Day 22 of Hormuz: The First Crack in $39 Trillion

America Is Destroying Its Deadliest Weapon — And It's Not Missiles.

Day twenty-two of the Strait of Hormuz closure. Brent crude has crossed $108.

Japan is counting how many more days its LNG reserves can last. South Korea is worrying about when rolling blackouts will begin. India is scrambling for LPG. Europe is watching its natural gas stockpiles dwindle. Every country is staring at its most painful nerve — and that’s normal. When your house is about to lose power, you don’t care about someone else’s monetary system.

And Americans? Americans might be celebrating. We’re a net energy exporter. We have shale gas. Our natural gas costs one-fifth of Europe’s. Oil prices are up? That’s everyone else’s problem.

But while Americans bask in their energy advantage, something is being quietly destroyed by this war — something a hundred times more important than oil.

The dollar.

Not whether the dollar is up or down today. But a deeper question — what is this war doing to the dollar system itself? When you stack the Hormuz energy crisis, a national debt that just breached $39 trillion, a Debt/GDP ratio exceeding 125%, and the fact that neither party will stop printing money — you see a picture far more disturbing than oil prices.

A picture of the empire’s most powerful weapon. A weapon being destroyed by its own master — who remains completely oblivious.

I. America’s Most Powerful Weapon Is Not an Aircraft Carrier

America has 11 nuclear-powered aircraft carriers, the world’s largest air force, and 750 military bases across 42 countries. But none of these are America’s most powerful weapon.

The most powerful weapon is the dollar.

You might think that’s rhetoric. It’s not. Let me explain how this weapon actually works.

50.49% of global payments are settled in dollars (SWIFT, December 2025 data). 56.92% of global central bank reserves are dollar-denominated assets (IMF, Q3 2025 data). When you buy a barrel of oil, a ton of copper, or a shipment of natural gas in any country, you most likely need to convert your currency into dollars first, then pay. This means virtually every major commodity transaction in the world passes through the dollar system.

This is the so-called “Exorbitant Privilege.” Former French President Valéry Giscard d’Estaing (then serving as Finance Minister) saw through this in the 1960s and coined the term. Sixty years later, this privilege has not only persisted — it has grown more vast, more systematic, and more irreplaceable.

And here’s the key — it’s more useful than aircraft carriers.

Aircraft carriers can bomb Iran. But the dollar can suffocate a country without firing a single missile. Ask Russia. In 2022, the United States froze $300 billion of Russia’s central bank reserves held overseas — not through war, but through SWIFT. Ask Iran. Sanctions have driven Iran’s oil exports to near zero.

This is America’s real weapon. Not military power — military power is the bodyguard of this weapon. It’s the dollar itself.

Even China — the largest competitor that is rapidly catching up to or surpassing the United States in nearly every tangible dimension including manufacturing, renewable energy, AI, and military — is completely unable to compete with America on the dimension of monetary hegemony. The renminbi accounts for less than 2% of global payments; the dollar accounts for 50%. This is the gap China cannot close.

But now, this weapon has a problem.

II. $39 Trillion: A Number More Dangerous Than World War II

Let me show you a number.

On March 17, 2026, the total debt of the United States federal government crossed a new milestone: $39,016,762,910,245 — 39 trillion dollars.

Five months ago, it had just crossed $38 trillion. Two months before that, $37 trillion. The pace of debt accumulation is accelerating — over the past year, it has grown by an average of $8 billion per day. $334 million per hour. $5.57 million per minute. $92,900 per second.

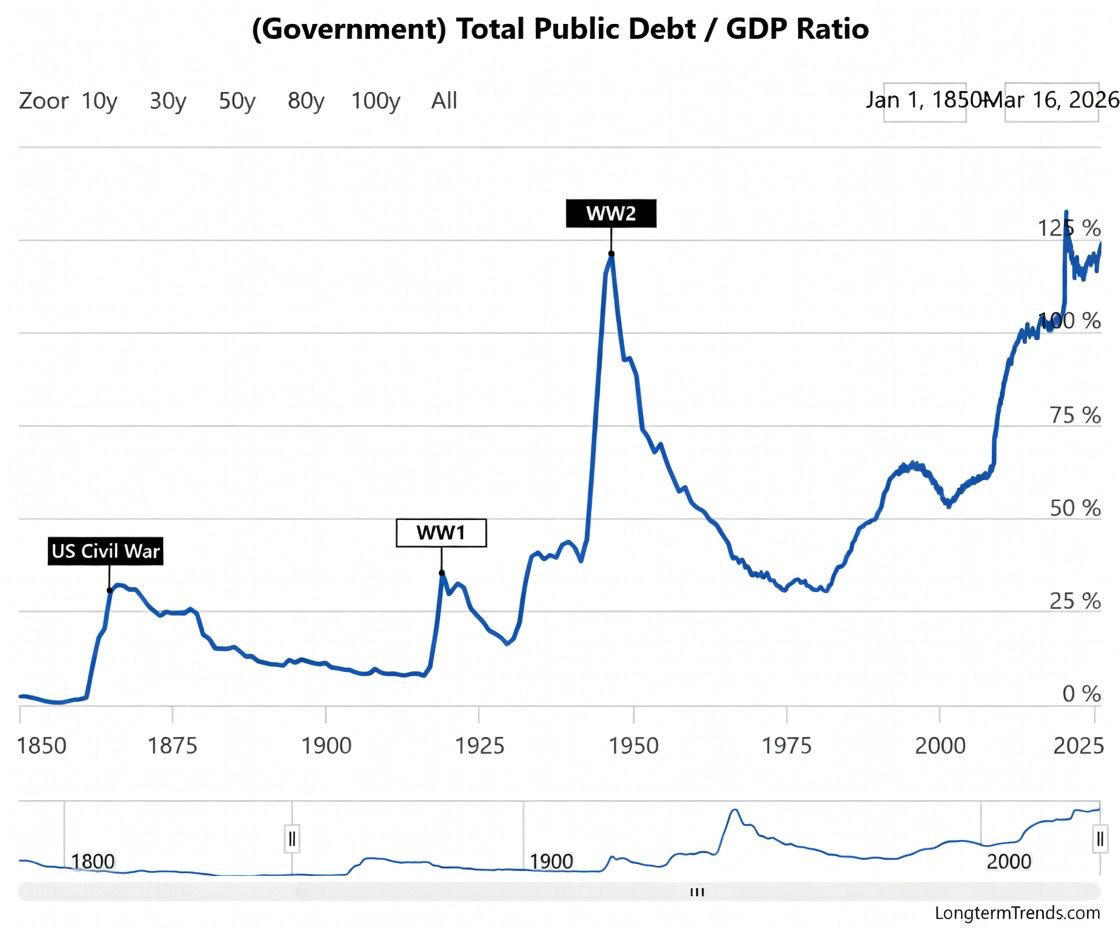

Debt/GDP ratio: 125.2% (Q4 2025).

That number alone may not shock you. Let me put it in context.

During World War II, America mobilized 16 million troops, built hundreds of thousands of aircraft and thousands of warships, and converted its entire industrial base to a wartime economy. It was the largest national mobilization in human history. At the peak of that mobilization, Debt/GDP reached approximately 119% (Total Public Debt basis, the same methodology used for today’s 125%).

America in 2026 has surpassed the peak of World War II — without fighting a world war.

Where did the money go? Not building aircraft carriers. Not building high-speed rail. Not investing in the future. Stimulus checks, social transfer payments, Medicare, Social Security — and an ever-growing slice: interest.

The CBO’s latest projections are even more unsettling: if nothing changes, by 2036 the national debt will balloon to $63 trillion. Debt/GDP will reach 120% (measured only by debt held by the public; the total debt figure will be far higher). The annual deficit a decade from now will expand from the current $1.9 trillion to $3.1 trillion — every year.

Stan Druckenmiller — arguably the greatest macro trader of the past three decades — saw this trend coming in 2013. His exact words: “We are stealing from our future and our children’s future.”

Twelve years later, he hasn’t changed his view — he’s doubled down. Just last week (March 15, 2026), in an interview hosted by Morgan Stanley, he made an even more striking statement: “The dollar will probably hold up in my lifetime, but I can’t be sure it’ll still be the reserve currency in 50 years.”

He also said something about crypto assets, but that’s not the point. The point is: when the most successful macro trader on the planet begins publicly discussing the end of the dollar’s reserve status — even if it’s 50 years away — you should listen carefully. Because markets never wait until the last day to price things in.

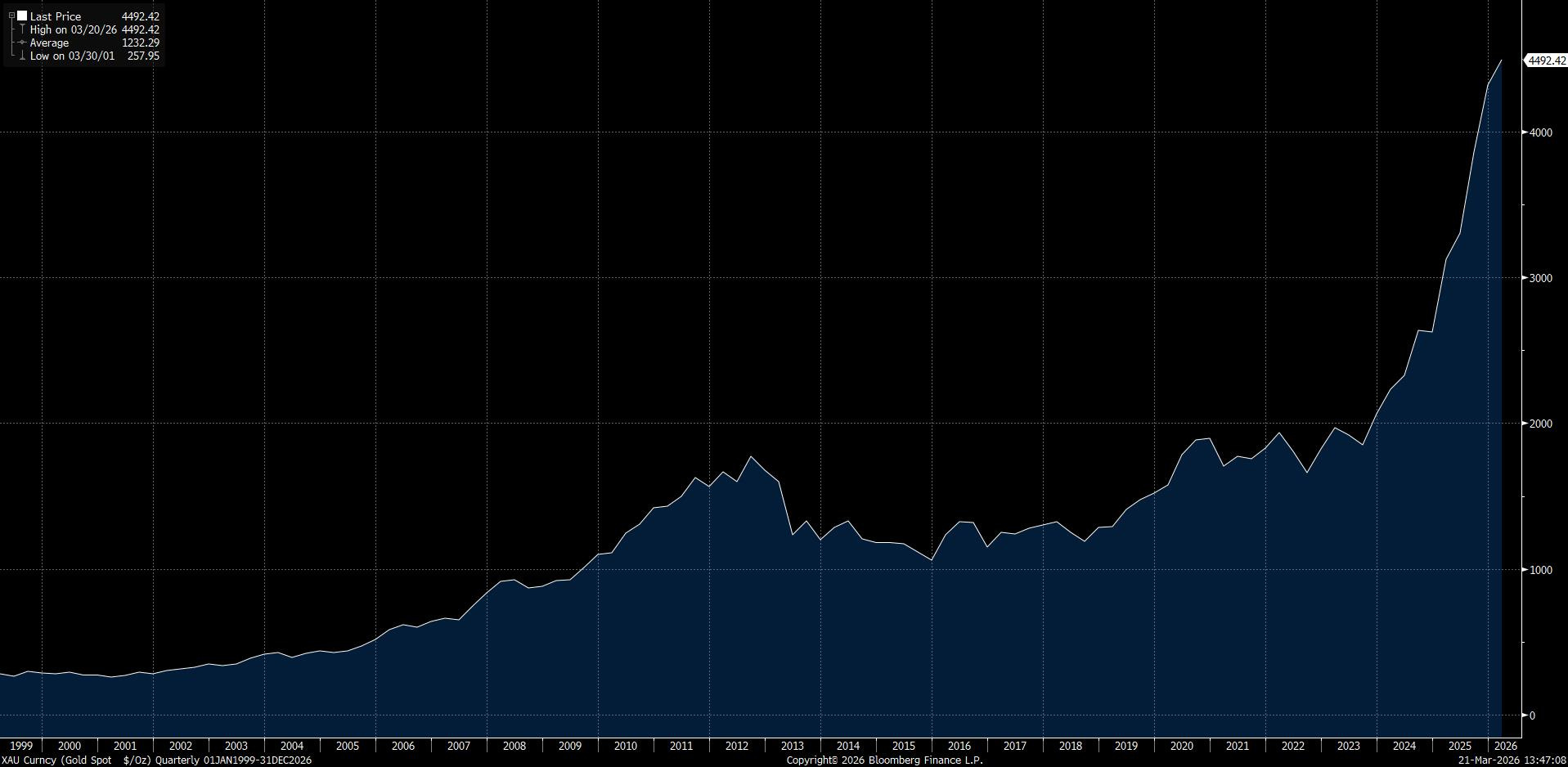

Gold has already moved first. When Druckenmiller first sounded the alarm in 2013, gold was at $1,200. In January 2026, gold hit an all-time high of $5,589. A 365% gain. And when he first said those words, America’s Debt/GDP had only just crossed 100%.

But what’s truly unsettling isn’t the numbers themselves — it’s the shape.

Look at the 126-year historical curve of America’s Debt/GDP. The World War II surge was a spike — it shot up to about 119% and then came back down quickly. The 2020s look completely different. It’s a plateau — sitting flat at the 120–127% range with no downward trend. No spike means no deleveraging.

Pull that curve out to a 126-year scale, and the pattern becomes even more brutal: from 1900 to 2026, four major surges — World War I (~8% → 35%), World War II (~40% → 119%), the 2008 Financial Crisis (~64% → 100%), COVID (107% → 127%+) — and after each surge, the magnitude of deleveraging has been smaller. After WWI, it fell from 35% back to ~16%. After WWII, from 119% back to ~32%. After 2008, there was almost no deleveraging. After COVID: no deleveraging at all — it kept rising.

The ~32% level in the mid-1970s was the post-war absolute low, and it has never returned since. And that time window corresponds precisely to two events: the 1971 collapse of the Bretton Woods system (the dollar’s decoupling from gold), and the first oil crisis of 1973–74. When you remove the last anchor of fiscal discipline — gold — you open Pandora’s box of unlimited money printing.

The reason America was able to deleverage after WWII was four conditions: an unrivaled monopoly on global productivity, the baby boom demographic dividend, real GDP growth driven by technological revolution, and dollar hegemony locked in by the Bretton Woods system.

America in 2026 possesses none of these.

China’s manufacturing output already exceeds that of the U.S., Japan, and Europe combined. America’s birth rate is declining. Dollar hegemony is precisely the thing being eroded. AI may bring a productivity revolution, but the vast majority of its fruits will be captured by tech giants, not the Treasury.

The numbers keep getting bigger. There are no conditions for deleveraging. Nobody thinks this is an emergency. Until you start counting the interest.

III. The Compound Interest Bomb

In fiscal year 2025, the U.S. federal government’s interest expense reached $970 billion — nearly tripling since 2020.

This figure already exceeds America’s defense spending. It exceeds Medicaid. It accounts for nearly one-fifth of federal revenue. And it’s accelerating — because every time a maturing low-rate bond is replaced by new high-rate debt, the number jumps another notch. Five years ago, the weighted average interest rate on U.S. Treasuries was 1.512%. Today it’s 3.355%. The rate has more than doubled, while the principal has simultaneously ballooned by nearly $11 trillion.

The CBO projects that by 2036, interest expenses will surpass $2.1 trillion. At that point, for every $4 of tax revenue the federal government collects, $1 will go straight to creditors — not to build roads, not for veterans, not for schools — to pay interest.

This is how the compound interest bomb works: you don’t need rates to spike dramatically. You just need rates to stay high enough for long enough.

Ray Dalio calls this state a “debt death spiral.” Just two weeks ago (March 15, 2026), Dalio once again issued a public warning. His criteria are precise — when three conditions are simultaneously met:

The ratio of debt interest to government revenue is persistently rising;

Treasury supply exceeds natural market demand, pushing rates higher;

The central bank is forced to print money to buy bonds, causing currency devaluation.

you’ve entered the death spiral.

Dalio also said something even more critical: “There won’t be a default — the central bank will step in and print money to buy debt. What this causes is currency devaluation.”

Let me translate: America will not formally default. It will default in a more covert way — by making the dollar itself worth less. Your bond has a face value of $100, and at maturity you’ll get $100 back, but the purchasing power of that $100 will have been eaten in half by inflation. This is a tacitly accepted, systemic, slow-motion default.

In the United States of March 2026, the three conditions Dalio described are converging simultaneously:

Interest-to-revenue ratio: The CBO projects it will reach 18.6% in fiscal year 2026, surpassing the historical high set in 1991;

The 10-year Treasury yield stood at 4.26% on March 18 — not far from the 5% critical threshold;

Foreign buyers are pulling back (more on this below).

And every day that Hormuz remains closed, every day oil stays above $100, inflation and yields keep pushing closer to that 5% line.

IV. Hormuz — Lighting the Fuse

Now you understand the construction of the bomb: $39 trillion in debt, 125%+ Debt/GDP, interest expenses exceeding military spending, and the three conditions of a debt death spiral closing in.

What the Hormuz war does is attach a fuse to this bomb.

The transmission chain works like this:

Strait closure → 20% of global oil and LNG supply cut off → oil surges from $72 to $108, a 50% increase in three weeks → inflation expectations spike → the Fed is locked: it can’t cut rates (inflation too high) and doesn’t dare raise them (the economy is slowing) → the fiscal deficit explodes under triple pressure (war spending + rising interest + falling tax revenue from a slowing economy) → bond issuance surges → foreign buyers are pulling back → rates are pushed higher → back to the death spiral.

The IEA has called this “the most severe disruption to global energy supply in history.” Analysts warn that if it persists for four months, Brent crude could reach $135. In extreme scenarios, even $120–150. And this isn’t theoretical — Iraq and Kuwait have already begun shutting down production, and the UAE could be next.

Why are foreign buyers pulling back?

Because you just froze $300 billion of Russia’s reserves. Because you just weaponized the SWIFT system. Because every central bank holding U.S. Treasuries is now reassessing one question: What if America does this to me one day?

The data doesn’t lie. Let me show you a set of truly alarming numbers:

BRICS nations are quietly exiting the Treasury market.

China: From a peak of $1.3 trillion in 2013, holdings have been steadily declining — according to U.S. Treasury TIC data, they fell to approximately $890 billion by November 2025; Bloomberg’s direct holdings tracker (HOLDCH) shows an even lower figure, below $700 billion by early 2026. Regardless of the measure, the scale of reduction is staggering. In February 2026, reports emerged that Chinese regulators had urged domestic financial institutions to cap their Treasury holdings.

Brazil: Held $229 billion in November 2024, reduced to $168 billion a year later — a 27% decrease.

India: Over the same period, fell from $234 billion to $186.5 billion (partly driven by the central bank selling Treasuries to defend the rupee’s exchange rate, but the objective effect is the same — the marginal buyer of Treasuries is vanishing).

Japan: Still the largest foreign holder (approximately $1.2 trillion), but holdings have stopped growing since 2014 and have slightly declined in recent years — even the biggest buyer is no longer adding to its position.

ING’s global head of markets put it bluntly: “BRICS nations are quietly exiting the Treasury market.”

And Bloomberg’s February 2026 headline was even more direct: “Once the Biggest Foreign Creditor of the U.S. Government, China Has Quietly Halved Its Treasury Holdings.”

These aren’t conspiracy theories. These are public, traceable, ongoing facts.

But to understand the severity of these facts, you need to see what they’re shaking — the two core pillars of dollar hegemony.

V. The Petrodollar: An Old Pillar Is Cracking

The dollar’s energy hegemony is not natural. It has a precise starting point: 1974. That year, Kissinger brokered a world-changing arrangement with the Saudi royal family: Saudi Arabia would price and settle its oil exports in dollars, and in exchange, the United States would provide military protection and security guarantees. This was not a formal treaty with an expiration date, but an informal understanding built on security commitments and economic interests — yet it was this understanding that formed the bedrock of the petrodollar system.

Fifty-two years later, the cracks are far deeper than most people realize. Saudi Arabia is systematically loosening this system through actions — not declarations.

In January 2023, Saudi Arabia’s Finance Minister publicly stated at the World Economic Forum in Davos that the kingdom was “open to discussions about trade settlements in currencies other than the dollar.”

That same year, China and Saudi Arabia completed the first yuan-denominated oil transaction. Saudi domestic banks began offering renminbi services. In June 2024, the Saudi central bank joined mBridge — a China-led cross-border payment platform and digital currency clearing network that bypasses SWIFT.

And in this war, an even more ironic development has emerged: Iran is considering allowing some oil tankers to pass through the Strait of Hormuz — on the condition that payment is made in renminbi, not dollars.

Do you hear that? While America is spending hundreds of billions of dollars fighting this war, the war’s byproduct is eroding the dollar’s settlement status.

There’s an even deeper structural shift: Saudi Arabia no longer unconditionally depends on U.S. security guarantees. In September 2025, Saudi Arabia signed a strategic mutual defense agreement with Pakistan — placing the kingdom under Pakistan’s nuclear umbrella. This is the first crack in the security cornerstone of the petrodollar system since 1974.

When your most important ally starts looking for alternatives, the writing is on the wall.

None of these cracks are individually fatal — roughly 80% of global oil transactions are still denominated in dollars, and the renminbi’s share remains minuscule. But history tells us that the decline of a reserve currency is never linear. When the British pound went from global hegemon to being replaced by the dollar, the tipping point didn’t happen when its share dropped from 80% to 50% — it happened at the moment trust began to loosen.

Look at the trajectory of the dollar’s reserve share: 71% in 2000, 64% in 2008, 58.5% in Q1 2025, and down to 56.92% by Q3 2025. A 14 percentage point drop in 25 years. The trend is accelerating, not decelerating.

Once behavioral change begins, cracks become self-reinforcing. That is reflexivity.

VI. The War Is Exposing the Fatal Fragility of the AI Supply Chain

Dollar hegemony isn’t built solely on oil. In the 21st century, AI chips and computing infrastructure are becoming a new extension of American economic influence — the global semiconductor market is projected to reach approximately $1 trillion in sales this year. But the Hormuz war is exposing an unsettling truth: this seemingly indestructible AI supply chain is physically extremely fragile.

Start with the most critical link: TSMC. According to TrendForce and other industry research firms, Taiwan produces over 90% of the world’s advanced logic chips at the 5nm node and below, with TSMC as the dominant force — every NVIDIA AI accelerator, every Apple mobile processor — all come from Taiwan’s fabs. And Taiwan imports 97% of its energy, of which approximately 37% of its LNG comes from the Middle East (per Goldman Sachs analyst Alvin So’s team estimates). Even more alarming, Taiwan’s strategic LNG reserves amount to only about 11 days — compared to South Korea’s 52 days and Japan’s roughly three weeks (per IEEFA and Morgan Stanley estimates). Qatar has already declared force majeure.

Morgan Stanley’s Head of Asia Technology Research Shawn Kim put it directly: “The Hormuz disruption won’t automatically halt chip production, but it will transmit through three pathways — electricity costs, material supply, and the economics of AI infrastructure — layer by layer.” He added that companies building energy-intensive facilities such as large-scale data centers may face higher operating costs and lower returns.

If TSMC is forced to reduce capacity due to power or supply pressures, the impact isn’t limited to one company — it’s the entire global AI industry’s computing supply. AI chip demand already exceeds TSMC’s capacity; any production disruption would jeopardize the $650 billion in AI capital expenditure that Big Tech plans to deploy this year. The disruption would also spill over into industries beyond tech — from consumer electronics to automotive manufacturing — sectors already coping with a historic global memory chip shortage.

But TSMC is just the tip of the iceberg. Critical materials for chip manufacturing are simultaneously being cut off:

Helium — roughly one-third of the global supply is processed in Qatar. After Qatar’s major LNG plants were shut down following Iranian drone strikes, Bloomberg Economics estimates that approximately one-third of global helium capacity is now offline. Helium is an irreplaceable cooling medium in wafer fab lithography and etching processes.

Sulfur — a byproduct of oil and natural gas refining — is an upstream raw material for semiconductor chemicals.

If helium shortages persist, Bloomberg Economics analyst Michael Deng predicts that chip fabs may be forced to prioritize high-margin AI chips and sacrifice lower-margin consumer and automotive chips — the entire semiconductor industry’s priority structure will be rearranged by the war.

There’s also an overlooked logistics chain: according to Frank Bösenberg, Managing Director of the German semiconductor industry association Silicon Saxony, speaking to Bloomberg, Cathay Pacific Cargo handles approximately 30% of global wafer shipments, with its regional hub in Dubai — and Dubai’s airport has been hit by drone strikes. Bösenberg warns that disruption to this logistics chain could hit European and Asian chip supplies faster than raw material shortages.

Meanwhile, the Trump administration is considering imposing a comprehensive licensing regime on global AI chip exports from NVIDIA and AMD — requiring U.S. government approval for virtually all exports. Bloomberg reports that American officials have drafted regulatory proposals to extend existing export controls covering roughly 40 countries to the entire world, making the U.S. government the “gatekeeper” of the global AI industry. This is the most substantive chip export control action by this administration since it repealed Biden’s “AI Diffusion Rule” last May.

Here lies a deep contradiction: on one hand, America is trying to consolidate control over global AI computing power through export controls; on the other hand, the Hormuz war is exposing the fragility of that control at the physical level — when you control chip design and export licensing, but chip manufacturing depends on an island with only 11 days of LNG reserves, and that island’s energy lifeline is being severed by the very war you started — the value of that control has to be discounted.

VII. Gold’s Verdict

If you find the analysis above too abstract, look at the verdict the market has delivered.

Gold — humanity’s oldest monetary trust-voting mechanism, stretching back five thousand years — is sending a historic signal.

In January 2026, gold hit an all-time high of $5,589 per ounce and currently trades around $4,500. Three years ago, it was still below $2,000.

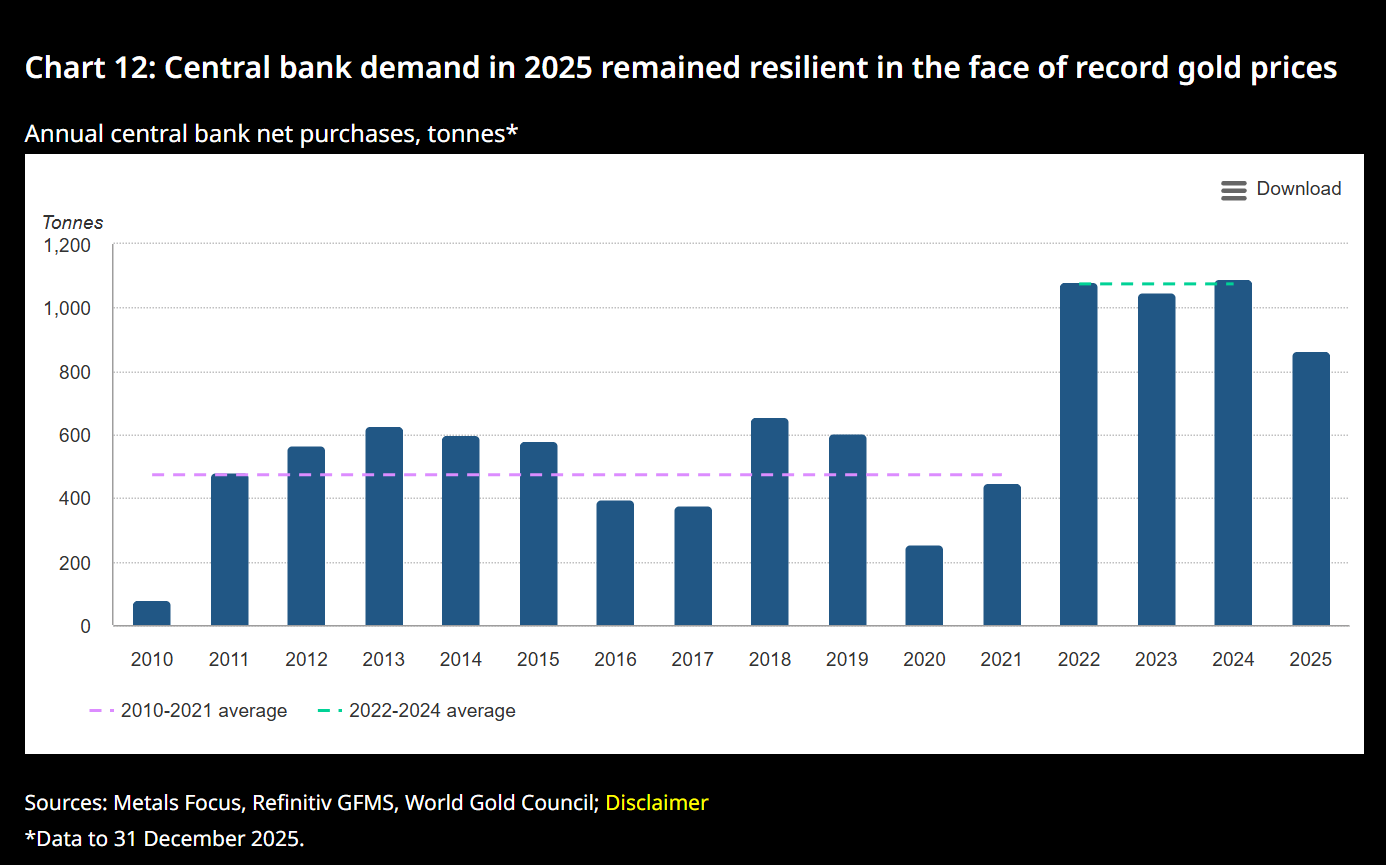

But the force driving this gold bull market is unlike any before it. Not an inflation hedge. Not risk-off sentiment. It’s central banks systematically replacing dollars with gold.

Since the outbreak of the Russia-Ukraine war in 2022 — more precisely, since the United States froze $300 billion of Russia’s reserves — global central bank annual gold purchases have doubled from the previous 400–500 tons to over 1,000 tons — exceeding 1,050 tons in each of the three consecutive years from 2022 to 2024. Although 2025 saw a pullback to approximately 850 tons, this remains far above the 2010–2021 average of roughly 480 tons — a new normal has been established.

In 2025, Poland, China, and Brazil were the largest buyers. The People’s Bank of China has been purchasing gold for 15 consecutive months (through January 2026). A World Gold Council survey shows that 95% of central banks expect to continue increasing gold holdings in 2026, with projected purchases of approximately 755 tons.

Goldman Sachs raised its gold price target to $5,400 — and gold has already surged past $5,589, leaving even Wall Street’s most optimistic forecast behind. Among their stated reasons is a new term — the “Debasement Trade” — referring to the trend of investors turning to gold driven by anxiety over government debt and long-term monetary stability. Goldman considers this “a completely new demand category that did not exist in previous gold cycles.”

Central banks are not speculating. The fact that they continue buying in large quantities above $4,000 shows that the objective is not short-term returns but long-term reserve security — because gold cannot be frozen by any government.

When 95% of the world’s central banks are all doing the same thing — reducing dollars, increasing gold — they’re telling you one thing: trust is shifting.

VIII. The Self-Destruct Button Pressed by the Empire’s Own Hand

Stack all the preceding sections together, and the logical chain closes.

The dollar is America’s most powerful weapon. This weapon is supported by two things: the global economy’s rigid demand for dollars (petrodollars + compute-dollars), and global investors’ trust in U.S. Treasuries. The Hormuz war is eroding both simultaneously.

On the demand side: The cracks in the petrodollar are widening — Saudi Arabia has publicly signaled openness to non-dollar settlement, yuan-denominated oil transactions have launched, mBridge bypasses SWIFT. The compute-dollar monopoly is loosening — energy costs are surging, export controls are backfiring, countries are accelerating computing sovereignty. Every day the war continues, the momentum for de-dollarization grows stronger — because the war itself is demonstrating to the world the risks of dollar weaponization.

On the trust side: $39 trillion in national debt, 125%+ Debt/GDP, interest expenses exceeding defense spending and Medicaid, the war pushing up deficits, deficits pushing up bond issuance, BRICS nations quietly exiting the Treasury market — the three conditions of a debt death spiral are closing in. The CBO projects deficits will double. Dalio says there won’t be a default, but there will be devaluation. Druckenmiller says the dollar may no longer be the reserve currency in 50 years. And neither party will touch Social Security or Medicare. No one will voluntarily defuse the bomb.

Of course, the dollar system has its resilience — and that resilience should not be underestimated. Before passing judgment on the dollar, we must confront its strongest defenses head-on.

First, network effects create lock-in. The global financial infrastructure — the FX market (daily turnover of $7.5 trillion, 88% of which involves the dollar), derivatives pricing, trade finance, cross-border payments — is deeply embedded in the dollar system. This is not a system you can simply “switch” away from. It’s more like a language: even if everyone knows a better alternative exists, the switching costs are prohibitively high. SWIFT, Fedwire, CHIPS — these pipes are moats in themselves.

Second, there is no alternative. The eurozone lacks fiscal unity and has no unified bond market. The renminbi’s capital account remains not fully open; its offshore liquidity pool is a fraction of the dollar’s. The yen and the pound are too small to bear global reserve demand. This is the “Churchill dilemma” — the dollar is the worst reserve currency, except for all the others.

Third, crisis reflexivity reinforces the dollar. In every global risk-off event, capital has actually flooded into dollars and Treasuries — the March 2020 pandemic panic, the 2022 Russia-Ukraine war, the 2023 banking crisis. The DXY rallied each time. Fear itself creates dollar demand. This self-reinforcing safe-haven mechanism is something no other currency possesses.

Fourth, the AI productivity revolution. This may be the sharpest card in the dollar bull’s hand: if AI truly delivers a productivity leap comparable to the steam engine or electricity, America — as the undisputed leader in AI technology — could plausibly grow its way out of debt, just as the post-WWII economic miracle compressed Debt/GDP from 119% back to 32%.

Each of these four cards is powerful on its own. But let me take them apart, one by one.

Network effects are real, but they protect the stock, not the flow. De-dollarization of global trade doesn’t require replacing SWIFT or Fedwire — it just needs to route around them at the margin. mBridge, CIPS, digital renminbi cross-border settlement — these aren’t trying to destroy the dollar’s pipes; they’re building a parallel road alongside them. Network effects never collapse linearly — they have a tipping point, and once enough participants begin using alternative networks, switching costs plummet. The pound’s network effects in 1945 were stronger than the dollar’s today — because the British Empire’s colonial trade system was compulsory — yet from 1945 to 1965, sterling’s reserve share crashed from roughly 87% to under 30%.

No alternative? That’s precisely the point. The decline of a reserve currency doesn’t require a single replacement. The pound wasn’t “replaced” by the dollar — it was diluted by a diversifying reserve system. The same thing is happening in 2026: central banks aren’t searching for “the next dollar.” They’re diversifying — more gold, more euros, more renminbi, more local-currency settlement. The dollar’s share can fall from 57% to 40% without any single currency replacing it. This isn’t “replacement.” It’s “dilution.”

The crisis safe-haven effect is real — but it has a fatal prerequisite: trust. Capital flooded into dollars in 2020 and 2022 because investors believed U.S. Treasuries were a “risk-free asset.” But when Debt/GDP exceeds 125%, when interest expenses exceed defense spending, when Treasury supply persistently outstrips demand — the words “risk-free” are themselves being eroded. More critically, the moment the U.S. froze Russia’s reserves in 2022, it scratched a crack into the “safe haven” sign — because a safe haven’s premise is that anyone can safely store assets there, not “you’re safe as long as you don’t cross me.” The next time global risk-off hits, will capital still flood unconditionally into dollars? The answer to that question is shifting from “of course” to “maybe.”

As for AI solving the debt — this is the most seductive narrative, and the one most in need of a reality check. Research from the IMF and CEPR shows that in the post-WWII deleveraging, GDP growth contributed less than half. The real drivers were two conditions that 2026 America entirely lacks: sustained fiscal surpluses (the U.S. ran budget surpluses for multiple consecutive years after the war), and financial repression (the Fed held real interest rates negative for decades). The reality in 2026: neither party will cut Social Security or Medicare (which account for over 60% of federal spending) — fiscal surplus is a political fantasy. And inflation — especially with the Hormuz war driving oil prices higher — makes financial repression equally impossible. AI’s productivity gains may be real, but they flow to tech giants’ income statements, not to the Treasury’s balance sheet — unless America dramatically raises taxes on tech companies, which in the current political environment is equally a fantasy.

So yes, resilience is real. But resilience is not the same as irreversibility. The British pound was also a safe haven during both world wars, also had the world’s deepest bond market, also had the most powerful navy as its escort — until it didn’t. From 1945 to 1965, sterling completed its fall from hegemonic currency to ordinary currency in just 20 years. Every one of the dollar’s “moats” is real, but none of them is eternal.

And this is the deepest paradox of the Hormuz war —

The war is strengthening the dollar and destroying the reasons it’s strong.

DXY at 100 is fear, not strength. Capital has nowhere to hide — so it floods into USD. But every day this war continues, it erodes the two pillars holding up the edifice: the petrodollar — Iran is already floating yuan-settled crude to reopen Hormuz; the compute-dollar — hard to enforce chip controls when your allies are bleeding from an energy crisis you started.

Fear is a fast variable. Trust is a slow one.

Right now, fear is winning. The DXY is rising, Treasuries are being bought, and the dollar looks invincible. But fear fades — wars end, oil prices retreat, risk-off sentiment subsides.

Trust doesn’t come back.

The $300 billion frozen from Russia won’t be forgotten. The precedent of yuan-settled oil won’t be reversed. Central banks that have begun diversifying reserves won’t turn back. The mBridge infrastructure already built won’t be dismantled. These are irreversible structural changes — they don’t disappear just because the DXY pulls back from 100 to 95.

This is the cruelest paradox of empire: it launched a war to defend its most powerful weapon, but the war itself is the hammer destroying it. Every missile that falls on Hormuz carves another crack in the dollar’s foundation.

And for investors, paradox is opportunity. While the market is still trading the fast variable of fear, the slow variable of trust is repricing everything — from gold to Bitcoin, from energy to non-dollar currencies, from the rate curve to volatility structures. The moment the DXY pulse fades and structural erosion surfaces — that is the starting gun for this trade framework.

These opportunities will be unpacked one by one in the upcoming installments of the Hormuz series.

This is Part III of the Garrett’s Signal Hormuz Series. The first two:

📡 Who Breaks First? — Tracking the global energy vulnerability ranking

💣 Hormuz is BATTLE FIELD — Arguing that markets are far from pricing in the real risk

This installment turns the lens from energy to currency — asking what this war is doing to the dollar system itself.

Next, we return to the trading desk — when cracks become trends, where should the money go?

Garrett’s Signal · March 2026 · Hormuz Series Part III

How ironic. America, which should be the most democratic nation, has been the most demanding dictator.

And by punishing its foes, let go what made it strong.

Meanwhile for cryptos, yes logic validates, but timing is everything.

Thank you Garrett, what a wonderful piece of writing.

I agree that the dollar is the United States’ most powerful weapon. Its strength comes not just from being the reserve currency, but from America’s ability to use the dollar system, sanctions, freezes, and payment infrastructure as tools of pressure and control. What we are seeing with Russia and China is not a conventional war, but a financial war centered on the power and weaponization of the dollar.