Weekly Signal Playbook · Mar 17 — 10 Cross-Market Signals

The Convergence Trade

PAID SUBSCRIBER CONTENT — This is the full Weekly Signal Playbook with triggers, sizing, and invalidation.

Companion piece to the free article: The Three-Body Problem: When AI, Debt, and War Collide

Regime Assessment

🔴 Current Regime: RISK-OFF · Convergence Phase

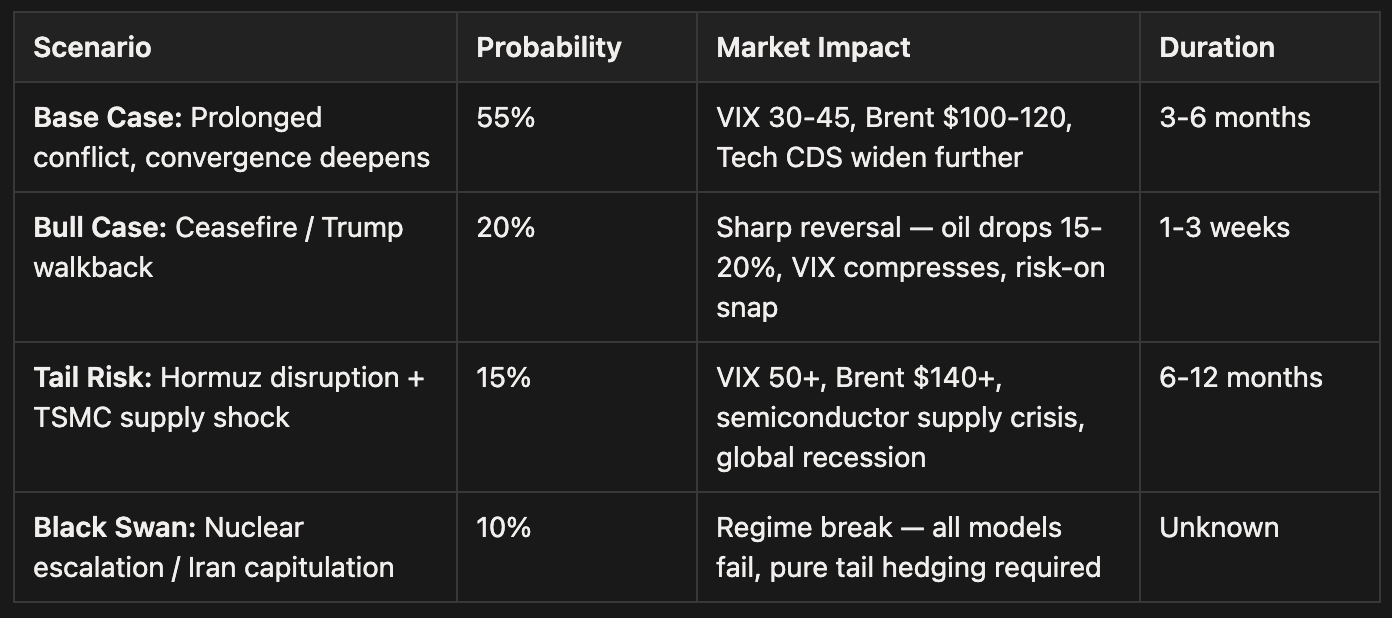

Three previously independent volatility streams (AI/software debt, energy/geopolitics, semiconductor supply chain) synchronized on March 10. This is the first time this cycle that all three are moving in the same direction simultaneously. Historical analog: early 2022 Russia-Ukraine, but with structurally worse supply-side dynamics and a depleted US policy toolkit.

Regime Shift Probability Table:

Macro Portfolio: Long / Short Framework

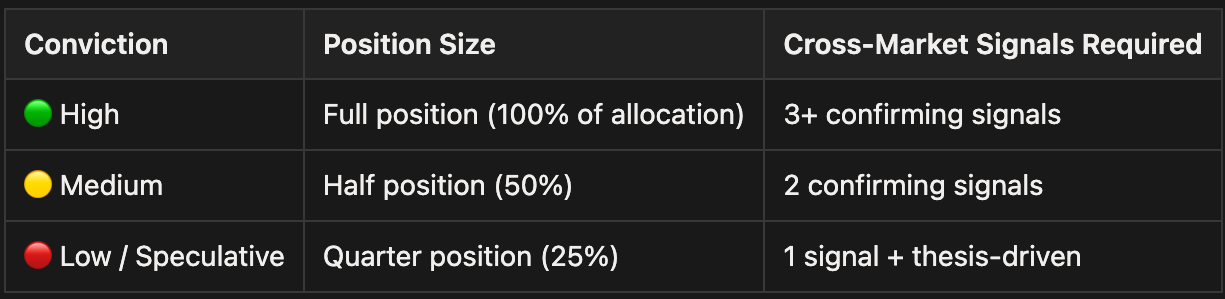

This portfolio is built on the convergence thesis. Every position is justified by at least two cross-market signals, and every position has an explicit invalidation condition.

Conviction Sizing Guide

LONG POSITIONS

1. Crude Oil / Energy Complex 🟢 High Conviction

Thesis: Duration is the pricing variable. Supply dynamics are structurally tighter than 2022. SPR depleted. OPEC spare capacity low. Restocking takes 2+ months.

Vehicles:

Long Brent crude (direct)

Long PetroChina (0857.HK) — outperforming MSCI Asia, strategic stockpiling beneficiary

Long China state-owned oil names — Russian pipeline infrastructure plays

Cross-Market Confirmation:

WTI / 10Y UST ratio at all-time highs → energy inflation winning

Brent / WTI spread widening → Hormuz premium live

SC-WTI spread parabolic → China import cost confirming tightness

Triggers:

Add: Brent breaks above $100 with OVX staying elevated above 60

Add: SC-WTI spread exceeds 250

Reduce: SPR emergency release announced > 50M barrels

Invalidation: Brent falls below $75 AND Brent/WTI spread compresses below $2 → geopolitical premium evaporating

2. China New Energy vs. Global Peers 🟢 High Conviction

Thesis: The energy shock accelerates the global shift toward renewables. China dominates solar, wind, batteries, and EVs. Europe and Japan/Korea are structurally disadvantaged energy importers. The relative trade is more powerful than the absolute trade.