Who Breaks First?

The war is in Iran. The fractures are everywhere else.

On March 14, North Korea fired a ballistic missile into the Sea of Japan. The same week, satellite tracking data confirmed approximately 1,200 Chinese fishing vessels holding formation in two parallel lines in the East China Sea — the third coordinated massing since December, each further east, each closer to Japan. The same day, the Pentagon confirmed that 2,500 U.S. Marines aboard USS Tripoli — the 31st Marine Expeditionary Unit, previously stationed in the Pacific — are redeploying to the Middle East.

The Pacific fleet is thinning. Pyongyang is testing the vacancy. Beijing’s maritime militia is mapping it.

None of this is about North Korea. None of this is about fishing boats. All of it traces back to one waterway — 33 kilometers wide, fourteen days closed — and to the chain of consequences that closure has set in motion.

The Strait of Hormuz is not just an oil chokepoint. It is the load-bearing wall of American global security architecture. Remove it, and the stress doesn’t stay in the Middle East. It propagates — through energy markets, through alliance commitments, through the military force posture that underwrites every American security guarantee from Seoul to Taipei to Tallinn. The missile in the Sea of Japan and the fishing boats off Okinawa are the first observable evidence of that propagation.

The question is not whether oil stays above $100 — it almost certainly goes higher, and institutional forecasts range from $95 (EIA, if Hormuz reopens within weeks) to $120–$150 in Barclays’ tail scenario, with Bernstein’s demand-destruction threshold at $155. The real question is which countries, which alliances, and which political systems break first under the compounding weight of energy scarcity, security vacuum, and diplomatic fragmentation — and who is positioned to fill the void.

This is that map.

I. Fourteen Days: $72 to the Abyss

The timeline is worth reading carefully, because each episode follows the same pattern: a policy signal compresses the price spike, physical reality reasserts within 48 hours.

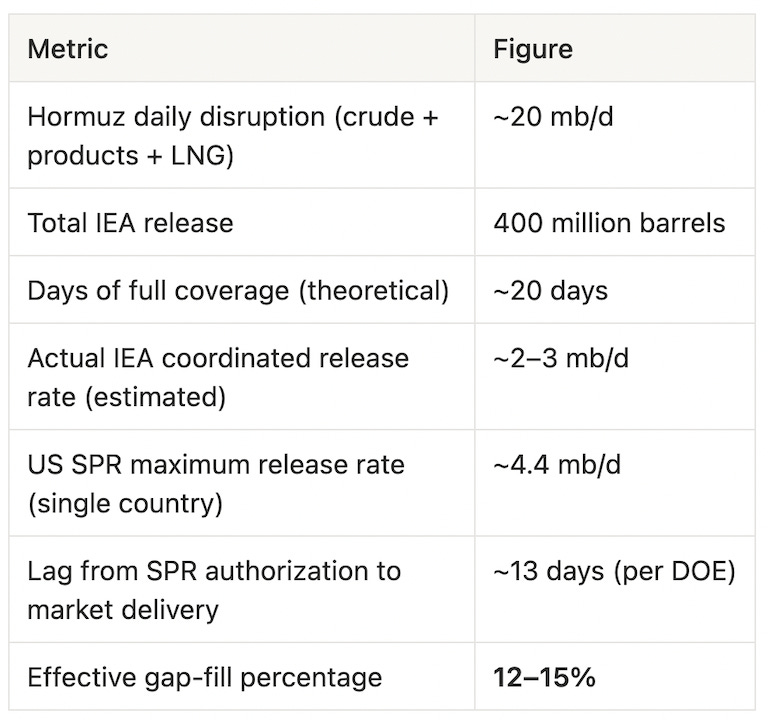

Days 1–4 (Feb. 28 – Mar. 3). US and Israeli forces strike Iran. Brent crude jumps from approximately $72 to $85 — an 18% move in four days. Iran retaliates immediately: missile and drone attacks on US military bases in the Gulf, on Saudi Arabia’s Ras Tanura refinery (capacity: 550,000 b/d), and on Qatar’s LNG export facilities. European natural gas prices rise 48% in two sessions. The Strait of Hormuz, through which roughly 20% of global oil and LNG transits daily, is effectively closed.

Days 5–7 (Mar. 4–6). Trump announces US naval escorts and trade insurance guarantees for Gulf shipping. Markets briefly exhale. Then CENTCOM confirms it has destroyed 16 Iranian mine-laying vessels — meaning the mines are already in the water. More than 200 vessels report GPS signal anomalies near Hormuz. The “all-clear” was not an all-clear.

Days 8–10 (Mar. 7–9). Saudi Arabia, the UAE, Kuwait, and Iraq are forced to curtail output — collectively, approximately 6.7 mb/d — because the Strait is their only meaningful export route and storage is approaching capacity. Brent trades intraday at $119.50. That is a 66% move from the pre-war close of $72.

Day 10–11 (Mar. 10). Trump tells Fox News the conflict will end “very soon” and signals potential sanctions waivers on oil and gas. WTI drops more than 10%, briefly trading below $80. On the same day, the Pentagon describes March 10 as “the most intense day of strikes since the conflict began.” The policy signal and the physical reality are pointing in opposite directions. Both cannot be true. Markets spent the next 48 hours discovering which one was.

Days 12–14 (Mar. 11–13). The IEA announces the largest coordinated strategic reserve release in its history: 400 million barrels. WTI spikes briefly, then falls — then climbs again within hours. On March 12, two tankers are struck in Iraqi waters. Oman clears the Mina Al Fahal export terminal on an emergency basis. By the close of March 13, Brent settles near $101. WTI at $99.30.

Day 14 (Mar. 13–14). Four developments land within 24 hours and shift the conflict’s trajectory. First, Trump announces US forces have “obliterated” military targets on Iran’s Kharg Island — the terminal handling roughly 90% of Iran’s oil exports — and warns that the island’s oil infrastructure could be next. Hours later, the Pentagon confirms the deployment of the 31st Marine Expeditionary Unit and the amphibious assault ship USS Tripoli, with approximately 2,500 Marines, from Japan toward the Middle East. A Marine Expeditionary Unit is purpose-built for amphibious landings and securing maritime chokepoints. CENTCOM requested the force because “part of the plan for this war was to have Marines available to provide options for use,” per a US official cited by NBC News. The Tripoli was spotted by commercial satellites near the Luzon Strait, putting it roughly 7 to 10 days from the waters off Iran. Then, on March 14, North Korea fires approximately 10 ballistic missiles into the Sea of Japan — its largest single salvo of 2026. The same day, AFP reports 1,200 Chinese fishing vessels detected in a third coordinated formation in the East China Sea, further east than the December and January events, closer to Japanese waters.

This is a qualitative shift on two axes. For 13 days, the US prosecuted an air-only campaign while Hormuz remained closed. The MEU deployment signals that Washington is preparing to physically contest the Strait — not merely bomb around it. Defense Secretary Hegseth made the intent explicit: “That’s not a strait we’re going to allow to remain contested.” But the MEU is the Pacific’s only forward-deployed rapid-response force — and within hours of its departure, both Pyongyang and Beijing’s maritime militia moved to test the vacancy. The Hormuz crisis is no longer contained to the Gulf.

The pattern across 14 days is unambiguous: every policy response buys 24 to 48 hours. Physical reality reasserts itself within hours of every announcement. And now, the consequences are propagating beyond energy markets into the global security architecture that Hormuz underwrites. But as of Day 14, the question has expanded: the crisis is no longer only about supply math. It is about whether the US can physically reopen the Strait before its allies’ reserves run dry — and what that attempt will cost.

II. The SPR Illusion

The IEA’s 400-million-barrel release is the sixth coordinated reserve drawdown in the agency’s 52-year history, and by a wide margin the largest. It more than doubles the 182 million barrels released after Russia’s invasion of Ukraine in 2022. The US alone committed 172 million barrels — roughly 43% of the total — with deliveries beginning next week over an estimated 120-day drawdown period, per the Department of Energy.

It sounds decisive. The math is not.

The gap-fill figure is the one that matters. At realistic coordinated release speeds — not the headline barrel number, but the actual daily flow — the IEA’s historic intervention covers somewhere between 12 and 15% of the supply disruption, per Reuters reporting on the release mechanics. It cannot fill the rest. Nothing can except reopening the Strait.

Gary Ross, founder of Black Gold Investors and among the most accurate analysts on Hormuz mechanics, put it plainly:

“This situation is not manageable without demand destruction and much higher prices, unless the conflict ends.”

The market agreed. WTI dropped sharply on the IEA announcement, then recovered the same day. As NBC News noted, the coordinated release “failed to bring down prices.” The signal was political. The shortfall is physical.

A further structural limit: the SPR release relieves pressure on liquid crude inventories but does not touch LNG. Japan and South Korea’s most acute vulnerability — detailed below — is not oil. It is liquefied natural gas, for which no strategic reserve system comparable to the IEA oil mechanism exists.

III. The Saudi Pipeline Myth

Saudi Arabia is the only major Gulf producer with a theoretical bypass route: the East-West Pipeline, running from eastern oil fields to the Red Sea port of Yanbu, with a nameplate capacity of 7 mb/d. Saudi Aramco CEO Amin Nasser has confirmed the pipeline is being pushed toward maximum utilization. Twenty-seven VLCCs are reportedly en route to Yanbu. Loaded volumes at the port have already surged to a record 2.72 mb/d.

That number — 2.72 mb/d — is the real figure. Not 7 mb/d.

The gap between nameplate and actual reflects several hard constraints that analysts at Argus Media have catalogued:

The Yanbu terminal was not engineered to handle 7 mb/d of loading traffic. Berth capacity and pumping infrastructure impose a physical ceiling well below the pipeline’s theoretical throughput. The pipeline itself serves dual purposes — export contracts and feedstock supply for Aramco’s western refineries — meaning there is internal competition for the same capacity. And Red Sea insurance premiums have more than doubled under Houthi threat, compressing effective bypass further.

Per Argus Media: “Pipeline constraints and limited loading capacity mean the route can only partially offset the loss.”

Net effective bypass capacity: approximately 2.5 to 3 mb/d. Against a disruption of ~20 mb/d, the Saudi pipeline is covering roughly 15% of the gap. Add the IEA SPR at 12–15%, and you still have well over two-thirds of the supply shortfall unaddressed by any mechanism currently in operation.

A third pathway now exists in theory: US naval escorts forcing a partial reopening of the Strait. Treasury Secretary Bessent confirmed the plan on March 12, stating the Navy would begin escorting tankers “as soon as militarily possible.” But Energy Secretary Chris Wright was more candid the same day: “We’re simply not ready. All of our military assets right now are focused on destroying Iran’s offensive capabilities.” Wright estimated escort operations could begin by month’s end — the Wall Street Journal, citing two US officials, put the timeline at a month or longer. The constraint is not ships; it is that the mines are already in the water, and the US has no mature mine countermeasures force deployed in the region. Until the coastal anti-ship missile batteries are neutralized and the mines are cleared, escort is aspiration, not logistics.

IV. Who Breaks First

The supply shock is global. The breaking points are not simultaneous. Each country’s clock is ticking at a different speed, shaped by its import dependency, reserve depth, grid composition, and social tolerance for price pain. And as of Day 14, there is a new clock running alongside the others: the US military’s timeline to physically reopen the Strait, estimated at 2 to 4 weeks from now. The question “who breaks first” is now a three-way race between reserve depletion, diplomatic resolution, and military intervention. What follows is a country-by-country vulnerability ranking, from most exposed to least.

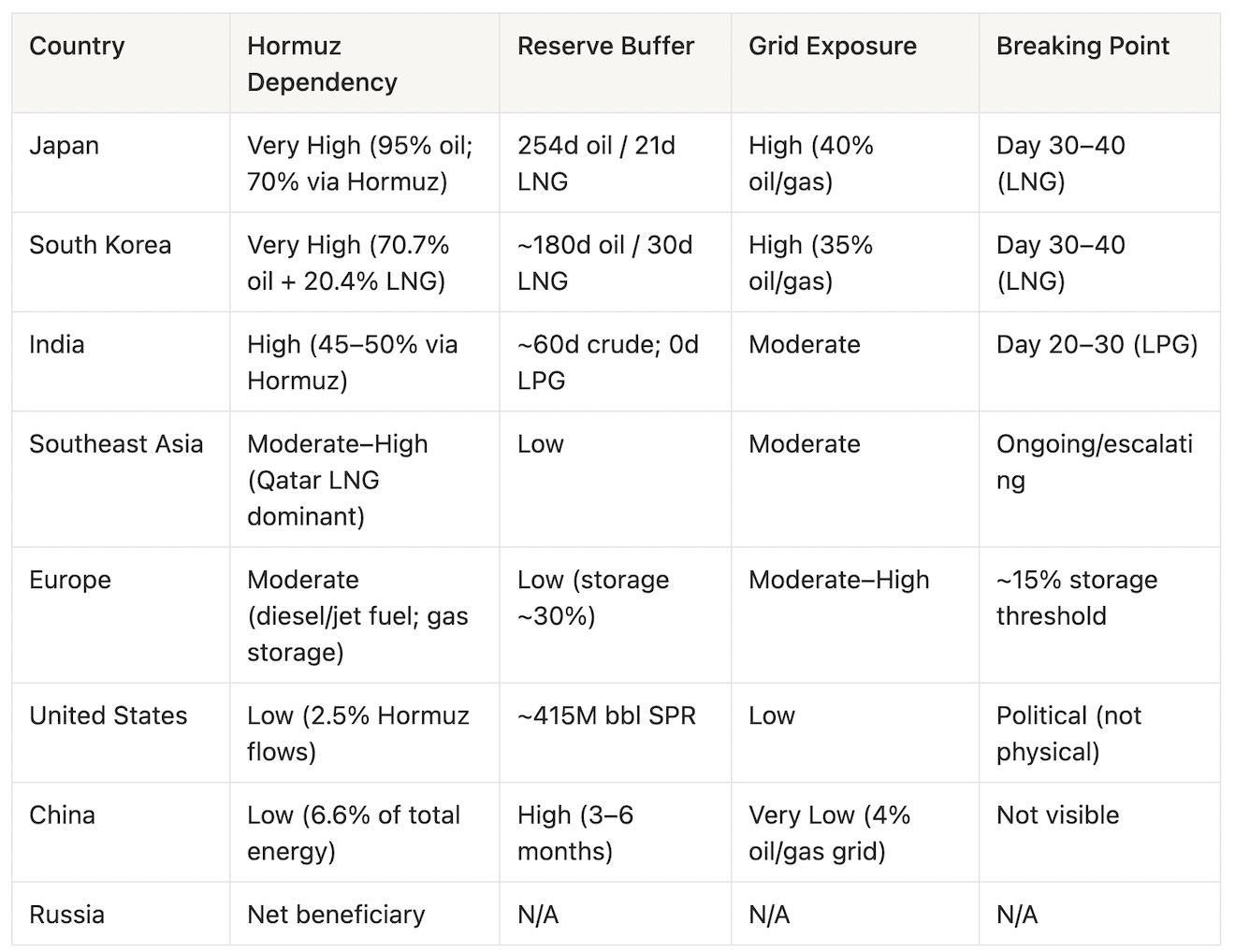

Japan

Japan is the most structurally exposed major economy on earth to a Hormuz closure. Approximately 95% of its oil comes from the Middle East, with roughly 70% of that transiting the Strait directly. Japan’s oil strategic petroleum reserve — nominally 254 days of supply — provides a significant buffer on crude. But Japan’s LNG position is the kill shot: the country holds only about three weeks of LNG inventory, and LNG fuels roughly 40% of Japan’s electricity grid.

The Fukushima irony is bitter here. After the 2011 disaster forced Japan to shutter its nuclear fleet, Qatar’s LNG supply became the lifeline that kept Japanese homes lit. That lifeline is now cut — Qatar’s LNG export facilities were among the targets of Iran’s Day 1 retaliatory strikes. Oxford Energy analysts have flagged that LNG spot prices could surge 170% if the disruption persists.

Japan is already acting unilaterally. It announced the release of 80 million barrels from national reserves on March 11 — 15 days of consumption. Forty-two Japanese-operated vessels remain trapped in or near the Strait. The Nikkei has sold off roughly 7% since the conflict began; the yen is weakening as a safe-haven currency in a world where the safe-haven playbook has been scrambled.

Physical shortage risk: Day 30–40 (LNG grid exhaustion threshold).

South Korea

South Korea’s exposure is nearly identical in structure to Japan’s, but the political circuit-breakers are already triggering. The country sources 70.7% of its oil and 20.4% of its LNG from the Middle East. Oil and gas together account for approximately 35% of grid power generation.

The KOSPI has fallen more than 12%, with trading halts triggered on the index’s worst days. In a measure not seen since 1997, South Korean President Lee Jae-myung has called for a fuel price cap — the first since the Asian financial crisis — with a ceiling of 1,900 won per liter reportedly under discussion, per the presidential policy chief. Refiners are cutting import volumes by 30%. Small independent gas stations have started closing.

The downstream consequence that Western investors consistently underestimate: Samsung and SK Hynix semiconductor fabs require stable, uninterrupted power. If the grid becomes unstable — not from blackouts, but from rolling voltage management — fab yields drop and production schedules slip. That is not a Korean problem. That is a global AI infrastructure problem, sitting inside your data center capex assumptions.

Hyundai Research estimates that $100 oil translates to a 0.3-percentage-point drag on Korean GDP, a 1.1-percentage-point acceleration in CPI, and approximately $26 billion in current account deterioration.

Physical shortage risk: Day 30–40 (synchronized with Japan on LNG exhaustion).

India

India consumes approximately 5.5 mb/d. Roughly 45–50% of that flows through Hormuz. The government secured a 30-day waiver from Washington allowing continued Russian oil purchases — a meaningful buffer for crude. But the LPG picture has no comparable workaround.

India imports roughly 62% of its LPG, with approximately 90% of that transiting Hormuz. India holds no strategic LPG reserve. LPG is not a premium fuel in India — it is the basic cooking fuel for hundreds of millions of households. Around 80% of Indian restaurants use LPG as their primary heat source. The Mangalore refinery has already been forced into temporary shutdown as feedstock flows dry up.

The social transmission is already visible. In Pune, crematoriums have switched from gas to wood and electric equipment as LPG supplies tighten. That is not an abstraction. That is a daily-life disruption reaching tens of millions of people.

Iran has, per Reuters citing Indian government sources, agreed to allow Indian-flagged tankers to transit the Strait — a bilateral arrangement that provides partial relief on crude while LPG supply chains remain disrupted. MUFG economists have flagged stagflationary dynamics: the rupee weakening, CPI accelerating, with every $20/barrel rise in oil prices translating to approximately a 4-percentage-point cut in corporate earnings.

Social-level shock risk: Day 20–30 (LPG chain stress reaching critical household penetration).

Southeast Asia

The region’s vulnerability is diffuse but accelerating. Pakistan — which sources approximately 99% of its LNG from Qatar — has seen gasoline prices rise 20% in a fortnight. The Philippines has shortened work weeks; Indonesia has imposed travel restrictions; Bangladesh cut Ramadan illumination. Economies with minimal fiscal room are already rationing.

Stress threshold: active and accelerating.

Europe

Europe’s Hormuz exposure is less direct — the continent sources roughly 30% of its diesel and 50% of its jet fuel from the Gulf — but the natural gas dimension is severe. European gas storage entered the conflict at approximately 30%, already historically low after the 2021–2024 drawdown cycle. The Netherlands, critically, held storage at just 10.7% at conflict onset. Gas prices have risen 75% since February 28. Gas-fired power generation is down 33% month-on-month.

Russia is the shadow beneficiary. Russian fossil fuel export revenues since the conflict began have risen by approximately €6 billion, including an estimated additional €672 million in premium pricing. The strategic paradox facing European governments: Trump may offer to ease Russian sanctions as a mechanism to flood European gas markets and reduce energy prices — which would simultaneously undermine the political architecture of European security that the continent has spent four years building. That is not a hypothetical. It is an active policy option circulating in Washington.

Crisis threshold: when gas storage hits ~15%, which, at current burn rates, is a question of weeks in the lowest-inventory markets.

United States

The US economy is the most insulated major economy in this analysis — and the most politically exposed.

The physical exposure is real but modest. Only approximately 2.5% of Hormuz throughput is bound for the United States. The SPR holds roughly 415 million barrels — historically low by post-1990 standards, but sufficient to backstop domestic markets for several months. Shale production capacity can respond — but with a 3-to-6-month lag from drilling decisions to incremental output. There is no short-term US production fix.

The California exception matters: 61% of refinery crude input in California is imported, with roughly 30% of that transiting Hormuz. Gasoline prices in California are already outliers versus the national average, and the state lacks the spare refinery capacity to substitute domestic crude at scale.

The actual US vulnerability is political, not physical. Pump prices are the most legible economic signal for American voters. Trump is simultaneously prosecuting a military campaign against Iran and publicly promising lower oil prices — a commitment that is physically impossible to fulfill while Hormuz remains closed and six-plus mb/d of Gulf Arab production remains offline. The contradiction cannot be sustained indefinitely. Something breaks: either the military campaign’s political support, or the administration’s credibility on economic management, or both.

Political transmission risk: active. Physical shortage risk: low in the near term, rising if the conflict extends past 90 days and SPR drawdown compresses the buffer.

China

China is the structural outlier — and the reason this article ends where it does.

Hormuz-transiting oil accounts for approximately 6.6% of China’s total primary energy consumption. Chinese strategic petroleum reserves are estimated at 1.2 to 1.4 billion barrels, equivalent to roughly 3 to 6 months of import coverage. New energy vehicles now account for more than 50% of new car sales in China; the grid’s oil and gas dependency is approximately 4%. The CSI 300 is down 0.1% since the conflict began. The yuan is outperforming every major Asian currency.

China has halted refined product exports — protecting domestic supply while others compete for alternatives. Iranian crude continues to flow to China through the Strait, per CNBC’s tracking of satellite vessel data (at least 11.7 million barrels since February 28, per TankTrackers). Iran’s compliance with its own blockade appears selective.

China is not a bystander. It is the fulcrum.

Russia

Russia is the only clear beneficiary. Approximately €6 billion in incremental fossil fuel export revenue in two weeks. European and Asian buyers that were diversifying away from Russian supply are now urgently seeking alternatives, and Russian pipelines and Arctic LNG routes are suddenly the most geopolitically uncomplicated options on the table. Washington’s India waiver on Russian oil purchases effectively reopened a sales window that the original sanctions regime had partially closed. The demand for Russian energy is, in the words of one market participant, “significantly increasing.”

V. The Vulnerability Matrix

VI. Demand Destruction: The Self-Extinguishing Mechanism

Oil has always carried its own cure. At high enough prices, demand collapses and the crisis resolves without diplomacy. The question is what price is high enough — and the answer, in this cycle, is higher than most people assume.

Bernstein analyst Irene Himona has done the most careful work on this: in today’s dollar terms, demand destruction at the scale needed to materially offset the Hormuz supply loss requires approximately $155/barrel as a full-year average for 2026 — the threshold at which the “oil burden” (oil spend as a share of global GDP) reaches the 5.2% level observed in 2007, historically associated with meaningful consumption reduction. Below that level, the world largely keeps buying and absorbs the pain through inflation, growth drag, and fiscal transfer.

Institutional forecasts for the resolution scenario (Hormuz gradually reopens) cluster as follows: EIA has Brent staying above $95 for two months before falling toward $80 in Q3; Goldman Sachs, per Daan Struyven’s latest note, revised Q4 2026 Brent and WTI targets to $71 and $67 respectively. Barclays flags $120 as testable if the conflict persists two more weeks, with a $150 tail scenario.

The critical insight is that demand destruction is not uniform.

Gasoline — roughly 25% of global demand — is elastic. Drivers cut discretionary miles. Diesel (17%) and jet fuel (8%) have harder floors: freight runs because supply chains require it, flights operate because business travel has no substitute. Petrochemicals (15–17%) are pure input-cost inflation. LPG and heating fuels are where the asymmetry is most severe. In the developing world, when LPG doubles, the response is not “drive less” — it is “switch fuels, reduce nutrition, cut activity.” Poor countries do not destroy demand gradually. They break.

VII. Duration Times Fragmentation: The Asynchrony Problem

The central analytical error in most current commentary is treating this as a single synchronized global shock. It is not. It is a shock that lands differently by country, product type, and reserve depth — and critically, the breaking points arrive at different times.

Japan and South Korea reach their physical shortage threshold on approximately Day 30–40 of sustained Strait closure, when LNG inventories are exhausted and spot procurement becomes either impossible or economically disqualifying. India’s LPG chain is already under acute stress; social-level disruption becomes difficult to contain by approximately Day 20–30. Europe’s crisis arrives when gas storage hits the 15% level — a function of current burn rates and the absence of Russian supply flexibility; in the most exposed markets, that is a matter of weeks. US political stress on energy escalates over Day 60–90 as SPR drawdown visibly compresses the reserve buffer and pump prices become a persistent electoral liability.

These different clocks produce a profound coordination problem. A ceasefire negotiation requires all parties to want resolution simultaneously. Japan and Korea may be screaming by Day 35; Washington may still be absorbing the crisis politically; India may have already seen street-level LPG riots. Europe faces its own calculus while watching Russian export revenues surge.

The asynchrony is Iran’s strategic asset. A unified Allied response requires equal pressure felt at equal times. That will not happen.

This is also why the SPR release — physically inadequate — was politically necessary. It buys not oil, but time: alignment time, the appearance of collective action that keeps Japan, Korea, and India from making bilateral arrangements with Tehran before Washington is ready to engage.

Whether that purchased time is used productively depends on two things: what happens in Paris this weekend, and whether the US military can beat the clock.

VIII. Three Theaters

The oil analysis above assumes one crisis. As of Day 14, there are three.

The Pacific Is Not Quiet

The MEU’s departure created a deterrence vacuum that was probed within hours. The details of the Day 14 events — Kharg Island, the Tripoli redeployment, the North Korean salvo, the fishing fleet formations — are catalogued in Section I. What matters here is the pattern beneath them.

The Chinese maritime militia formations are not improvised. AIS data tracked by geospatial firm ingeniSPACE shows three coordinated events since December 2025, each larger and further east: 2,000 vessels in December in two parallel inverted-L shapes, each 400 kilometers long; 1,400 in January in a 320-kilometer rectangle; 1,200 this week, closer to the Japan–China median line. Hundreds of vessels participated in multiple events, nearly all originating from Zhejiang province — home to several known militia ports. CSIS’s Gregory Poling: “They are almost certainly not fishing, and I can’t think of any explanation that isn’t state-directed.” The Pentagon’s own China military assessment confirms Beijing subsidizes these units to “perform official missions” and that they could support combat operations by creating obstacles to foreign military intervention.

North Korea’s salvo — its largest of 2026 — landed during the US-South Korea Freedom Shield exercises, which are running at reduced tempo as American assets shift to the Gulf. Pyongyang’s Foreign Ministry had already framed the war as proof that “the strong can survive and develop under any conditions; the weak will fall victim to sanctions and aggression.”

Neither event is unprecedented in isolation. The sequencing is. Japan is absorbing an LNG exhaustion clock, Chinese militia vessels to its southwest, and North Korean missiles to its west — while its security guarantor steams in the opposite direction. Taiwan is watching a rehearsal for its own blockade. The Iran war has cracked open a window in the Pacific, and the actors who have been preparing for it are testing it in real time.

The Hormuz Dilemma

The MEU redeployment was not arbitrary. Washington has a genuine operational need: two weeks of air strikes have destroyed over 15,000 targets and rendered Iran’s navy “combat ineffective,” per General Dan Caine, Chairman of the Joint Chiefs. But air power has not reopened Hormuz. The mines are in the water. Coastal anti-ship missile batteries have not been fully neutralized. The Strait remains closed. The MEU adds what air power cannot: the option to put boots on the ground.

Three operational scenarios are plausible for forcing Hormuz open. First, escort-first: the US degrades Iranian coastal defenses, clears mines, and begins escorting commercial tankers by late March. Energy Secretary Wright estimated this could begin by month’s end; the Wall Street Journal, citing officials, put it at a month or longer. Second, Kharg Island seizure: the MEU assaults the terminal handling 90% of Iran’s oil exports — Trump has already struck military targets there and threatened the oil infrastructure. Third, coastal clearing: operations along the 150-kilometer Iranian coastline commanding the Strait. The Australian Strategic Policy Institute compared this to “Gallipoli times ten.” The IRGC has 20,000 naval troops in the Strait region and has spent four decades rehearsing the repulsion of exactly this kind of assault.

The timeline is razor-thin. The Tripoli is 7 to 10 days from the Arabian Sea. If it arrives around Day 22–25, the military option becomes operational just as Japan and South Korea’s LNG reserves approach critical levels. A successful escort operation starting around Day 25 could begin relieving the most exposed allies before they hit physical shortage. A failed operation — a tanker struck under escort, an amphibious assault bogged down — would accelerate the crisis.

And even success has a ceiling. A Strait that is “open under armed escort” is not the same as a Strait that is open. Lloyd’s List estimates a basic escort operation would require 8 to 10 destroyers protecting 5 to 10 vessels at a time — a fraction of the pre-war traffic of nearly 100 transits per day. Forced reopening delivers a trickle, not a flood.

The Two-Front Bind

This is the strategic trap that no section of this article can analyze in isolation. The US needs the MEU in the Gulf to reopen Hormuz before its allies’ reserves run dry. But the MEU’s departure from the Pacific has created a deterrence vacuum that is being probed within hours. Every day the Tripoli steams west is a day the Pacific grows more permissive for actors who have been waiting for exactly this kind of American overextension.

The US military is not short of total capacity. It is short of capacity in two oceans at once. And the Iran war — which began as an air campaign that was supposed to end “very soon” — is now forcing a resource allocation decision between the Middle East and the Indo-Pacific that American defense strategy has spent two decades trying to avoid.

The oil crisis described in Sections I through VII is the trigger. What is emerging in Section VIII is the consequence: a global security architecture being tested at multiple stress points simultaneously, with the same finite set of assets being asked to hold every line.

IX. The Paris Prelude — Under Three Shadows

Tomorrow, US Treasury Secretary Scott Bessent sits down with Chinese Vice Premier He Lifeng in Paris. According to the Associated Press and Reuters, the meeting runs Sunday and Monday — a preparatory session for President Trump’s scheduled state visit to Beijing beginning March 31, his first to China since 2017. On the American side, the public agenda is trade: reducing Chinese purchases of Russian and Iranian oil, increasing Chinese imports of US soybeans, Boeing aircraft, and energy.

The agenda was overtaken by events before the plane landed.

Bessent is not walking into a trade negotiation. He is walking into a room where the man across the table holds leverage over all three theaters described above — the Gulf, the East China Sea, the Korean Peninsula — and knows it. Beijing did not create any of these crises. But Beijing is the only actor positioned to resolve or exploit all three simultaneously. That is the hand He Lifeng brings to Paris.

Hours before the meeting was announced, CNN reported that Iran is considering allowing a limited number of oil tankers to pass through the Strait of Hormuz — on one condition: oil cargo must be settled in Chinese yuan, not US dollars. A senior Iranian official confirmed the framework to CNN. RBC-Ukraine, citing the same reporting, framed it precisely: tankers can pass, but only if trade is denominated outside the dollar system.

Iran is not simply offering a passage fee. It is offering China the prototype of a new monetary architecture: yuan-denominated energy settlement enforced at the world’s most critical chokepoint. If China accepts — and if tankers begin flowing on yuan terms — Beijing will have embedded its currency in the infrastructure of global energy trade in a way that no financial engineering or diplomatic agreement could have achieved in peacetime.

The ask Bessent carries into the room — “pressure Iran, buy less Russian oil, buy more American stuff” — was already a difficult pitch. It is now almost absurd. The US is asking China to forgo a once-in-a-generation monetary upgrade, restrain its maritime militia at the moment of maximum American overextension, and help stabilize a Korean Peninsula it has no interest in stabilizing — in exchange for soybean purchases and goodwill toward a state visit.

Bessent is not arriving empty-handed. He is arriving with that MEU steaming toward the Gulf. The implicit message: if China does not broker a resolution, the US will attempt to force one, and the resulting escalation would be far messier for everyone — including for China’s own energy flows and for the yuan-settlement architecture that Iran is offering. A negotiated reopening preserves Beijing’s leverage. A military reopening destroys the conditions under which that leverage operates.

But the MEU is also Bessent’s weakness. Beijing knows that every day the Tripoli steams west is a day the Pacific grows more permissive. The military card that gives Washington leverage on Hormuz simultaneously gives Beijing leverage on everything else. China does not need to escalate in the Pacific. It just needs to keep rehearsing, keep probing, keep demonstrating that the US cannot hold two oceans at once — and let the implications do the negotiating.

China’s leverage at the table is not static. It compounds daily. Every day Japan and Korea inch toward their LNG exhaustion threshold, Washington’s ask becomes more urgent and its concession space expands. Every day the Pacific deterrence gap widens, the price of Chinese restraint rises. The asynchrony of breaking points described in Section VII does not operate symmetrically — it operates in Beijing’s favor across every theater.

“The only broker in the room is Beijing. The price will be high.”

What can Washington offer that might compete? Sanctions relief on Chinese tech exports, a CHIPS Act rollback, movement on Taiwan — these are not trade-desk concessions. They are strategic architecture decisions that require principals-level authorization, not Bessent in Paris. Which is precisely the point: this meeting is Washington taking the measure of China’s price before Trump arrives in Beijing on March 31.

Carnegie Endowment analysts have long argued that Beijing’s energy diplomacy operates on a horizon Washington’s electoral cycle cannot match. Iran’s yuan offer is not a surprise to Beijing. It has been discussed in bilateral channels for years. The Hormuz crisis moved it from theoretical to operational. The Pacific vacuum moved it from operational to urgent.

Four scenarios are now live. In the first, China brokers a face-saving Hormuz reopening, restrains the militia activity, and yuan settlement remains marginal — the EIA’s $70-range year-end Brent baseline assumes this. In the second, China extracts full structural concessions on Taiwan, tech, and currency architecture; Hormuz reopens on Chinese terms; the Pacific probing continues because Washington has conceded the leverage that would have stopped it. In the third, diplomacy stalls and the US forces the Strait open militarily around Day 25–30 — but the Pacific remains exposed, and the “victory” in the Gulf is purchased at the cost of deterrence in the theater that actually matters for the next 30 years. In the fourth, both tracks fail — diplomacy produces nothing, the military operation is delayed or bloodied — and Japan, Korea, and India enter physical rationing while the Pacific tests move from rehearsal to execution.

The Paris meeting will not resolve any of these crises. But it may be the last moment at which they are still separate crises — before they merge into a single, cascading confrontation that no one in the room has the authority to stop.

What Is Actually Breaking

This article began as an energy analysis. It is now a war assessment.

Two-thirds of the global oil shortfall has no solution in operation or in transit. And on Day 14, the crisis stopped being about energy: the US pulled its only forward-deployed Marine force out of the Pacific, and within hours both Beijing and Pyongyang moved to test the vacancy — not in response to the redeployment, but alongside it, as if the script had already been written and the cue had just arrived.

The question this article set out to answer — who breaks first under $100 oil — now sits inside a larger and more dangerous one: how many fronts can open before the system that is supposed to hold them closed admits it cannot hold them all?

This is not an abstract structural question. It is a concrete operational one with a near-term timeline.

The MEU arrives in the Gulf around Day 22–25. If the Strait is forced open by Day 30, Japan and Korea survive their LNG clocks — barely. But the Pacific remains exposed for every day of that operation and for weeks afterward. If the Strait is not forced open, allies begin rationing and the diplomatic leverage shifts decisively to Beijing. If the Pacific probing escalates while the MEU is in the Gulf — a fishing fleet incident near the Senkakus, a North Korean test that overshoots, a Chinese naval exercise that crosses a line — the US faces a choice it has spent 80 years of alliance architecture trying to avoid: which theater to abandon.

Tomorrow in Paris, Bessent and He Lifeng sit across from each other with all of this on the table. The American offer is trade concessions and the implicit threat of military escalation. The Chinese counter is restraint — in the Gulf, in the East China Sea, on the Korean Peninsula — priced at whatever Beijing decides restraint is worth this week. Next week it will cost more.

The next 48 hours are not a negotiation window. They are the last interval before the crises in the Gulf, the East China Sea, and the Korean Peninsula stop being parallel and start being the same war.

“Who breaks first” is no longer about oil. It is about whether anyone in the room has the authority — and the nerve — to stop what is coming.

Invalidation Signals

The bearish thesis (oil prices sustained above $100, structural fragility deepening) requires monitoring against these exit conditions:

Rapid Hormuz reopening: A ceasefire or Iranian decision to reopen the Strait within the next 10–14 days would collapse the geopolitical premium and validate the EIA/Goldman Q3–Q4 $70–$80 range. Watch for: official Iranian announcement accompanied by independent maritime confirmation of vessel movement.

Saudi pipeline fully operationalized: If Yanbu loading consistently exceeds 3.5 mb/d for more than a week, the theoretical 7 mb/d capacity is being approached in practice. This would be a material supply-side relief signal.

IEA release rate beats estimates: If daily SPR flows from IEA members track at 4+ mb/d sustained, the effective gap-fill rises above 20% — still insufficient, but meaningfully better than base case.

Demand destruction arrives early: If global air travel data (IATA weekly) and US diesel consumption (EIA weekly) show simultaneous sharp declines, the $120–$155 demand-destruction mechanism may be triggering ahead of schedule. This resolves oil prices but creates a new problem: recession pricing in growth assets.

US escort operations begin successfully: If the Navy begins escorting tankers through Hormuz before Day 30 without a major incident (no escorted vessel struck, no mine detonation in convoy), the military path becomes the primary resolution mechanism. Watch for: CENTCOM announcement of escort corridor, confirmed commercial vessel transits under protection, and insurance markets beginning to write new policies for escorted passage. Even partial success — 10 to 15 escorted transits per day — would meaningfully change the supply math.

China successfully embeds yuan settlement into Strait passage mechanism: This is not a short-term oil price signal. It is a long-duration structural shift in the petrodollar architecture. Watch for: Iranian government announcement of yuan settlement requirements for passage, followed by observable vessel traffic resuming with Chinese financial intermediaries. If this materializes, it is the most consequential development in the global monetary order since the 1973 oil embargo — and it will not initially look like a crisis. It will look like a solution.

Pacific escalation crosses from rehearsal to incident: The thesis that Beijing and Pyongyang are probing, not attacking, requires that the probing remain below the threshold of a kinetic or territorial event. Watch for: any physical confrontation between Chinese maritime militia and Japanese Coast Guard near the Senkakus; a North Korean missile that lands inside Japan’s exclusive economic zone closer to shore than previous tests; a Chinese naval exercise that transits the Taiwan Strait or enters Japanese territorial waters while the 31st MEU is in the Gulf. Any of these would transform the multi-theater pressure from a leverage play into a genuine second-front crisis, radically compressing the timeline for every other variable in this analysis.

This is the second installment in Garrett’s Signal’s Hormuz series. The first piece — Home Is the Battlefield — mapped the domestic shock: how the Strait closure translates into household-level pain across economies dependent on Gulf energy. This piece follows the fractures outward — from homes to hemispheres — tracking where the crisis has spilled beyond energy markets into the global security architecture, alliance commitments, and the multi-theater confrontation now taking shape across the Gulf, the East China Sea, and the Korean Peninsula.

Garrett’s Signal · March 2026 · Day 14 of the conflict

No biases, solid analysis. Eager to see your reporting as things unfold! Kudos!

Great analysis. Arrived independently at the same conclusions a few days ago but with a lot less data. Glad to see your data backing up this conclusion. The net result of this conflict is an irreversible, dramatic weakening of US influence and a substantial strengthening of its rivals. That is asymmetric warfare.