The Most Important Job Interview in Washington

One man, three audiences, three contradictory scripts.

For three weeks, Iran was the only trade. Every headline, every tick, every desk conversation. Now the ceasefire is holding, a second round of negotiations is pending, and the war’s marginal grip on prices is loosening. The S&P made new highs within three weeks of the war low. Oil dropped nearly $20 from its spike. VIX slipped back below 20. The market hasn’t moved on from Iran. It’s just in a holding pattern, waiting for the next round of talks to tell it what to do.

But while Iran waits, another catalyst isn’t waiting.

At 10:00 AM Eastern, Kevin Warsh sits down in front of the Senate Banking Committee for the most important job interview of his life. If it goes well, this 55-year-old former Fed governor, Stanford fellow, and Wall Street veteran becomes the seventeenth Chair of the Federal Reserve when Powell’s term expires on May 15.

But “goes well” is a luxury assumption in 2026 Washington.

An Impossible Brief

Warsh faces three audiences today. They want three different things.

Trump wants to hear: rate cuts. Now. The president told Politico back in December that willingness to cut immediately was his “litmus test” for the job.

The Senate wants to hear: independence. Republican Senator Tillis has publicly declared he won’t vote on any Fed nominee until the DOJ investigation into Powell is resolved. Warren went further, calling Warsh a “Trump sock puppet.”

The market wants to hear: clarity. The oil shock has evaporated this year’s rate cut expectations from two to 0.6. Two-year Treasury yields are up 30bp since the war started. Traders don’t care about nice words. They care whether Warsh is a dove or a hawk.

One man. Three scripts that contradict each other completely. That’s the show today.

Who Is Kevin Warsh?

Fed governor from 2006 to 2011. Lived through the entire financial crisis.

Publicly opposed QE2 in 2010. Resigned in 2011. This is his defining career move.

Joined Druckenmiller’s family office afterward. Research fellow at Stanford’s Hoover Institution.

Core label: “limited central banker.” The Fed should do monetary policy and nothing else.

Father-in-law: Ronald Lauder, Estée Lauder heir, World Jewish Congress president, longtime Trump confidant.

One line to capture his policy philosophy: the Fed does too much, prints too much, talks too much.

His Two Rate Cut Playbooks

Warsh’s core dilemma: Trump wants cuts. Inflation won’t allow them. He’s prepared two narratives to sell the story.

Playbook One: AI Will Kill Inflation For Us

The logic chain is elegant. AI boosts productivity. Costs fall. Inflation retreats naturally. Room to cut opens up.

Warsh explicitly draws the parallel to Greenspan in 1996, when Greenspan resisted rate hike pressure and bet that internet-driven productivity gains would contain inflation. He won that bet.

The problem: 1996 is not 2026.

In 1996, inflation had just dropped to 2%. The fiscal trajectory was heading toward surplus. Globalization was crushing import prices. Today? Inflation has run above target for six straight years. The deficit is at wartime levels. Tariffs and decoupling are pushing costs up. A Middle Eastern war just sent oil into triple digits.

Worse: Greenspan spent a decade building credibility before he made that bet. Former Fed Chair Yellen said it publicly last week: “I don’t think Warsh walks in with that level of credibility.”

Even Warsh’s own allies are hedging. Lavorgna, former senior Treasury advisor and a Warsh supporter, is pulling back: “Kevin is right that AI can be deflationary. But the Iran war changed the equation.”

Playbook Two: Shrink the Balance Sheet, Then Cut

This one is more technical. Also more likely to gain traction inside the FOMC.

The formula: aggressively shrink the Fed’s balance sheet by roughly $1 trillion, which is equivalent to about 50bp of tightening. Then cut rates 50bp to offset. Net effect: easier policy, smaller balance sheet.

Sounds clever. Left hand tightens, right hand loosens.

The constraints are hard.

The Fed holds $1.9 trillion in MBS. Most are low-rate mortgages. Homeowners won’t prepay. Natural runoff takes decades. Actively selling? BofA’s Cabana: “Extremely disruptive to financial markets.” The last time the Fed tried shrinking aggressively, it ended with the 2019 repo market blowup. Cleveland Fed President Hammack has flagged that bank liquidity rules leave limited room to shrink further.

Bottom line: the actual space for balance-sheet-for-rate-cuts is far smaller than what Warsh may have promised Trump behind closed doors.

What the Written Testimony Already Tells Us

Warsh’s prepared remarks were released last night. Key signals:

1. “The Fed must stay in its lane.” This is today’s headline quote. On the surface, it defends independence. In practice, it draws a line: the Fed should stick to monetary policy and stop wading into climate, social equity, and financial regulation. It reassures senators worried about independence while laying groundwork for shrinking the Fed’s scope.

2. No mention of rate views. Zero commentary on whether current rates are appropriate. Standard confirmation hearing playbook: stay vague, give no ammunition.

3. “The Fed must take responsibility for persistent inflation.” This is subtle. It criticizes the Powell-era legacy of loose policy (pleasing Trump) while signaling he’ll take inflation seriously (reassuring markets).

Our read: Bloomberg Economics’ Wilcox mapped Warsh’s possible positioning into three buckets. Traditionalist (maintain the status quo entirely), reformer (narrow the Fed’s scope, overhaul the communication framework), revolutionary (invoke Section 11, redefine the Chair’s power). The written testimony puts Warsh squarely in the reformer camp. No rate cut timeline. No loyalty pledge to Trump. But nothing that would make Trump unhappy either. A confirmation hearing is not a policy meeting. He just needs to not screw up.

Five Questions That Actually Matter

If you can only watch five exchanges today, watch these.

① “If the president asks you to cut rates, what do you do?”

The ultimate independence test. Warsh will almost certainly say monetary policy must be independent of political pressure. Watch the intensity. “Absolutely” and “generally” are very different words.

② “Would you use Section 11 to remove regional Fed presidents?”

This might be the most explosive question of the night. Section 11 of the Federal Reserve Act gives the Board the power to remove regional Fed presidents “for cause.” In 112 years, it has never been used. But it matters now because the Trump administration has already demonstrated similar moves at other independent agencies. If the president pressures a new Chair to fire dissenting regional presidents, what does Warsh do? This is not hypothetical. Regional presidents hold 5 rotating FOMC votes plus New York’s permanent seat. That’s nearly half the committee. If the Chair can fire dissenters, FOMC independence becomes a fiction. This is the ultimate test of whether Warsh is a reformer or a revolutionary.

③ “What’s your view on the dot plot and the SEP?”

Warsh has long argued that Fed officials talk too much. He may push to eliminate the Summary of Economic Projections and the dot plot, which would be the biggest overhaul of FOMC communications since Bernanke. If he signals this clearly, expect a market reaction: no dot plot means traders lose forward guidance, which means rate volatility goes up.

④ “How does the oil shock affect monetary policy?”

The trickiest question on the board. Say “oil is transitory” and risk getting the Powell 2021 treatment. Say “oil will keep pushing inflation higher” and you’ve just announced no cuts are coming. Trump won’t like that. Watch how he walks the tightrope.

⑤ Does Tillis blink?

Republican Senator Tillis holds the key to the confirmation timeline. If he softens his stance before or during the hearing, Warsh’s confirmation becomes high-probability. If he holds firm, we could see a Chair vacancy after Powell’s May 15 expiration.

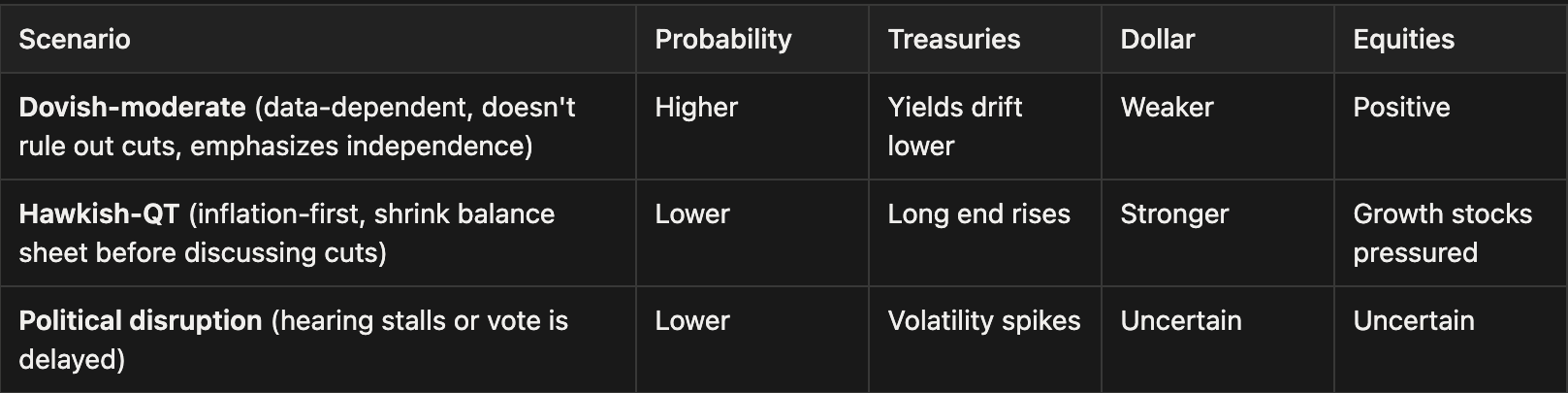

Three Scenarios, Three Market Reactions

Scenario one is the most likely outcome. The reasoning is simple: the point of a confirmation hearing is to get confirmed, not to pledge allegiance. Nearly every nominee in history has played it vague. Warsh has already pivoted toward moderation in his written testimony.

If scenario one plays out, it matters more than people think.

Here’s why. The market’s pricing of the Fed right now is deeply pessimistic. Futures imply only 0.6 cuts this year. Two-year yields are up 30bp since the war started. Rate volatility (the MOVE Index) is stuck at elevated levels. The bar for a dovish surprise is low. Warsh doesn’t need to say “I will cut rates.” He just needs to not close the door. One sentence like “if the data allows, we have room to adjust policy” would be enough to give the front end some relief.

The timing matters even more. The S&P just made new highs from the war low in three weeks, but the bond market hasn’t followed at all. The equity-bond divergence is at an extreme. If Warsh’s dovish tone confirms the narrative that the Fed won’t pour gasoline on a wartime fire, this divergence could start closing: bonds rally, dollar softens, risk assets get another leg.

Flip it around. If Warsh surprises hawkish, the current equity-bond gap tells a different story: bonds were right, stocks were wrong. The drawdown will hurt.

One Last Thing: Hearing Dove ≠ Policy Dove

The biggest trap today is mapping Warsh’s hearing tone directly onto future policy.

Reality check: the Fed Chair is not a dictator. The FOMC has 12 votes. Warsh’s two rate cut narratives, AI productivity and balance-sheet-for-cuts, have almost no buy-in inside the committee. The first requires Greenspan-level credibility that takes years to build. The second is constrained by MBS liquidity and bank reserve requirements.

More important: this hearing coincides with the Iran ceasefire expiration. If today delivers Warsh-dovish plus ceasefire-extended at the same time, expect a risk-on wave. If it’s Warsh-hawkish plus ceasefire-collapses, volatility gets repriced.

Two catalysts stacking. That’s the real trade today.

Garrett’s Signal · Independent macro and cross-asset research