Trump Blinked Again. This Time It May Kill the Petrodollar.

Trump's latest retreat did not end the war — it accelerated the collapse of dollar hegemony.

Note: This is not a formal sequel to the Hormuz Series, but an event-driven special edition. Today Trump extended his 48-hour ultimatum to strike Iran's power plants by five days, claiming on Truth Social that the U.S. and Iran have had "very good and productive conversations" — while Iran flatly denied any talks have taken place. We believe the far-reaching implications of this retreat are severely underpriced by the market, and its logic demands immediate dissection. This piece builds on our first three installments — from the Hormuz battlefield analysis (Part I), to the energy vulnerability rankings (Part II), to the dollar debt system (Part III) — and focuses on this event's impact on the petrodollar system.

Trump blinked. Again.

Right on cue, a chorus of analysts declared the worst is over. “Peak escalation has passed.” “De-escalation is underway.” Markets rallied. Volatility compressed. Everyone exhaled.

This is dangerously naive.

This reading is a purely America-centric narrative — treating Iran’s more than 93 million people as extras in a movie scripted by Washington. It ignores the most fundamental principle of geopolitical analysis: empathy.

Let me reframe.

Imagine a country bombed for weeks. Schools destroyed. Civilians killed. Then one day, the aggressor quietly extends its own ultimatum — not because a peace treaty was signed, but because it’s running low on ammunition. Worse, it claims to be in “productive talks” with you — talks you know never happened. Would the victim accept? Would you trust the aggressor not to come back once it restocks?

Add this: the aggressor has signed peace agreements before — and torn them up. Every single time.

This is Iran’s position today.

An airstrike hit a girls’ school in Iran. Dozens of students killed. Classrooms turned to rubble. Ask yourself — if your child was buried under that rubble, would you accept the aggressor simply extending its own deadline, dressed up as “diplomatic progress,” with no long-term peace commitment? Or would you pick up a weapon?

If you do geopolitical and macro analysis without empathy — without truly putting yourself in every participant’s shoes — you’re not analyzing. You’re projecting your portfolio onto the world. Like those fund managers sitting in trading rooms far from the battlefield, caring only about their positions, demanding governments adopt policies favorable to their holdings. Completely indifferent to the lives of the people on the ground.

Now they want Iran to surrender. How convenient.

The only thing that can bring the U.S. to the table to sign a binding, long-term peace agreement is a protracted war — making the U.S. bear unbearable costs until the price of continued conflict exceeds the price of negotiation. Every asymmetric war in history follows the same logic: the weaker side wears down the stronger side’s will and resources by extending the duration of the conflict. As we argued in Part I: airstrikes cannot reopen the Strait of Hormuz, the diplomatic window is narrowing, and Iran’s cheap asymmetric arsenal — drones, mines, shore-based anti-ship missiles — has trapped the U.S. in a “can’t leave, can’t win” dilemma. This dilemma was not resolved by this retreat — only temporarily shelved.

I. Three Paths — Trump Chose the Worst One

Trump had three paths:

Path One — Quick Victory: Impossible. Iran has vast territory, a population exceeding 93 million, and produces far more missiles than the U.S.

Path Two — Protracted War: Sustained high inflation, U.S. debt expansion, potential Treasury default, dollar asset collapse.

Path Three — Retreat: Suppresses short-term volatility, but destroys the petrodollar system.

Trump chose Path Three — trading a few days of market calm for the structural dismantling of America’s most powerful weapon.

As we analyzed in detail in Part I, the logic of this trap: the U.S. cannot exit (or the entire Middle Eastern alliance system collapses), nor can it win by airstrikes alone (the real blockading force at Hormuz is Iran’s asymmetric arsenal and the rational retreat of the global insurance system). Path Three appears the easiest of the three — but it is not a solution. It transfers strategic costs from the military ledger to the monetary one.

II. Why Did Trump Blink? Three Motives.

Motive One: Market Manipulation

An unprovable but logically worth examining speculation: before announcing the deadline extension, Trump may have established long oil and short equity positions, then reversed — flipping his book.

If true, this is the most grotesque scenario imaginable. Iranian civilians, Israeli soldiers, more than 50,000 American troops deployed to the region — all reduced to props in one man’s P&L optimization. A modern-day “Boy Who Cried Wolf” played with real missiles and real lives, for one man’s equity curve.

Motive Two: Volatility Suppression

Markets were screaming. VIX spiked. Credit spreads widened. Treasury yields approached dangerous territory. A temporary ceasefire signal compressed volatility — buying the government time to manage the narrative.

Motive Three: Military Stalling

A tactical pause. The U.S. has redeployed Patriot and THAAD missile systems from South Korea and signed expanded missile production contracts with Japan. The five-day extension buys time to restock — while the public thinks diplomacy is working.

None of these motives produce lasting effects. They are short-term tricks that accelerate long-term structural damage.

III. The Long-Term Consequences Are Catastrophic

1. American Credibility Is Officially Bankrupt

Traders are betting on another TACO trade — “Trump Always Chickens Out,” the term Wall Street coined during his 28 tariff flip-flops and now applies to his geopolitical retreats. Each one makes the next negotiation harder.

Iran will never again trust American commitments — why should it? The U.S. was about to complete nuclear negotiations, then bombed Iran. The Minsk agreements were torn up. Every “deal” is a prelude to the next betrayal. And now Trump claims on Truth Social that the two sides have had “very good and productive conversations” — while Iran’s officials flatly deny any talks have taken place. This is not diplomacy. It is gaslighting on a geopolitical scale.

Result: Iran doubles down on protracted war strategy. No ceasefire without a binding long-term peace framework — and the U.S. has proven it cannot honor one. As we noted in Part II, Iran’s strategic advantage lies precisely in the asynchrony of each country’s “breaking point” — Japan and South Korea face LNG depletion by Day 30–40, India faces an LPG crisis by Day 20–30, while America’s pain point is political rather than physical. This asynchrony is Iran’s strategic asset: it makes a unified allied response impossible, and ensures that any U.S. retreat at a single point in time cannot satisfy all stakeholders simultaneously.

2. Gulf States Become Collateral Damage — And They Know It

This is the truly terrifying consequence.

If the U.S. unilaterally backs off its own ultimatums and walks away, who is left to clean up the mess? The Gulf states. Saudi Arabia, the UAE, Qatar, Kuwait — the countries whose infrastructure was destroyed, LNG facilities demolished, economies devastated — while the U.S. fabricates “productive talks” on Truth Social.

The Gulf states are not stupid. They will draw the only rational conclusion: America’s security guarantee is worthless.

And once the Gulf states conclude that “America’s security guarantee cannot be relied upon,” the foundation of the petrodollar — the 1974 Kissinger-Saudi arrangement, “we price oil in dollars, you protect us” — collapses.

IV. The Petrodollar Death Spiral

Let me trace the transmission chain from Trump’s retreat to systemic dollar collapse.

U.S. unilateral withdrawal → Gulf states lose trust in U.S. security → Petrodollar compact breaks → Gulf sovereign wealth funds exit U.S. assets → Dollar credibility collapses → Treasury crisis → Hyperinflationary feedback loop

Here is how each link operates:

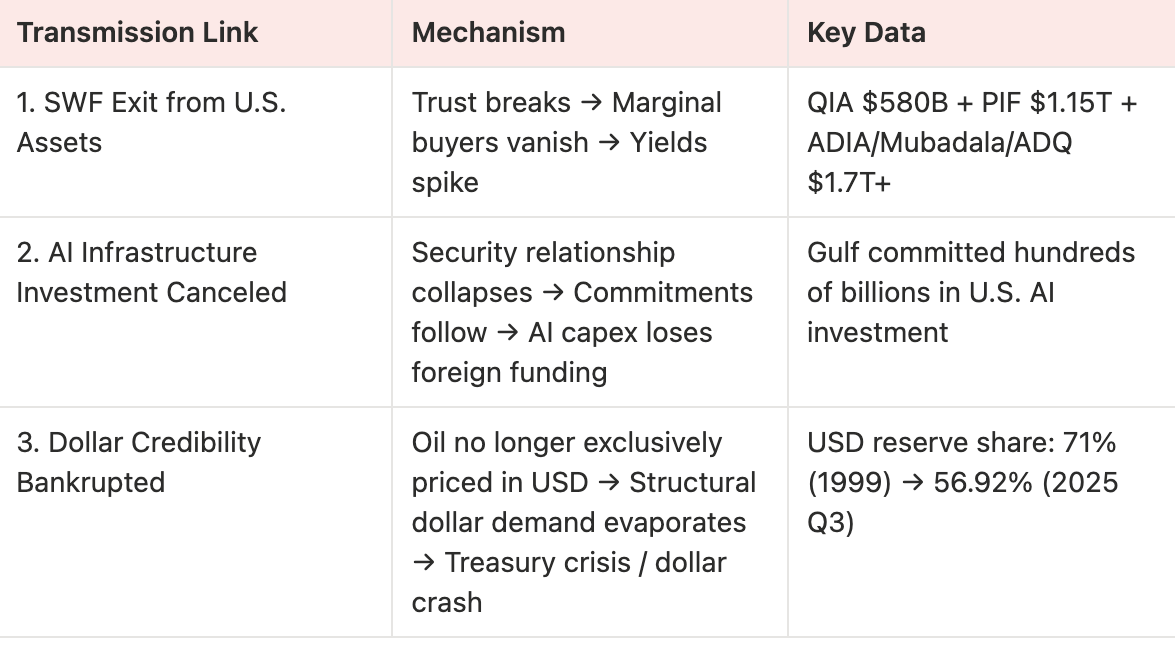

Link One: Gulf Sovereign Wealth Funds Exit U.S. Treasuries and Equities

Gulf sovereign wealth funds hold trillions in U.S. assets — Treasuries, equities, real estate, AI infrastructure. Qatar’s QIA alone holds $580 billion, Saudi Arabia’s PIF manages over $1.15 trillion, and Abu Dhabi’s ADIA, Mubadala, and ADQ collectively manage approximately $1.7 trillion.

If these funds begin exiting Treasuries and U.S. equities — not because of sanctions, but because of broken trust — the effect is a mass retreat of marginal buyers from the U.S. debt market. Yields spike. The debt death spiral we dissected in detail in Part III — $39 trillion in national debt (as of publication), 125%+ Debt/GDP, interest payments already exceeding defense spending, and the three conditions Ray Dalio described converging simultaneously — would accelerate. Part III analyzed the “first transmission channel”: Hormuz → oil prices → inflation → interest rates → fiscal → dollar. Today’s link adds a more direct path: trust breaks → capital flight → yields spike — both channels firing at once.

Link Two: Gulf States Cancel AI Infrastructure Investment

Saudi Arabia, the UAE, and Qatar have collectively committed to invest hundreds of billions of dollars in U.S. AI infrastructure. These commitments were premised on a functioning security relationship. If that relationship collapses, the commitments collapse with it.

The effect: the AI capex boom — the single largest driver of U.S. equity momentum — loses its most important foreign funding source. The AI debt crisis we have been warning about just got moved up by years.

Link Three: Dollar Credibility Bankrupted

If the petrodollar system collapses — if oil is no longer exclusively priced in dollars — global structural demand for the dollar evaporates. Central banks no longer need to hold large dollar reserves. The dollar’s “exorbitant privilege” dies.

Result: Directly triggers a Treasury crisis, or a dollar collapse, or both — leading to U.S. hyperinflation and a self-reinforcing debt-inflation death spiral. The data we cited in Part III — BRICS nations quietly exiting the Treasury market (China’s holdings down from a peak of $1.3 trillion to under $700 billion, Brazil reducing holdings by 27% in a single year, India cutting 20% over the same period), global central bank gold purchases doubling, the dollar’s reserve share falling from 71% in 1999 to 56.92% — all of these slow-moving variables would be violently amplified the moment the petrodollar system fractures.

V. A Brief History of the Petrodollar — What Is Truly at Stake

In Part III we systematically dissected the full history and mechanics of the petrodollar system from the perspective of dollar weaponization. Here we offer only the briefest recap, focusing on the core structure directly under assault from today’s event: security in exchange for pricing power.

In 1974, Kissinger struck a world-altering arrangement with the Saudi royal family: Saudi Arabia would price its oil exports in dollars, with oil revenues recycled into U.S. Treasuries; in exchange, the U.S. would provide military protection and security guarantees. By 1975, all OPEC members followed suit. This created the petrodollar recycling mechanism — the anchor of global rigid demand for the dollar.

For 52 years, this system has been the invisible architecture of American hegemony. More powerful than aircraft carriers. The underlying reason the U.S. can run $2 trillion annual deficits without consequence.

And Trump just took a sledgehammer to its foundation — not through the war itself, but through the signal sent by his latest retreat: America’s security guarantee cannot be trusted. When this signal is layered on top of the slow-moving variables analyzed in Part III ($39 trillion in debt, BRICS de-dollarization, central bank gold hoarding), the petrodollar system faces not gradual erosion but the possibility of structural fracture.

VI. Institutional Q&A — What the Smart Money Is Asking

Over the past week we have been in close contact with institutional investors. Here are the 11 most frequently asked questions — and our answers.

Q1: Can the U.S. Unilaterally Walk Away?

No.

Iran will not allow it. Iran seeks a long-term solution — it has publicly stated its conditions, consistent with our analysis. Without a binding peace framework, Iran keeps fighting. A U.S. unilateral withdrawal will not end the war; it guarantees its continuation.

Q2: What Is the Probability of a Ground Invasion? What Would the Objective Be?

Low probability, but cannot be ruled out — as we argued in detail in Part I of this series, if diplomacy fails and airstrikes cannot reopen the Strait of Hormuz, ground forces are the only remaining military option. But it is strategic madness. Iran is far harder to fight than Afghanistan — larger territory (2.5×), over 93 million people (approximately 2.1×), with a real military-industrial complex. Afghanistan took 20 years and approximately $2.26 trillion (per Brown University’s Costs of War Project). With U.S. debt at $39 trillion and interest costs already exceeding defense spending, this is the worst option. Trump’s current choice of the retreat path (Path Three) lowers the short-term probability of a ground invasion, but as long as the Strait of Hormuz remains closed, this option stays on the table.

If it happens, it would be structurally bullish for Chinese assets over the long cycle — the U.S. bleeds while RMB-denominated assets benefit from relative strength.

Q3: What Does an 80% Probability Protracted War Look Like?

Missiles + drones. Key data point: Secretary of State Rubio himself stated that Iran produces over 100 missiles per month. The U.S. produces 6–7. If accurate, the math of a war of attrition is devastating for the U.S. We laid out the full picture of this cost asymmetry in Part I: a single Shahed drone costs $10,000–50,000; a single Patriot interceptor costs $2–4 million. Iran can launch dozens of threats for less than the cost of a single intercept. Even if 90% are intercepted, the remaining 10% is enough to make the entire shipping lane uninsurable. And Iran is almost certainly receiving external support — it is not fighting alone.

Q4: Can the U.S. Destroy the Strait or Seize Islands to Control Hormuz?

Largely irrelevant. Drones and missiles are too cheap and too numerous. America’s core problem is air defense missile inventory — using expensive interceptors against cheap drones is a losing proposition. Unless U.S. intelligence can locate and destroy every drone production line and launch site in Iran — across a country the size of Alaska — the Strait remains contested.

Q5: Can Russian Oil Fill the Middle Eastern Gap?

Minimal help. Russia’s energy export focus has fully pivoted to Asia (primarily China). While some volumes still reach Europe through indirect channels (Russia has pocketed over €7 billion in fossil fuel exports in the first two weeks of March alone, with daily oil revenues up 14% from pre-war levels), this is far from enough to fill the Middle Eastern gap. The more critical question is whether Russia would sell to South Korea, Taiwan, and Japan — given current geopolitical relations, the answer for Taiwan and Japan is very likely no.

Taiwan’s energy vulnerability is the single largest black swan for the global AI supply chain. As we detailed in Part III — Taiwan has only 11 days of LNG reserves, yet produces over 90% of the world’s advanced chips.

Q6: What Would Trigger a U.S. Treasury Default? What Is the Path?

The trigger conditions are already emerging. We are watching for the point at which yields break expectations — in either magnitude or duration. A simple reference: during the Russia-Ukraine war, U.S. inflation peaked at 9%. If Treasury yields reach 9%, the system detonates.

5% on the 10-year is the critical threshold. Beyond that level, the effects are nonlinearly compounding. We analyzed this more fully in Part III — when the interest-to-revenue ratio keeps rising, Treasury supply exceeds natural market demand, and the central bank is forced to print money to buy bonds (causing currency depreciation) — all three conditions met simultaneously is what Dalio calls the “debt death spiral.” All three conditions are converging in sync.

Q7: Can Russia Mediate?

Unlikely. Iran and Syria are Russia’s two allies in the Middle East. Syria has already fallen into America’s sphere of influence. Iran is the last one. If you are Russia, you do everything possible to keep this war going. It is a better strategic opportunity than the Ukraine war — and American credibility is already shattered (bombing mid-nuclear-negotiations, Minsk agreements torn up, etc.).

Q8: Will Midterm Election Pressure Force Trump to End It Faster?

He wants to — but ending a war is not a unilateral decision. Iran has suffered enormous losses. Without long-term U.S. commitments, Iran keeps fighting. The U.S. cannot not respond. That is the definition of a protracted war.

NATO’s and America’s credibility is effectively bankrupt.

Q9: Trump Visiting China at the End of March?

Irrelevant. Political theater. Striking Iran is a direct chokehold on China’s energy lifeline. There is nothing meaningful to discuss.

Q10: Why Does the U.S. Need a Long-Cycle War?

To contain China. Both the Ukraine war and the Iran war serve this objective. China will also be hurt, but relatively less — which effectively makes it a Chinese victory. The risk-reward is asymmetric: the strategic advantages this creates for China are multiples of the damage.

If Iran holds its ground and keeps oil prices elevated, the relative positioning becomes even more favorable for China.

Q11: If Not a Protracted War — What Happens to Oil and Gas?

Two non-protracted-war scenarios:

Scenario A — U.S. Quick Victory (Iran Collapses): Extremely bearish for China. The U.S. controls the chokepoint. A strategic catastrophe for Chinese energy security.

Scenario B — Trump Retreats: Petrodollar system collapses → Oil undergoes violent repricing (but with a different structure than today) → Dollar may crash → Massive repricing across all asset classes.

The petrodollar system has operated for 52 years. The volatility from its collapse is essentially unmodelable.

VII. The Bottom Line

Trump’s latest blink is not a de-escalation. It is escalation in a different form.

Every retreat destroys American credibility. Every broken promise pushes Iran further from the negotiating table. Every betrayal of Gulf allies loosens another bolt on the petrodollar architecture.

Markets are celebrating a few green candles. The smart money is asking: What happens when the system that has underpinned American hegemony for 52 years begins to fracture?

We have been building toward this answer throughout the Hormuz Series:

Part I argued that markets have far from priced in the true risk

Part II mapped the global energy vulnerability rankings

Part III revealed the first crack in $39 trillion of debt

This special edition adds the keystone: the petrodollar system itself is now in jeopardy.

Part III dealt with slow-moving variables — $39 trillion in debt, BRICS de-dollarization, central bank gold hoarding. This edition connects those slow variables to the fracturing of the petrodollar system: Trump’s retreat is the catalyst — it activates both slow and fast variables simultaneously, pointing toward the same endpoint.

Not in 10 years. Not as a theoretical risk. Now. Because the man who holds this system together just told the world — yet again — that America’s commitments are not worth the paper they’re written on.

I can understand there is no silver bullet in this scenario but what would you think is the best option for the U.S. to opt to ensure the best of both worlds. There is a big variable of Israel but discounting that what can the U.S. do to save the remaining credibility it has (if there is any).