Weekly Signal Playbook · Apr 16 — Trading the Calendar

War, Oil, and the Calendar That Doesn't Negotiate — 12 Positions, Full Framework Update

PAID SUBSCRIBER CONTENT — This is the full Weekly Signal Playbook with triggers, sizing, and invalidation.

Updated Apr 16. The market got bored of Iran. The physical shortage didn’t.

Trading the Calendar

The market is bored of Iran.

Four TACOs. A ceasefire that changed nothing. One 21-hour marathon in Islamabad that produced nothing. A leaked framework. A blockade announcement. Trump saying “close to over” on Fox, then sending 6,000 more troops the same week. The market has seen this movie so many times it stopped watching. S&P erased every point it lost since the war started. Nasdaq hit a record. BTC touched $76k. Oil dropped back to $95.

Iran fatigue. We get it.

That’s exactly when the real shortage hits. Not when the headlines get worse. When everyone stops watching.

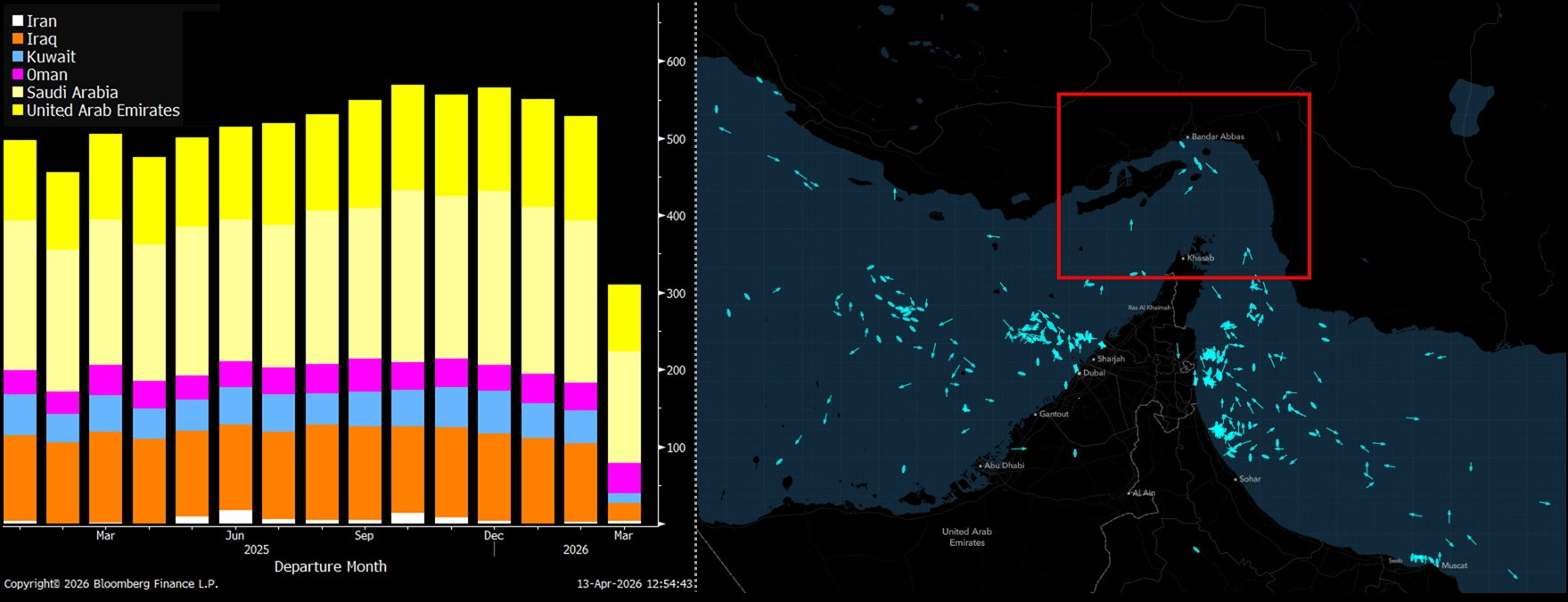

Seven weeks in. From day one we said the market was mispricing duration. That Hormuz had no quick fix. That every ceasefire was an intermission, not an ending. Seven weeks later, the strait is still shuttered. And the data coming out of the physical market this week is the most alarming since the war began.

Last week in the North Sea, the most important physical crude market on earth, traders submitted 40 bids for cargoes. Four were met by offers. Forty to four. By Wednesday, that ratio had flipped: seven offers, two bids, both withdrawn. That’s not a signal that the shortage is over. It’s a signal that $144 physical crude is already destroying demand at the margin. The physical market is still in crisis. It’s just starting to price its own pain.

Trafigura and Gunvor were bidding $22 a barrel above Dated Brent for late April and early May delivery. Nigerian crude premiums hit $25 a barrel over benchmark. Before the war, that number was less than $3.

Dated Brent hit $144 on April 8, hours before the ceasefire was announced. Brent futures traded at $109 the same day. A $35 gap. Normal is $1 to $2. That gap is the physical market screaming what the futures market refuses to hear.

ADNOC’s Sultan al Jaber put it plainly last week: “The final cargoes that transited Hormuz before the conflict are now arriving at their destinations. The 40-day gap in global energy flows is truly exposed.” (The “40-day gap” refers to when most pre-war barrels have been consumed. JPMorgan’s April 20 estimate marks when literally the last tanker clears.)

JPMorgan’s oil team confirmed the math. The last tanker to clear Hormuz on February 28 reaches its destination around April 20. After that, every pre-closure barrel on the planet is gone. The developed world’s oil stockpiles could hit the minimum levels needed to keep refineries running by early May. Asian refiners cut only 2 million barrels a day (far less than expected). The gap is being filled by burning through reserves and killing demand. That’s not a solution. That’s a countdown.

Look at what’s happening on the ground. Japanese refiners are booking smaller ships to squeeze through the Panama Canal faster. Chinese refiners pushed Vancouver crude imports to a record this month. India doubled Venezuelan crude purchases in the first week of April. Traders at Asian refineries told Bloomberg they’re “no longer focused on price, simply seeking barrels for energy security.” Energy Aspects warned that US exports are running so high there may not be enough crude left for American refineries.

US gasoline inventories are at the smallest in 16 years. Jet fuel and diesel above $200 a barrel.

The market is pricing a ceasefire. The physical market is pricing a siege.

The Negotiation Gap

The physical shortage is driven by Hormuz. Hormuz is driven by the war. So we still have to read the room.

Our read hasn’t changed. We don’t think a deal gets done.

The single biggest obstacle is uranium. Iran’s foreign ministry said last week that the right to enrich is non-negotiable. The “level and type” are open to discussion, but the principle is off the table. On the other side, Israel’s defense minister said all highly enriched uranium must be physically removed from Iran. Trump said he’s unhappy with reports that the US proposed a 20-year moratorium on enrichment, calling it insufficient. After 21 hours of talks in Islamabad, Vance left empty-handed. Trump posted that Iran was “very unyielding as to the single most important issue.”

This is not a gap you close with another round of talks. Both sides are asking for things the other side can’t give.

Then there’s Hormuz. For Iran, it’s the only card that makes the US feel real pain. First time in decades that leverage has been tested, and it worked. For America, the stakes go beyond oil prices. We wrote about this in Hormuz Is the Battlefield and Trump Blinked Again: free passage through the strait is what backs the dollar’s security guarantee. Seven weeks of closure have done more to erode that premium than any BRICS summit ever could. Both sides know what Hormuz represents. Neither can afford to give it up.

So here are the three paths from here.

Path one: a deal. There are two versions. In the first, Iran gives up enrichment rights and Hormuz leverage. Nothing in the past seven weeks suggests either side is close to that trade. In the second, the US concedes some form of Iranian control over Hormuz. Oil drops short-term. But that’s not peace. It’s a transfer of oil wealth and strategic power from the Gulf states to Iran. Saudi and the UAE won’t accept that quietly. You’re trading one conflict for another. And a Saudi-Iran power struggle over Hormuz revenue would keep oil elevated for years, not weeks. Either version of a deal is the least likely outcome.

Path two: the war resumes. The ceasefire expires April 22. The Pentagon just sent 6,000 more troops on the USS George H.W. Bush. Ground operations are still on the table. Iran’s military commander called the US blockade “a prelude to a breach of the ceasefire” and threatened to shut down all exports in the Gulf, the Sea of Oman, and the Red Sea. If fighting restarts, oil goes parabolic.

Path three: the stalemate drags on. Another extension. More talks. No resolution. Hormuz stays functionally closed. This is the most likely outcome. It’s also the one the market is least prepared for, because it means the shortage doesn’t spike and crash. It grinds. Week after week. Inventories drawing down. Refiners cutting runs. Prices staying elevated with no catalyst for relief.

All three paths lead to higher oil. One is a spike. One is a slow bleed upward. And even the “deal” path, if it hands Iran the strait, creates a new instability that reprices the entire Middle East. There is no path back to $70 oil from here.

Even in that least likely scenario, restoring normal shipping takes 6 to 8 weeks minimum (Hapag-Lloyd’s CEO said this on day one of the ceasefire). Insurance markets are still frozen. Lloyd’s hasn’t reinstated coverage. 800+ vessels remain trapped in the Gulf.