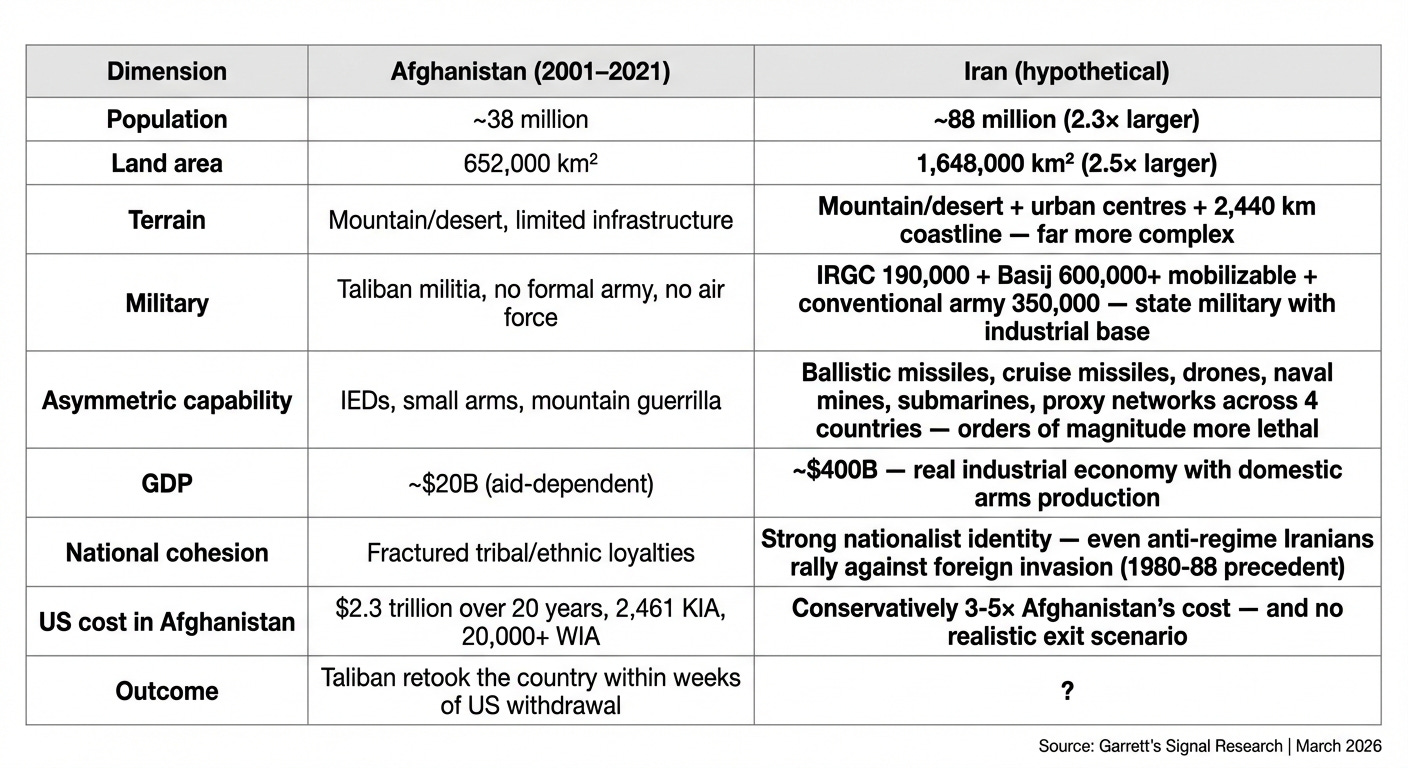

But committing ground forces to Iran would mean entering a theatre that makes Afghanistan look manageable. Consider the comparison:

Iran would be the ultimate "empire's graveyard." Afghanistan cost America $2.3 trillion, 2,461 lives, and 20 years — only to end exactly where it started. Iran is 2.3× the population, 2.5× the land area, with a real military-industrial complex, ballistic missiles, and a national identity forged in the 8-year war against Iraq. If Afghanistan was unwinnable, Iran is unwinnable on a scale that could define the end of American military primacy.

To be clear, Iran is not without vulnerabilities. Khamenei's death and Mojtaba's untested succession create a genuine leadership fragility. The IRGC has sworn allegiance, but institutional loyalty under a new Supreme Leader has never been stress-tested in wartime. Iran's multi-ethnic composition (Persians ~61%, Azeris ~16%, Kurds ~10%, Arabs ~2%) offers potential fault lines that covert operations could exploit. And the urban middle class, which flooded the streets in 2022, has no love for the regime. But these vulnerabilities operate on a longer timeline than the Hormuz crisis. Internal fractures take months to develop and years to become strategically decisive. The 1980–88 Iran-Iraq War demonstrated that foreign military aggression unifies Iranian society across ethnic and political lines; even those who despise the regime rally to national defense. In the near-term window that matters for markets (weeks to months), these internal weaknesses are unlikely to change the fundamental calculus.

V. The Last Off-Ramp: The Xi-Trump Summit

Given the trap described above (can’t exit, can’t win from the air, ground troops lead to an empire’s graveyard), the most plausible off-ramp is diplomacy. And the diplomatic channel with the most leverage over Tehran is Beijing.

Only China and Russia have the relationship with Iran to broker a ceasefire that Tehran would accept. And only under such a framework could Trump credibly frame a negotiated outcome as a strategic victory rather than a retreat.

The question is whether a deal can be reached. Both sides have pressure and both sides have buffers. China imports ~40% of its oil through Hormuz, but it has substantial strategic reserves (500-900M bbl), Russian pipeline supply, and a coal-dominated power grid. The disruption is costly but manageable. The US, as noted above, faces political pain from oil-driven inflation and a fracturing base, but the structural fiscal dynamics are not uniformly negative (see Section 4.1). The urgency is concentrated in Trump’s political timeline (midterm elections, approval ratings, gas prices) rather than in the institutional machinery of the US government, which can absorb a prolonged conflict more comfortably than headlines suggest.

This creates a negotiation where both sides have reasons to deal and reasons to wait. The likely shape of any agreement involves some combination of tariff adjustments, chip export recalibration, and a framework for Gulf energy security, but the exact contours will depend on how the military situation evolves over the coming weeks.

5.1 What If Diplomacy Fails?

The failure modes are multiple: the Bessent–He Lifeng pre-meeting could be cancelled or downgraded to a formality; Beijing could conclude that prolonged US entanglement in the Gulf serves its strategic interests more than a deal; or the two sides could meet but fail to bridge the gap on core issues (Taiwan, chips, tariffs). If the diplomatic track collapses, the situation defaults back to the military deadlock described in Section IV, with no off-ramp, no timeline for Hormuz reopening, and escalating domestic pressure on Trump. In that scenario, oil prices move rapidly into Phase 3–4 territory ($140+), the political pressure for ground troops intensifies, and the risk of a broader regional conflict (involving Hezbollah, Iraqi militias, or direct Iranian strikes on Gulf state infrastructure) rises materially.

What to watch: The Bessent–He Lifeng meeting (expected around March 14 in Paris) is the most important near-term signal. If the meeting proceeds and the Xi-Trump summit is neither delayed nor cancelled, markets will focus intensely on the diplomatic track. We will publish a dedicated deep-dive on the summit dynamics, Beijing's strategy, and scenario analysis at that point. Stay tuned.

VI. The Oil Price Framework: Duration × Chokepoint

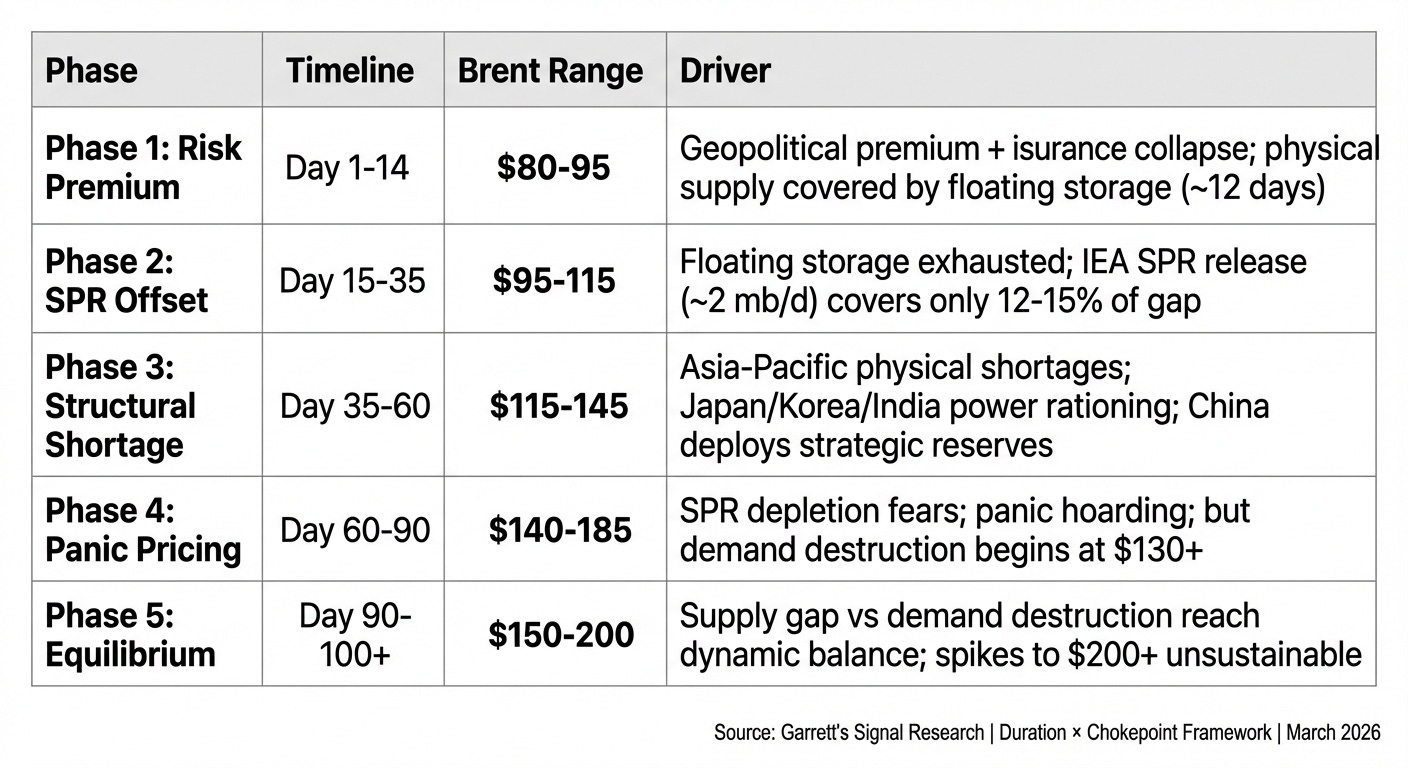

The market’s core mispricing has been duration. At $85 (pre-March 9 surge), Brent was pricing a disruption lasting days to two weeks. At $119.50, the market has begun to price supply destruction — but the full duration repricing has only just begun.

Phase-Based Pricing Model

We are currently transitioning from Phase 1 to Phase 2. The March 9 oil spike ($119.50) reflects the market’s sudden realization that this is not a short-term event — but it has not yet fully priced a multi-month disruption.

Why duration is always underpriced — the COVID lesson. Markets systematically underestimate the persistence of supply shocks. The Fed called post-COVID inflation "transitory" and was wrong for two years. Trump says the war will last "4–5 weeks"; CENTCOM is planning for 100+ days. The pattern is structural: policymakers anchor to optimistic timelines, and markets price accordingly — until reality forces a violent re-mark. The COVID supply-chain disruption was a demand shock that became a supply shock; Hormuz is a supply shock from Day 1, with a J-shaped inflation path rather than a V-shaped one. The asset rotation will rhyme: energy, commodities, and hard assets over growth and duration-sensitive equities — but this time faster, because the transmission channel (oil) is more direct than shipping containers.

Risk Repricing: The Triple Prism Framework

The standard macro read-through — oil → CPI → rates → risk assets down — is correct but incomplete. The Hormuz crisis transmits through three distinct and mutually reinforcing layers, each with its own pricing implications:

Why the Triple Prism matters: Each layer alone would pressure risk assets. But the three layers are self-reinforcing: the Inflation Layer keeps rates high, the Fiscal Layer removes Washington's incentive to resolve it quickly, and the Fragmentation Layer ensures the pain falls disproportionately on energy-importing allies while creating pockets of structural winners. The result is not just "risk off" — it is a regime change in cross-asset correlation, geographic risk distribution, and the market's willingness to price tail duration. Risk assets stay under pressure until a credible path to Hormuz reopening emerges — and even then, the insurance rebuild alone takes 3–6 weeks.

VII Conclusion: The Narrowing Window

1. Hormuz is the real battlefield — and it has no military solution. The strait is closed not by a physical blockade but by the lethal interaction of Iran’s cheap, dispersed asymmetric arsenal and the global marine insurance system’s rational withdrawal. Air strikes have destroyed Iran’s conventional navy, but the IRGC can threaten any vessel with drones, mines, missiles, and fast boats at a fraction of the cost of interception. Every escalation reinforces the actuarial risk that keeps P&I Clubs out, ports closed, and crews grounded. More bombing equals longer closure.

2. Duration — not intensity — is the variable that matters most. At $119.50, Brent has begun to reprice — but only for Phase 1–2 of what could be a multi-month disruption. The potential supply gap (~14–16 mb/d) dwarfs every historical precedent. Pipeline bypasses cover less than a third; SPR releases cover ~12–15% at best; and OPEC+ spare capacity is trapped inside the chokepoint. If Hormuz remains functionally shut beyond Day 35, we enter uncharted territory — Phase 3 structural shortage — where Asia-Pacific physical deficits force rationing and oil moves toward $140+. The repricing has begun; it has not finished.

3. The Xi-Trump summit is the last credible off-ramp. Beijing holds monopolistic leverage as the only power that can simultaneously pressure Tehran and offer Washington a face-saving exit. The Bessent–He Lifeng pre-meeting (expected ~March 14, Paris) is the single most important near-term signal. If it proceeds and the summit stays on track, the diplomatic channel is alive. If it stalls, the window is closing fast.

4. Without a diplomatic exit, the logic of escalation takes over. If the summit fails and Hormuz remains unsolvable from the air, Washington faces an impossible choice: accept strategic retreat (surrendering the Gulf alliance system, oil architecture, and nuclear containment) or commit ground forces to a theatre that makes Afghanistan look manageable. Iran is 2.3× the population, 2.5× the land area, with a real military-industrial complex and a national identity forged in eight years of war. That path leads to an open-ended occupation whose costs could define the end of American military primacy.Thanks for reading Garrett's Signal! Subscribe for free to receive new posts and support my work.

5. For markets, the asymmetry is clear. The upside scenario which is Hormuz reopening with a successful summit leading to ceasefire or other potential events. The downside (diplomatic failure and prolonged closure) has no historical pricing template. In either case, the near-term direction is higher duration premium across crude, rates, and inflation expectations, with risk assets under sustained pressure until a credible resolution path emerges. The next two weeks will tell us which world we are in.