Priced as a Non-Event: The Xi-Trump Handshake

China People's Daily headline: "US-China relations cannot return to the past — but can have a better future."

The Market Already Made Its Call

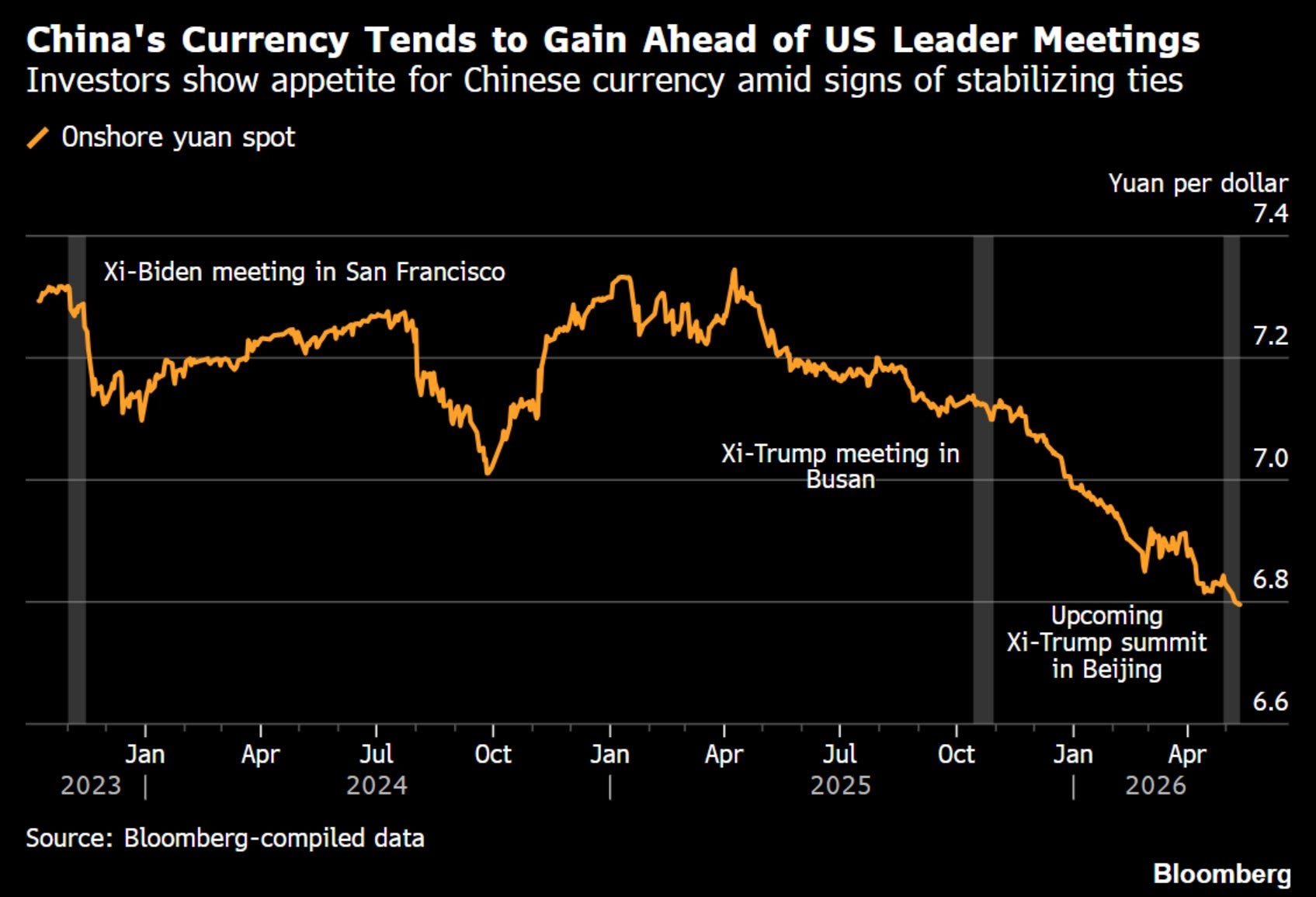

The Xi-Trump summit is priced as a non-event in last week’s ETF Compass. The S&P forward vol curve has no kink around May 14-15. FXI and ASHR — the two main China ETFs — sit at the bottom of the expensive-vol screen, meaning options on Chinese equities are as cheap as they’ve been in months. Translation: nobody is paying up to hedge this meeting. Priced clean is not the same as priced safe. The handshake has no convexity left in it — the path after does.

The base case for Thursday is the same script that’s run for nine years: chocolate cake, beautiful lines, a planeload of US CEOs, a Boeing order, an ag list, a handshake that risk assets celebrate for forty-eight hours.

But there is the other half of the trade. Per Barclays’ ETF Compass last week, SPY moved more than 1σ around four of the last five Xi-Trump face-to-faces — and the China ETFs (KWEB, FXI, ASHR) moved harder. Read it as direction, not promise: the event has been priced clean and historically traded dirty. Consensus this time isn’t wrong — it’s just being bought at zero cost. The interesting question isn’t Thursday’s handshake. It’s the four-to-eight weeks after, when the script reliably reverses. That’s where the tail sits.

Chocolate Cake, and a Thousand Reasons

April 6, 2017. Mar-a-Lago. Dinner.

Trump and Xi sit down together for the first time. Dessert: chocolate cake. Trump later told Fox it was “the most beautiful piece of chocolate cake you’ve ever seen.”

Just as Xi took his first bite, Trump leaned in and told him: we just fired 59 Tomahawks into Syria.

That’s the opening frame of US-China summit diplomacy. Sugar coating, plus steel. The sugar came from the Trump side itself: Ivanka’s five-year-old daughter Arabella Kushner, with her three-year-old brother Joseph, sang Mo Li Hua / Jasmine Flower (a traditional Chinese folk song) in Mandarin and recited the Three Character Classic (the classical Confucian primer every Chinese child grows up with) for Xi. A deliberate charm gesture from Trump’s family to his guests. The steel was the host’s: mid-dessert, Trump leaning across the table to tell Xi about 59 cruise missiles.

Nine years on. This Thursday, the upcoming Xi-Trump meeting — this time on Beijing’s turf. No Mar-a-Lago dessert table.

Five Meetings, Four Episodes. Same Playbook.

Put the opening lines and closing results of the past five summits side by side. This isn’t coincidence. This is a machine.

April 2017 | Mar-a-Lago → November 2017 | Beijing State Visit

April 2017, Mar-a-Lago. Xi opens: “We have a thousand reasons to make China-US relations work. Not a single one to break them.” Trump closes: “We’ve made tremendous progress. Our relationship is outstanding.” The 100-day action plan gets announced.

Seven months later, Trump returns to Beijing on a state visit. Xi, at the state dinner: “China-US relations face limited challenges, but boundless potential for growth.” Trump, inside the Great Hall: “I don’t blame China. Who can blame a country for taking advantage of another country for the benefit of its citizens?” An official dinner inside the Forbidden City — described at the time as the first such treatment for a foreign leader since 1949. Deliverables totaling $253.5 billion: a 300-jet Boeing order (~$37B), long-dated LNG, bulk ag purchases. Highest protocol. Full props package. The closest analog to what we’re watching this Thursday.

Then the trade war started. March 2018, Section 232 steel and aluminum. July 2018, the first $34B in China tariffs hit. May 2019, the rate on $250B of Chinese goods got jacked to 25%. Total escalation inside 14 months.

December 2018 | Buenos Aires

Trump walks out of dinner: “An amazing and productive meeting, with unlimited possibilities.” On the plane he adds: “Our relationship is incredible.”

90-day tariff truce announced.

Three days later (three, not three weeks) Trump tweets: “I am a Tariff Man.”

May 2019: tariffs jump from 10% to 25%. The rest you know.

June 2019 | Osaka G20

Xi opens with ping-pong diplomacy — the 1971 small ball that, in his words, “played a big role in moving world events.”

Trump replies: “We’re right back on track.” Pauses the $300B tariff round. Soft pass on Huawei.

Five weeks later, on August 1, the new $300B in tariffs lands. Huawei stays on the US Commerce Department’s Entity List — the export-ban list that cuts a foreign firm off from American semiconductors, software, and IP. Not one day off.

October 2025 | Busan

Xi: “We do not always see eye to eye. This is normal.”

Trump on Air Force One: “Zero to ten, ten the best. I’d give this summit a 12.”

On rare earths: “There is no road block at all on rare earth. Hopefully that will disappear from our vocabulary.”

Two months later, a US carrier group rolls into the Caribbean, pointed at Venezuela. Four months later, the Iran war breaks out and Hormuz goes functionally dark. Stated reason: counter-narcotics, counter-terror. Real effect: two of China’s energy anchors squeezed at the same time, one in Latin America and one in the Middle East. Whether or not Washington calls it containment, the chessboard reads the same way.

After “12 out of 10”

Busan was late October 2025. Inside four months: US naval forces enter the Caribbean in December under a “counter-narcotics” banner, aimed at Venezuela. February 2026, war on Iran. Hormuz functionally closed. March 2026, Venezuelan crude exports effectively shut in.

Venezuela ships China roughly 400,000 barrels a day of heavy crude — about 4-5% of Chinese seaborne imports, most of it disguised in customs data as Brazilian or Malaysian — and is Beijing’s single largest oil-and-debt exposure in Latin America. Iran, once you re-attribute the so-called “Malaysian” barrels (Malaysia ships China roughly twice as much crude as it actually produces), is among China’s three biggest crude suppliers, the Middle East anchor of the Belt and Road, and a key node for yuan-denominated oil settlement. Together they’re roughly 15% of China’s real crude imports. But the real weight isn’t in the barrels.

Put those two moves side by side. Hit Iran, and you cut China’s Middle East anchor. Squeeze Venezuela, and you cut China’s Latin America exposure. This is one chessboard. The game isn’t over.

But there’s a reversal no one fully priced: the war meant to pressure China has also constrained Washington. When you are the co-belligerent in a Middle East conflict, energy markets are rattled, and your own Court of International Trade — the federal court that adjudicates tariff disputes — just shook the legal foundation of your current tariff workaround (even if the tariffs themselves haven’t disappeared yet), you walk into Beijing needing stability as much as your counterpart does. Trump arrives in China with a thinner hand than he had in Busan. Xi knows it. That’s what “emboldened” looks like — not louder, just more patient.

Beijing Understands the Game

Five handshakes in, China’s leadership has finished a full cognitive cycle on Trump.

2017 China: treat him as a new president. Full charm offensive in return. “A thousand reasons.” State visit invite. Forbidden City state dinner. $253.5 billion in deliverables.

2018-2019 China: start to realize the man reverses course the moment he lands back home. A “commitment” to him isn’t political credit. It’s marketing content. The line circulating quietly in Beijing’s diplomatic circle back then: the better the meeting with Trump, the harder the crash after.

2025 Busan China: Xi’s line, “We do not always see eye to eye. This is normal”, was not diplomatic boilerplate. It was a categorical statement. Translation: I have accepted that you will renege, and we will still talk. That sentence has never come out of China’s top leader’s mouth before.

2026 May China: complete mental shift. The goal isn’t to build the relationship. The goal is managing uncertainty.

Beijing’s own flagship mouthpiece confirmed the frame this morning. A long-form People’s Daily front-page commentary on the morning of May 13, signed by Guo Jiping (the paper’s house pen-name reserved for major foreign-policy set-pieces, distinct from the more frequent Zhong Sheng column), ran under the headline: “US-China relations cannot return to the past — but can have a better future.” That’s not boosterism. That’s managed expectations at official register. The line buried mid-text: “dialogue is better than confrontation, cooperation is better than zero-sum, stability is better than chaos.” Three comparisons, in descending order of ambition. Published to a domestic audience, on the morning of the summit. Beijing almost never runs expectation management in public before a summit. This time it did.

Trump’s strongest asset was never tariffs. It’s unpredictability. That is the one variable no counterparty who treats commitment as political credit can hedge. Beijing has now internalized that variable into its own reaction function. The internal framing of this summit is defensive.

So What Is Beijing Actually Doing This Week

If you accept the premise that Beijing no longer believes Trump, every visual symbol of this summit reassembles.

The potential 500-jet Boeing order and the ag purchase list. This isn’t really “a public stake Trump can’t walk away from.” Given his style, he can pivot any time and blame China. The order doesn’t lock him in. He won’t even pretend to care. But it is a deal that fits Beijing’s diplomatic profile: quantifiable purchases, traded for controllable stability. If what the US side wants right now is tariff de-escalation and a posture of “winning,” this is a price Beijing will pay, and they’ll happily hand Trump the off-ramp. Short of a full surface blow-up, this kind of shopping list has never been a real problem for China.

Beijing even pre-loaded Trump’s victory narrative. Xi first offered that framing at Busan; People’s Daily put it back on the front page on the morning of the summit: “China’s development and Trump’s ‘Make America Great Again’ are not mutually exclusive — China and the US can fully achieve mutual success and shared prosperity.” That sentence isn’t a concession. It’s a face-saving ramp, built in advance, so Trump can walk away claiming a win without Beijing giving up anything structural. The other side of the table has stopped being a counterparty. It’s become a co-author of Trump’s press release.

Musk, Cook, Fink, Fraser, Ortberg in tow. These CEOs are US capital’s dependence on the China market, in human form. Beijing inviting them in puts “we still want to do business” on the table in plain view.

But one thing has to be clear. The price tag here only buys “stability in trade and tariffs.” It does not come close to buying “China cooperating with the US on Iran.” China’s position on Iran is strategic. Energy. Geopolitics. Yuan-based oil settlement. None of that gets traded away for a Boeing order. If Washington actually wanted China to lean on Tehran in a decisive way, the corresponding ask back would have to be the things China has wanted for years and the US has refused to give. Chips. Real loosening of export controls. A defined boundary on Taiwan. None of those are on the table right now.

On top of that, after the US Court of International Trade’s May 7 ruling, the legal foundation of the tariff tool itself is shaky. The US hand is getting thinner. What Beijing is willing to give right now is a courtesy. What Beijing won’t give, the US doesn’t have the cards to force.

Xi pre-saying it himself: “We often don’t see eye to eye, and that’s normal.” That’s expectation management, delivered ahead of the room. Don’t romanticize this summit, in markets or at home. Before a summit, Beijing only ever puts out positive talking points. Not this time.

Putin lands in Beijing next week. Days after Trump leaves, Putin arrives. This is for Trump’s benefit: whether you show up or not, the other side of the line is already there.

The whole event has stopped being a negotiation. It’s a risk management ritual.

What’s Likely to Be Announced Thursday

Washington’s wish list has been summarized in five words by a CSIS senior adviser: Boeings, Beans, Beef, Board of Trade, Board of Investment. Three are purchases. Two are committees. Note which category is missing: enforcement.

Likely deliverables: a 737 Max order that could run as high as 500 jets. An ag purchase list (soy, pork, beef, poultry). A 12-month rare earth export extension. A counter-narcotics framework (officially packaged as fentanyl cooperation) — both sides already announced a cross-border drug network takedown days before the meeting, and the US extradited a fugitive to China, giving both governments a zero-cost win to attach their names to. Something called a “US-China Trade Commission,” a quasi-cabinet-level working group designed to handle trade issues without touching national security questions — i.e., a mechanism for kicking every hard problem six months down the road. (The US Trade Representative already pre-downplayed it before Trump landed.)

Unlikely to be structurally resolved: a real pause on Taiwan arms sales. Any substantive loosening of AI chip export controls. Any Chinese concession on Iran. A reopening pathway for Venezuelan oil.

Both sides will smile. Markets will rip. Trump will say “13 out of 10.” Xi will say “China-US relations enter a new phase.”

And then.

The Tail: Where the Cheap Hedge Sits

This is the part the non-event pricing leaves on the table. Not a forecast. Just an observation about where the asymmetry lives.

If the last five summits are any guide, the first crack tends to land four to eight weeks after the handshake — usually on Trump’s Truth Social. The form is familiar: “China is not following through on agricultural purchases,” or “China is helping Iran rebuild.” Then the toolkit comes out.

What’s different this round is the toolkit itself. Per The New York Times, the US Court of International Trade ruled that Trump’s 10% global tariff on most imports is illegal. His space to launch a trade war without explicit Congressional authorization has shrunk.

So if the script does reverse, it probably won’t use tariffs. It will reach for the dirtier stuff:

Entity List additions — Commerce Department export bans on specific Chinese firms (the Huawei treatment)

SDN sanctions — Treasury’s Specially Designated Nationals list, the harshest financial sanction the US issues; cuts a name out of the dollar system entirely

Tightened chip and semiconductor export controls

Secondary sanctions on Chinese refiners buying Iranian or Venezuelan crude

Tariffs are blunt. These are scalpels. The market is numb to the first. It has not really priced the second.

And this time, Beijing won’t pretend to be surprised. The reaction function is already loaded — rare earth export quotas snap tighter, a US company in China suddenly walks into an antitrust review, the Putin visit gets upgraded. All pre-staged.

None of this needs to happen. The base case is still that Thursday is theater and the weeks after are quiet enough. The point is just that the tail isn’t expensive right now, and five handshakes of history suggest it’s worth keeping a line on.

Closing

When Trump lifted that chocolate cake at Mar-a-Lago in 2017, the market thought it was the beginning. Nine years later, we can see it was just page one of the script.

Every China-US summit, the market re-prices “political credit.” Every re-pricing turns out to be wrong.

Because political credit, in this relationship, has never existed.

This Thursday, you’ll see a beautiful handshake. You’ll hear beautiful lines. Markets will rip. CEOs will smile. The planes will be announced.

The meeting is the relief trade. The post-meeting implementation window is the risk.

Enjoy it. Just don’t hold it.

The market is right that Thursday is a non-event. The cheap question is what shows up four weeks after.

Garrett’s Signal · May 2026 · Xi-Trump Series #1

No news. No noise. Just signal.

in short the summit could be a sell news event, with a relief rally at first with the music stopping after the summit?