Oil Is the War

WTI above Brent, Hormuz still shut, and the forward curve is dreaming.

Trump gave Iran 10 days. That was a week ago. Yesterday he reminded everyone: 48 hours left on the clock. Tehran's response: no.

Five weeks ago, when US and Israeli jets hit Iran on February 28, the market priced a surgical air campaign. Two weeks, maybe three. Hormuz reopens. Oil spikes and fades. Back to business.

We said no.

Our call from Day 1: this war escalates before it de-escalates eventually. The most likely path is boots on the ground followed by a long, grinding conflict. Hormuz stays disrupted far longer than anyone wants to model. We laid out the logic in our duration framework, our Hormuz pricing model, and our war variable analysis. The core thesis: Iran doesn’t need to win. It just needs to make the war expensive enough that Washington looks for an exit. And the exit won’t come with a clean reopening of the strait.

Five weeks later, every part of that call is being validated.

Hormuz is still shut. Brent closed around $110. The Pentagon is preparing for weeks of ground operations. Trump’s war aims have drifted from “denuclearization” to “back to the stone ages.” He still can’t define what victory looks like.

Ground troops are the escalation climax we’ve been tracking. Marines and paratroopers are staging in theater. The moment is close.

But here’s what matters more than the next airstrike or the next ultimatum: oil.

Oil is not a side effect of this war. Oil is the war. Equities, bonds, crypto, the Fed, your grocery bill — all downstream. Get the oil call right and the rest follows. Get it wrong and nothing else you do matters.

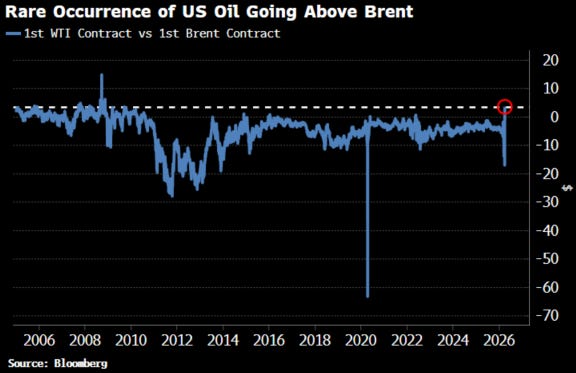

WTI just settled higher than Brent for the first time since 2022. That got everyone’s attention.

Good. It should.

WTI Above Brent: What Everyone Is Asking

April 2. WTI settled at $111.54. Brent settled at $109.03. A $2.51 WTI premium, the widest since 2009.

Two weeks earlier, WTI was trading at a big discount to Brent.

Everyone wants to know what happened. Here’s the short version and the real version.

The Short Version: Contract Timing

WTI’s front month delivers in May. Brent’s front month already rolled to June. When supply is this tight, one month earlier = pay more. WTI just happens to deliver sooner.

Adi Imsirovic, 35-year oil trading veteran now at Oxford, said buyers are paying almost $30/barrel more to take Brent cargoes a month early, on top of historically high shipping and insurance costs. In 35 years, he’s never seen anything like it.

That’s the mechanical explanation. It’s correct. It’s also incomplete.

The Real Version: The Curve Is Moving

The WTI-Brent convergence isn’t just a front-month quirk. Bloomberg flagged that it’s visible across multiple contract months, all the way down the strip. The entire curve is repricing.

Why?

Asian demand rotation.

Asian refiners bought ~10 million barrels of US crude for May loading in late March. Another ~8 million the week before. Kpler forecasts US-to-Asia exports hitting 1.7 million barrels/day in April, up from 1.3 million in March. China, South Korea, Japan, Exxon’s Singapore refinery. Everyone is buying American barrels because that’s what’s available.

Hormuz is shut. Murban crude, Abu Dhabi’s flagship and closest substitute to WTI, is gone from the global market. WTI is now the world’s swing barrel.

This isn’t a panic buy. This is a flow regime change.

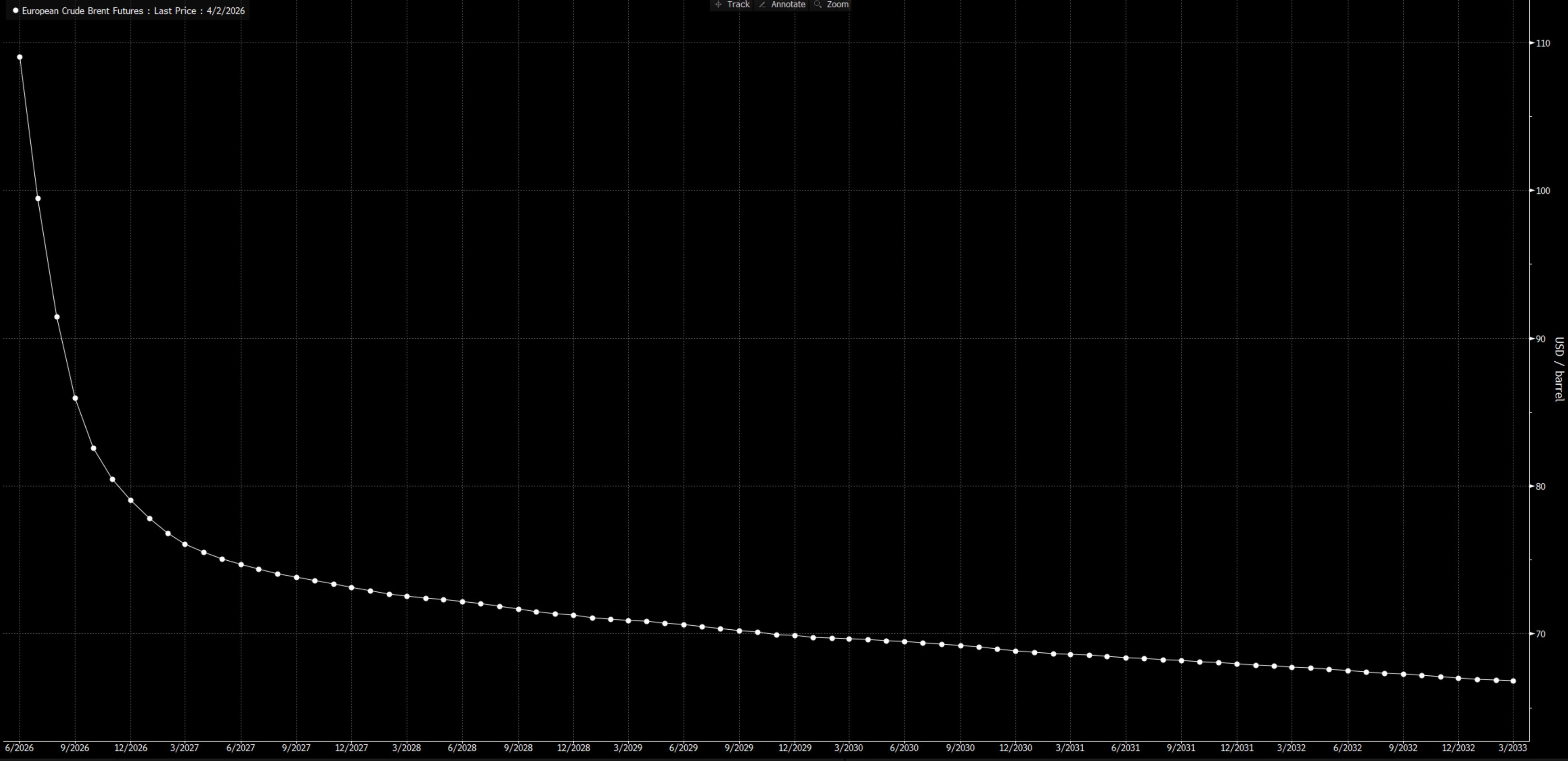

Now look at the forward curve.

The curve is saying: this is temporary. Back to normal by Christmas.

Our read: the curve is dreaming.

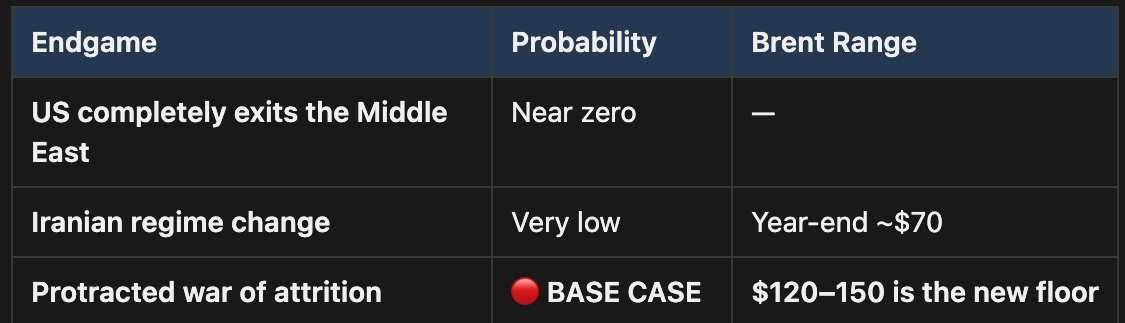

Three Endgames. One Base Case.

We laid this framework out in our Weekly Signal Playbook. Nothing has changed since. If anything, the base case has gotten stronger.

There are only three ways this war ends:

Endgame 1 is politically impossible. Endgame 2: the terrain, force requirements, and guerrilla dynamics all argue against it. Iran is three times the size of Iraq, twice the population, and the mountains don’t forgive. This isn’t 2003.

Endgame 3 is the base case, and by a wide margin. A long grind means Hormuz stays disrupted. Oil stays elevated. Structurally, not temporarily. The forward curve is heavily mispricing this.

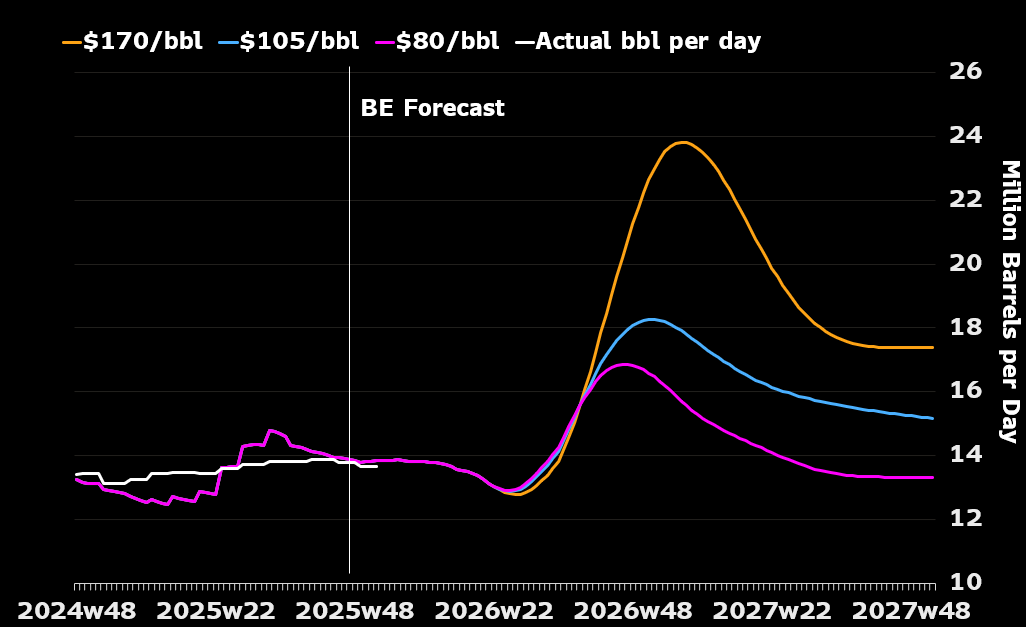

Here’s the part most people miss: if we look at the oil industry alone, a prolonged war might actually serve US strategic interests. Middle Eastern production capacity gets destroyed. Global buyers pivot to North American energy because there’s nothing else left. And higher prices? They incentivize US producers to ramp output (more rigs, more shale). Look at the chart below: every major price spike in history triggered a US production surge within 12–18 months.

The only cost the US needs to manage is domestic: keeping gas prices from staying above $4/gallon long enough to trigger political backlash. That’s a pain threshold, not a war-ending condition.

The Math

Brent at $110 with Hormuz shut is not the ceiling. It’s the starting point. Under our base case, $120–150 is where this settles for as long as the strait stays closed.

Every week that passes depletes inventories. UBS: global stocks hit their five-year average at end of March. That was before the latest round of escalation. Macquarie: $200 if the war drags past June with Hormuz shut — 40% odds.

The prompt spread (the gap between the two nearest Brent contracts) blew out to $8.59/barrel. The market is paying an 8% premium for one month of earlier delivery. That’s 2008 levels of desperation.

2008 didn’t have 15% of global supply physically blockaded.

Every model, every curve, every year-end target on the Street is built on the same assumption: this ends. Hormuz reopens. Oil normalizes. Life goes back to the way it was.

Our bet: it doesn’t.

The back end of the curve hasn’t caught up.

The market has priced the war. It has not priced the war lasting.

Until Hormuz reopens, every dip in crude is a gift. That’s our position and we’re not hedging it.

Oil is node one. When boots hit the ground and there’s no quick victory — when the war settles into the long grind we’ve been calling since Day 1, the repricing won’t stop at crude. It will cascade through rates, currencies, equities, and credit, in that order. That’s where we’re going next.

Garrett’s Signal covers macro, war, and markets at the intersection where most analysis stops.

Um. WTI only settled above Brent because it's still tracking the May contract vs Brent that just rolled to the June contract.

We pay for the analysis which is awesome and you’ve been spot on with your predictions but tell us where the money is to be made. What’s the next trade ?